2021 Q3 Review

Quarterly review of results, the market, portfolio companies, and insights

Results

The third quarter of 2021 ended on September 30th, 2021.

For the third quarter, the consolidated return for Torre Financial accounts was 13.21%.

For the same period, the S&P 500 (SPY) returned 0.58%.

The Dow Jones Industrial Average (DIA) returned -1.49%.

Returns for individual accounts may vary as each account is managed separately. While indices serve as a useful benchmark, each portfolio is tailored towards each investor’s unique investment objectives and risk profiles.

Market

The bull market continued in July and August, featuring low volatility with a constant churn higher. The story changed in September as turbulence returned. The indices gave back most gains from the quarter and the SP&500 broke below its 50-day moving average.

The beginning of the quarter was marked by optimism, driven by the strong reopening momentum. COVID was seemingly under control. Companies were making plans to return to the office. Although inflation spiked, it was deemed transitory as supply lines around the world were opening back up. Ultimately, many of those plans were delayed as the Delta variant entered the picture.

The political scene both in the USA and abroad, particularly in China, was on display.

The US military exited Afghanistan, leading to immediate instability in the region. New policy proposals were circulated, aiming for increases in infrastructure spending, social welfare, and taxes.

The Chinese Communist Party (CCP), under Xi Jinping, has enacted a series of seemingly aggressive actions against many national companies. China banned for-profit school tutoring, driving a handful of publicly-traded companies towards zero over a few day period.

The CCP launched antitrust investigations against their largest companies and delivered a $2.8 billion fine to Alibaba. Shares of Alibaba are down nearly 50% over the last year. (For what it’s worth, Charlie Munger of Berkshire Hathaway seeks to take advantage, doubling down on his position in Alibaba.)

DiDi, the Chinese ride hailing app, had a similar experience. Two days after DiDi went public in New York, they were ordered to stop signing up new users while under investigation, were forced to remove their apps from the app stores, and were hit with an antitrust fine. DiDi shares are down 45% since their July 2021 listing.

The potential default of Evergrande, the second largest property developer in China, has created angst in the market. With over $300 billion in debt coupled with the potential inaction by the Chinese government, Evergrande’s failure could have widespread fallout.

Returning to market action, over the last year buying the dip at the 50-day mark has been a successful strategy. That trend finally broke. The market is now in the midst of a moderate sell off.

There is no shortage of concerns in the market today.

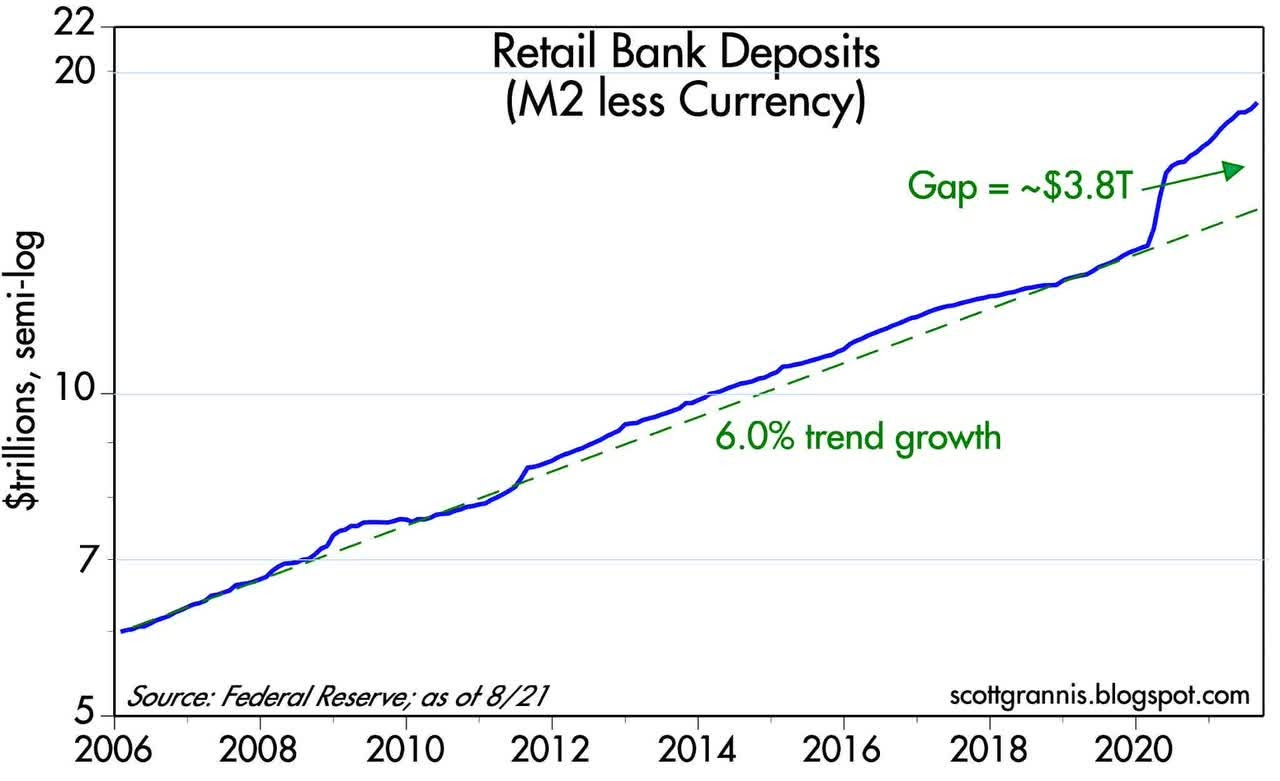

The significant actions taken to counteract COVID, however, led to a generous increase in the money supply, unlike anything in our past.

The Fed continues to be accommodative but has made it clear that tapering is likely to begin soon. The market took it in stride, as the real funds rate will likely remain negative for many years, which is anything but restrictive.

The abundance of deposits will likely find their way to better use elsewhere.

Portfolio

The following cohorts are bucketed by their contribution to the portfolio. The ranking considers both the performance of the individual stock and position sizing.

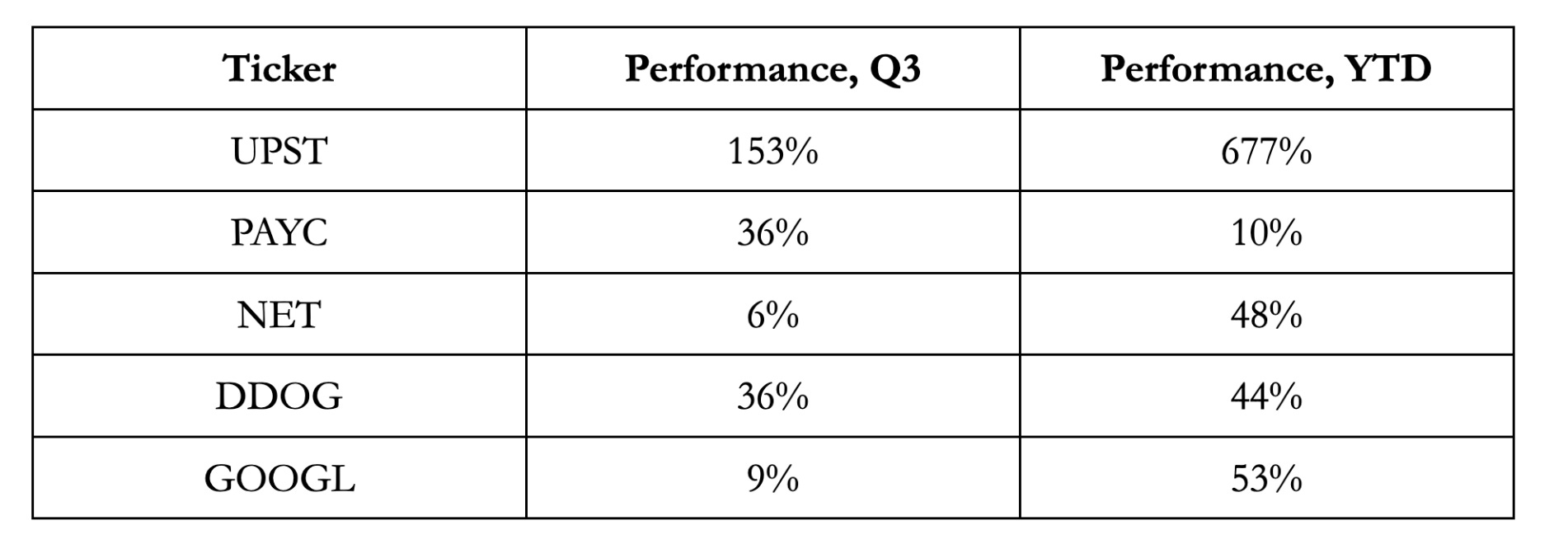

Top performers in Q3

Bottom performers in Q3

Commentary

UPST. Needless to say, Upstart had an impressive third quarter. The company has performed exceptionally well since their IPO in December 2020. Each earnings release has resulted in significantly higher guidance. Upstart is growing revenue triple digits and has positive earnings and cash flow. The company launched their platform in Spanish and expanded into auto loans. They are capitalizing on their Prodigy acquisition, moving quickly to triple the number of dealership customers and reposition it as Upstart Auto Retail. I believe the recent price action to be the result of large investors initiating positions, which, if true, could provide stability. I maintain UPST as a top position, adding opportunistically.

NET. Cloudflare continues to innovate relentlessly. They are pushing aggressively into the cloud service provider space, competing openly with Amazon’s AWS and other cloud providers. In addition to routine announcements, Cloudflare’s Birthday Week and Speed Week delivered a plethora of new offerings. While Cloudflare’s price may seem extended, it is well supported by a strong backlog. I maintain NET as a top position, adding opportunistically.

LMT. Lockheed Martin, a well-known defense contractor, is a very strong and reputable company. They are currently facing some headwinds regarding issues with their signature F-35, but more importantly the market seems to have topped out for their jets. Additionally with Democratic control of the government, Lockheed Martin is poised for a slowdown in growth going forward. There are better opportunities out there at this time. I recently cut LMT from the portfolio.

PYPL. PayPal, one of the leading digital payment processors, has experienced a significant tailwind from COVID and trends towards digitalization. Given their strong network of merchants and consumers, coupled with many promising opportunities ahead, I find PayPal to be a particularly attractive established compounder. Additionally, PayPal’s business model benefits from any increases in inflation, counteracting the impact interest rates may have on our other high growth companies.

Insights

I recently read an article from Ensemble Capital, The Risk of Low Growth Stocks Part 1: Stall Speed.

This article highlights the importance of a company’s ability to maintain their trajectory. It states that a significant deterioration in long-term growth can cause a permanent loss of capital; not simply volatility, but a true repricing of an asset due to its expected cash flows.

“When you stop growing you start dying.” -William S. Burroughs

The article goes on to state that any company growing at a slower pace than their overall market is effectively done.

“For companies, if they stop growing as fast as the economy they start slowly losing share of their customers’ wallet. They start losing relevance and as they are left behind by new competitors, their customers start thinking about them less and less and growth continues to slow before finally going into decline.”

This idea connects very closely with concepts shared throughout the quarter. I wrote a few articles covering my investment process, the importance of qualitative assessment, and thorough analysis of economic moats.

While the past can be, and often is, informative, it is imperative for an investor to look forward into what the future could become.

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.