2025 Q1 Letter

Review of quarterly results, contributors and detractors, portfolio overview, and personal reflection

Torre Financial consolidated accounts declined 2.02% for the quarter. The S&P 500 (SPY) declined 4.27% over the same period.

SPY is an ETF tracking the S&P 500, an index of 500 companies. Torre Financial invests in 25-30 high quality companies. Returns for individual accounts may vary as each account is managed separately.

The following excerpt from our 2024 Q4 Letter turned out prescient:

“Markets, however, do not go up forever.

As we look forward to 2025, we are focusing on protecting our capital as we stay invested in high-quality compounders. Our portfolio is well set up to outperform in a weaker market.”

After climbing in January and February, the stock market pulled back in March. In April, the sell off accelerated into a full bear market with Trump’s tariffs.

The global economy is being challenged, as the Trump administration addresses the federal deficit and trade imbalances. Many American companies rely on international sales – they have outgrown their market in the USA and need to expand beyond. The current dynamic pressures the largest companies, including the Magnificent 7 which make up a large concentration of the indices.

Recently, the volatility index (VIX) has spiked above 50. Forward returns have been very favorable after such an event in the past, with average returns of +35%, +55%, and +129% the following 1, 3, and 5 year periods. These returns are significantly better than the average.

We’re well positioned and confident in our portfolio. We’re well diversified in the highest quality of companies. With higher than average gross margins, our companies are best equipped to handle any turbulence. We have some cash available that we will likely be deploying shortly.

Top Performers and Detractors

The following companies were the top performers in Q1 2025:

Abbott (ABT) +18%

Intercontinental Exchange (ICE) +16%

MercadoLibre (MELI) +15%

Visa (V) +11%

Agree Realty (ADC) +11%

These companies are from a broad variety of sectors. Abbott is a leading healthcare company, where demand is often distanced from economic influence. Intercontinental Exchange is a financial and data company, effectively offering risk management including specific hedging products. MercadoLibre is the leading e-commerce and financial platform in Latin America, quite distant from any impact due to USA tariffs. Visa is a high quality company, and unlikely to be challenged by themes dominating the current market scene. Agree Realty is a real estate investment trust, collecting rent from the high quality investment grade tenants – their cash flows are likely to remain very stable throughout any turmoil and the price is more affected by changes in the cost of capital.

The following companies were detractors to our performance in Q1 2025:

PayPal (PYPL) -24%

Salesforce (CRM) -20%

Alphabet (GOOGL) -18%

Adobe (ADBE) -14%

Amazon (AMZN) -13%

The detractors list has a clear theme: technology.

PayPal appeared to be staging a comeback in Q4, only to give up all the gains in Q1. The company is very cheap (~10% FCF yield!) and there is a lot of optionality (new ads business, Fastlane for faster anonymous checkout, etc). That being said, the concerns appear to be the fundamental core value of the offerings: consumers and merchants seeing the value in using PayPal. For consumers, that is reflected in regular transaction activity. For merchants, payment processing adoption. It is highly competitive. We reduced our position earlier in the year and are keeping a close eye.

Salesforce, Alphabet (Google), Adobe, and Amazon are operating steadily and caught up in global turmoil. International partners and customers have material implications to their businesses.

Another concern facing both Adobe and Alphabet is potential disruption from AI. It is driving and will drive significant changes as to how people work. It is automating a lot of work already across many functions including sales, marketing, customer service, and software development. There is opportunity for new leaders in this new space.

That being said, Adobe’s large enterprise customers require very specific solutions, controls, and configurations. Also, Adobe has been at the leading edge of AI solutions – within the enterprise context; not for the general public which may be splashier. The tightening of capital markets likely benefits Adobe, as it will focus capital on what is working instead of funding so many experiments.

For Alphabet, the concern is that the prized search model is being challenged. New incumbents such as OpenAI have grown quickly and dramatically. Some believe it will take away search traffic from Google. Over time, Alphabet has been able to show more and more of their potential with AI such as by integrating GenAI into search results, embedding Gemini into Google Workspace, evolving their AI infrastructure, and building out brand new AI products within Google Cloud Platform. They are a clear leader in driving AI forward.

Portfolio Overview

We are confident that our portfolio will do well in any market environment. We have some of the strongest businesses across various proven industries with attractive business models.

Our portfolio is well diversified across technology, healthcare, risk management, payments, e-commerce, travel, advertisements, enterprise efficiency, and defensive companies. Each of these are supported by compelling longer-term investment themes.

In big tech, we have Google, Meta, and Amazon. These companies continue to innovate and deliver amazing offerings, whether in their core business or upstart businesses including cloud and AI.

In healthcare, we have Abbott, United Health, Edwards Lifesciences, and Thermo Fisher Scientific. Healthcare adds resilience and stability, without sacrificing growth. Demand is increasing as the population continues to age.

In risk management, we have Intercontinental Exchange, MSCI, FactSet Research, Moody’s and S&P Global. These companies help their customers make better informed decisions. As market volatility increases, the value of these products increases, making them great antifragile components of our portfolio.

Enterprise efficiency includes Salesforce, Workday, Adobe, Intuit, ADP, and Veeva. These companies make it easier and cheaper for other companies to operate. As wages rise over time, their value proposition only strengthens.

Payment companies include Mastercard, Visa, and PayPal. The secular shift to digital transactions is still underway and has a lot of room to run. Because these companies take a slice of the transaction, they benefit from inflation as the gross merchandise volume increases.

In travel, we have two global leaders, Booking and Airbnb. Humans have an innate desire to travel. Experiences make for a rich life. Travel will benefit as middle classes grow across the world. Prices will go up over time (land, housing, wages), benefitting the marketplace business model of both Booking and Airbnb.

Defensive companies include PepsiCo in consumer staples and Agree Realty in real estate. These are high quality companies in their respective industries. While good investments on their own, they also serve as a counterbalance in times of significant market movement.

All of our companies exhibit strong returns on capital, competitive advantages, and durable growth.

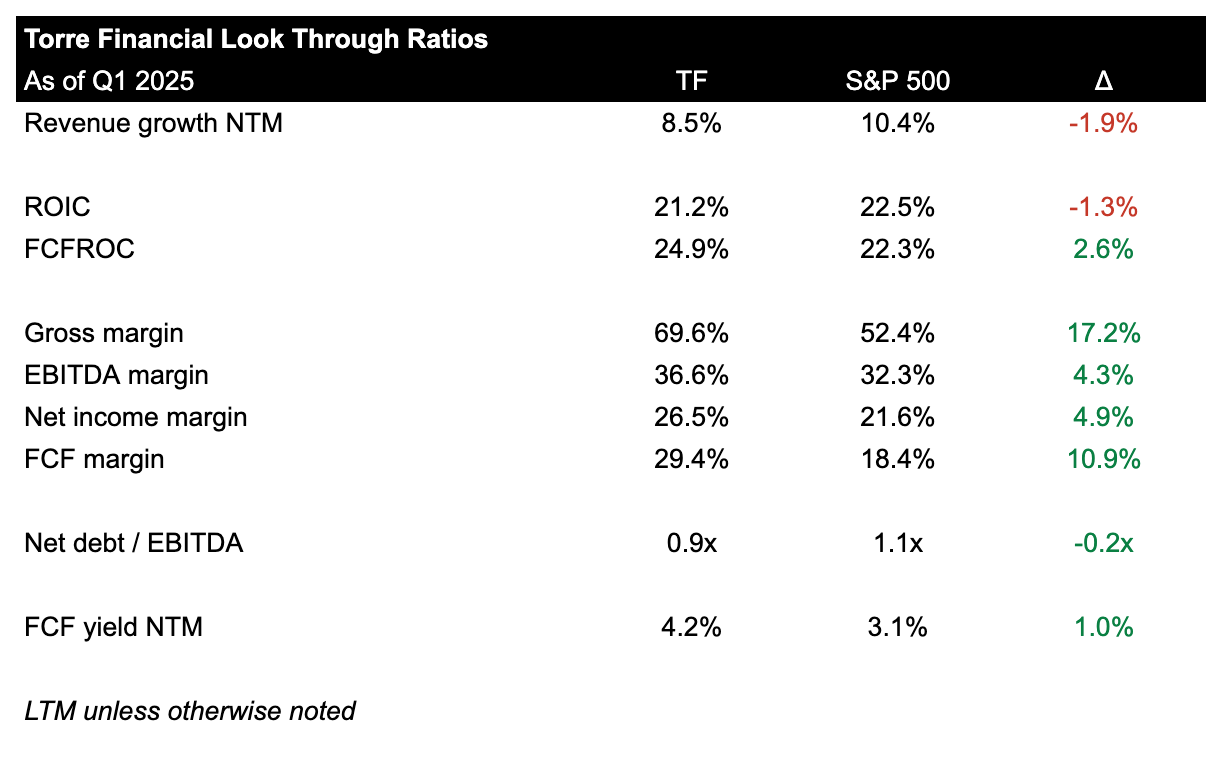

When compared to the S&P 500, our portfolio has:

Slightly lower revenue growth of 8.5% vs 10.4% for the index

Slightly less return on invested capital (ROIC) of 21.2% vs 22.5%

Higher free cash flow (FCF) ROIC of 24.9% vs 22.3%

Superior margins across the board

Less leverage (less debt, more resilient)

Significantly cheaper, with a FCF yield of 4.2% versus 3.1% for the index

It is worth noting that the index is highly influenced by Nvidia, which is likely at peak numbers.

We balance quality with appropriate valuation in order to protect our capital while staying invested.

After two calm years with strong market results, volatility has come back with vigor. While we don’t know what will cause future volatility, we know to always expect it. Volatility is the price of admission in the market. Our companies are more likely to come out stronger from any period of volatility, giving us confidence that our portfolio will come out ahead.

As always, we thank you for trusting us with your capital. Your commitment, confidence, and patience is essential for a successful partnership.

The Appendix below dives into detail on our portfolio management process including:

examining target weights over time

rationale behind each decision we make

companies on our watchlist

As well as our quarterly reflection on from the quarter including portfolio construction and our take on the current investing landscape.

Keep reading with a 7-day free trial

Subscribe to Torre Financial Newsletter to keep reading this post and get 7 days of free access to the full post archives.