2022 Q1 Review

Quarterly review of results, the market, portfolio companies, and insights

Results

The first quarter of 2022 ended on March 31st, 2022.

For the first quarter, the consolidated return for Torre Financial accounts was -13.71%.

For the same period, the S&P 500 (SPY) returned -4.61%.

The Nasdaq (QQQ) returned -8.76%.

Returns for individual accounts may vary as each account is managed separately.

Market

The first quarter of 2022 posted the first negative quarter since the pandemic hit.

The Nasdaq dipped into a bear market, dropping more than 20% from its recent high before rebounding and cutting those losses in half.

Inflation surged to its highest level in four decades, rising 7.9% over the last 12 months as of February 2022.

Russia’s invasion of Ukraine has rattled the world. Sanctions dealt a devastating blow to the Russian economy, at the same time pressuring already stretched supply chains.

U.S. oil futures climbed to roughly $130 a barrel in early March before declining back to around $100. A year ago crude oil traded at about $60 a barrel.

The energy sector posted returns of 39% in the first quarter. The second best performing sector was utilities with a gain of 4.7%.

Inflation has seemingly left the Fed with no choice but to raise rates.

The following chart shows inflation and interest rates over the past 60 years. Notice how they tend to move in tandem.

March brought the first 0.25% raise. Investors struggle to understand the pace of future raises. The market is currently pricing in a series of 0.50% raises over the remainder of the year.

Investors have dumped bonds, sending yields on corporate and municipal bonds as well as Treasurys higher.

In late March, the yields on 2-year U.S. Treasurys briefly surpassed yields on 10-year notes. An inverted yield curve, where shorter duration bonds yield more than longer dated bonds, is not normal and has often been seen as a leading indicator of a recession.

Portfolio

Top performers in Q1

Bottom performers in Q1

Commentary

CRWD. As a leader in endpoint security, CrowdStrike has been a standout amongst fast growing technology companies. The pandemic accelerated investment in cybersecurity. The geopolitical tensions add to that acceleration. This is not a momentary or temporary increase in spend. It is an important shift in upgrading their enterprise security posture, one that is likely to have durable effects.

V & MA. Visa and MasterCard have both held up well throughout the recent drawdown. They established companies with well-known competitive advantages. They both naturally benefit from inflation – both by processing increasing volume and the fact that they are capital-light businesses.

PYPL. PayPal, a leading online payment system, had a tougher time. Investors are concerned about the durability of PayPal’s growth. Ebay has been parting ways with PayPal, which has been an important headwind for revenue. Instead of going for growth at all costs, PayPal shifted to focus on quality, ensuring they were capitalizing on opportunities with higher return on investment. PayPal grew as an online checkout option, and has expanded into many areas of digital commerce, including discounts, returns, p2p, buy now pay later, and many more areas. As they look to establish a digital wallet, they have a lot of optionality as an interactive payment processor and with in person payments.

FB. Formerly known as Facebook, Meta announced their intentions to focus on creating the metaverse. After a disappointing earnings release, Meta lost $232 billion in market value in a single session, the biggest loss in market value for a US company ever. Investors are concerned about the effects of privacy updates and slowing growth, increasing competition from newcomers like TikTok, and whether the investments in the metaverse will pay off. Notwithstanding those concerns, Meta has a lot of potential. They are actively investing in commerce with efforts such as partnering with Shopify, Facebook Marketplace, and an NFT store in Instagram. They have a strong internal culture around performance – they are known for having top quality people.

OKTA. Okta has struggled since the acquisition of Auth0. Their CFO resigned, perhaps unregrettably. This quarter, Okta faced a security breach. While it was appropriately contained, they were criticized for how they responded. That being said, Okta is the leading identity service provider for cloud solutions. They have a strong management team with an ambitious vision. They have demonstrated successful execution in the past. Although it may take some time, they are likely to bounce back. Identity is a key pillar of a company’s security posture and Okta is the leader. Unless another company rises to challenge Okta, it is worth staying with them.

UPST. Upstart reported a strong quarter and guidance. They continue their foray into automobiles, recently partnering with Subaru and Volkswagen. Business has proceeded as usual. Volatility is likely more due to macro concerns. The valuation is currently very appealing, with the profitable company trading at 31x EV/EBITDA and growing revenue at 65%+ year over year.

INTU. Having recently acquired Mailchimp, Intuit continues leveraging their distribution channel to expand further into the small business space. Intuit continues business as usual. Investors may be concerned about the large acquisition. Relatedly, the recent decline could be in part attributed to the share price getting a bit ahead of itself.

Insights

The macro environment has been challenging and the recent correction has been longer lasting than prior drawdowns.

With inflation and rate increases, investors face difficult choices with asset classes. Cash, equities, bonds, even real estate all face headwinds. Commodities and energy seem to be the outliers.

High growth technology companies have been particularly affected.

This comes as no surprise – the multiple compression was inevitable. We mentioned it in an article published on March of 2021, SaaS Valuations Post COVID-19:

“The high multiples are unlikely to be sustained. Compression seems inevitable as growth and interest rates normalize.

The crucial component here is the timing, which is difficult to prognosticate. Whether multiple compression happens in a few weeks or over the span of a few years would make a significant difference. Considering the high revenue growth rates of many of these companies coupled with a sufficiently ample time horizon, investors can plan around the inevitable compression.”

Although that time has come, the bottom-up investment landscape looks promising. There is a lot of potential in our portfolio companies.

The majority of my research time goes into identifying the right businesses. I look to build true conviction in the company’s ability to execute. I look to understand the challenges and downside risks.

Only after understanding the business, I consider whether it is an appropriate time to purchase by looking at the valuation. In doing so, I tend to look out at least 5 years. I often build in significant compression into my expectations.

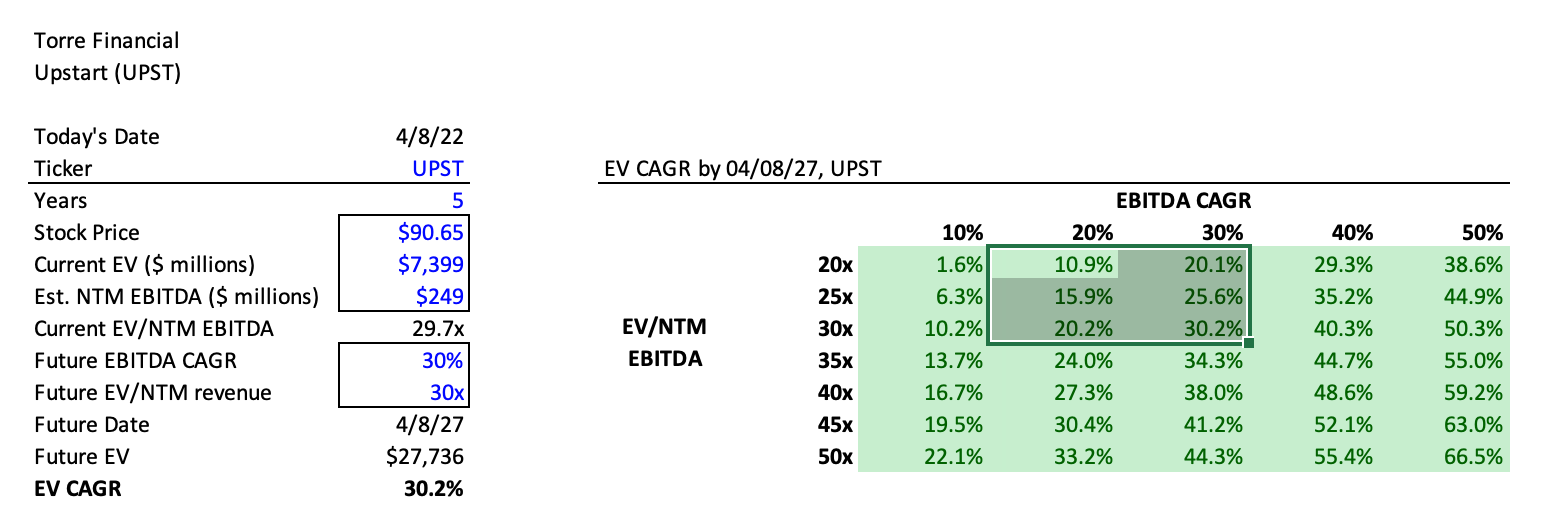

As an example, consider Upstart:

Upstart is a profitable business, with 250%+ revenue growth in 2021 and 65%+ growth projected for 2022. If Upstart is able to maintain its current (depressed) multiple of 30x EBITDA/EV and grow EBITDA at a CAGR of 30% over the next 5 years, an investor could be looking at annual returns of 30%. Even with multiple compression to 20x and 20% EBITDA CAGR, the investment could return 11% per year.

Given Upstart’s proven model, execution, and long runway, these outcomes do not seem unreasonable.

Rising rates do not invalidate a good business nor imply negative returns.

Related to rates – the Fed is under pressure from inflation to increase rates.

There may be a few potential forces that may help inflation subside with less intervention from the Fed.

Looking at year-over-year inflation rates, it is clear that the pandemic severely depressed inflation in 2020.

Given the comparison against extremely low rates in 2020, the inflation numbers for 2021 came in significantly higher.

April 2021 showed the first bump in inflation. With the year lapsing by, April 2022 will start being compared against higher numbers.

As long as prices are able to maintain somewhat steady, the headline inflation rate may begin to subside on its own.

Another potential force is in the driver behind prices — supply and demand.

Craig Fuller, a transportation and supply chain specialist, has a reason to believe that the market has reached saturation of goods. He shared observations about the trucking market via twitter, specifically noting an increase in trucks, increase in inventory, and a decrease in volume (perhaps indicating the tipping point). Saturation of goods in the market could help combat inflation.

Only time will tell how things play out.

If inflation does subside, the market could be end up pleasantly surprised.

As for my part, I will continue to stay focused on our portfolio companies and be on the look out for other exceptional businesses.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.