Earnings Review - October 22, 2022

Market commentary, portfolio company earnings results, and a deeper dive into Intuitive Surgical (ISRG)

Earnings season unofficially kicked off on October 13th, 2022.

There’s a lot of attention on this quarter’s results and guidance, given the concerns of an impending recession.

Early results have skewed towards the positive side. Some examples of well known companies surprising to the upside include:

Goldman Sachs (GS) earned $8.25 vs $7.69 consensus

Johnson & Johnson (JNJ) earned $2.55 vs $2.48 consensus

Lockheed Martin (LMT) earned $6.71 vs $6.67 consensus

Netflix (NFLX) earned $3.10 vs. $2.17 consensus

Market reaction has been positive to companies posting positive results.

Needless to say, not every company is surprising to the upside. Snapchat’s parent company, Snap (SNAP), is one of the first digital advertising companies to report. Although Snap beat on earnings ($0.08 vs -$0.01 estimates), sales fell short of very low expectations. Shares fell 30%.

The market generally extrapolates signals to the broader industry. Snap’s difficulties in the online advertising market cause reactions in other ad-based companies such as Google, Meta, and The Trade Desk. The reaction was very marked last quarter. Snap finds itself in a particularly difficult situation with revenue growth quickly decelerating over the last few quarters (38% to 13% to 7%) and is now guiding for 0% revenue growth.

The Fed did not escape headlines this week. On Friday, the Wall Street Journal reported that the Fed would raise rates by 0.75 points in November and debate the size of future hikes. The market had been expecting 0.75 point increases in both November and December – this is the first hint at a possible easing up on the rate hikes.

Q3 2022 Results

Over the last two weeks, two portfolio companies reported earnings.

United Healthcare and Intuitive Surgical beat across the board. To be fair, expectations had come down since the last quarter.

Company Spotlight: Intuitive Surgical (ISRG)

“As part of our mission, we believe that minimally invasive care is life-enhancing care. We are committed to advancing minimally invasive care through a comprehensive ecosystem of products and services. This ecosystem includes systems, instruments and accessories, learning, and services connected by a digital portfolio that enables precision and control, seamless interactions and experiences, and meaningful insights to drive better care.” - ISRG, Q3 10-Q

Intuitive focuses on four dimensions: improving patient outcomes, improving the patient experience, improving care team satisfaction, and lowering the total cost to treat. Given the variety of stakeholders – hospitals, doctors, patients, and many more in between – it is critical they address the needs of each to build out a fruitful ecosystem.

Minimally invasive surgery (MIS) allows for complex operations to be conducted through small ports, rather than large incisions required for the alternative open surgery.

Intuitive’s da Vinci Surgical System enables surgeons to treat many more operations with MIS, leading to more predictable results with reduced trauma and better recovery.

Intuitive has a razor-and-blades business model, primarily generating revenue through

the sale of the da Vinci Surgical Systems ($0.5-2.5 million each)

recurring sales of instruments and accessories ($600-3,500 per surgery)

recurring services

Recurring revenue has increased from 72% of total revenue in 2019, to 75% of total revenue in 2021.

While Intuitive does not break out the gross margin contribution from sales of machines and instruments, it can be assumed that instruments and accessories, consumables per operation, are high margin sales. The more machines Intuitive is able to place, the more high-margin recurring revenue they will build over time.

The medical device industry is difficult to break into. From regulatory requirements to working with a variety of stakeholders, the barriers to entry are very high. With over 3 decades of operation, Intuitive has not only been able to innovate, but also build a successful and highly profitable business with a robust ecosystem. While some large medical companies are trying to compete, Intuitive has built a self-reinforcing network: hospitals are buying their systems; doctors are training and getting certified; patients are seeing better outcomes. The more doctors are trained on the da Vinci, the more likely hospitals are going to choose the da Vinci.

On to the financials:

The pandemic caused a setback, as surgeries and capital expenses were delayed. Intuitive has been able to work through it and maintain a strong business with both growth and impressive profitability.

Revenue has grown from $1.27b in Q3 2019 to $1.56b in Q3 2022, nearly 8% CAGR through a very challenging period.

Gross margins have been maintained in their historical range of 67-70%.

EBITDA margins have fluctuated between roughly 35-45%.

FCF margins have been between 18-24%, although most recently trending downwards.

In terms of efficiency, Intuitive is generating a strong FCF return on investments. Due to the significant amount of cash & equivalents on their balance sheet ($7.3 billion!), the invested capital ratio gives a better picture of the efficiency of the business operations.

FCF / invested capital is in the 27-37% range. For every dollar invested, Intuitive generates between $0.27-$0.37 in a year.

Zooming out over the last 20 years shows how Intuitive has been able to grow revenue and FCF in tandem. Efficiency coupled with growth is the trademark of a compounder.

As for more recent events, Q3 highlights include:

Da Vinci procedures growing 20% y/y, up from 14% y/y in prior quarter

305 da Vinci systems placed, representing 13% y/y growth & increasing the total installed base to 7,364

Repurchased $1 billion of common stock in Q3, on top of $607 million purchased in the first half. There is another $2.5 billion authorized under the current repurchase plan.

Procedure demand seems to be increasing, driving additional da Vinci system installs.

Highlights from the earnings call with CEO Gary Guthart:

“Our business fundamentals strengthened in Q3 with 20% procedure growth in da Vinci procedures compared with Q3 of last year and solid performance in each of our global regions.”

“Our capital placements reflected 13% growth in our installed base to meet procedure demand accompanied by continued increases in utilization per system per year, healthy indicators for our customers and for us.”

“Per system utilization grew 7% in the quarter, up from our three-year compound annual growth of 5% over the pandemic.”

“I will now turn to our financial outlook for 2022. Starting with procedures, on our last call, we forecast full year 2022 procedure growth within a range of 14% to 16.5%. We are now increasing our forecast and expect full year 2022 procedure growth of 17% to 18%.”

“Our teams continue to work closely with hospitals, physicians and care teams in pursuit of what our customers have termed the quadruple aim, better, more predictable patient outcomes, better experiences for patients, better experiences for their care teams, and ultimately, a lower total cost of care.”

“We believe value creation in surgery and acute care is foundationally human. It flows from respect for and understanding of patients and care teams, their needs and their environment. At Intuitive, we envision a future of care that is less invasive and profoundly better, where diseases are identified earlier and treated quickly so patients can get back to what matters most.”

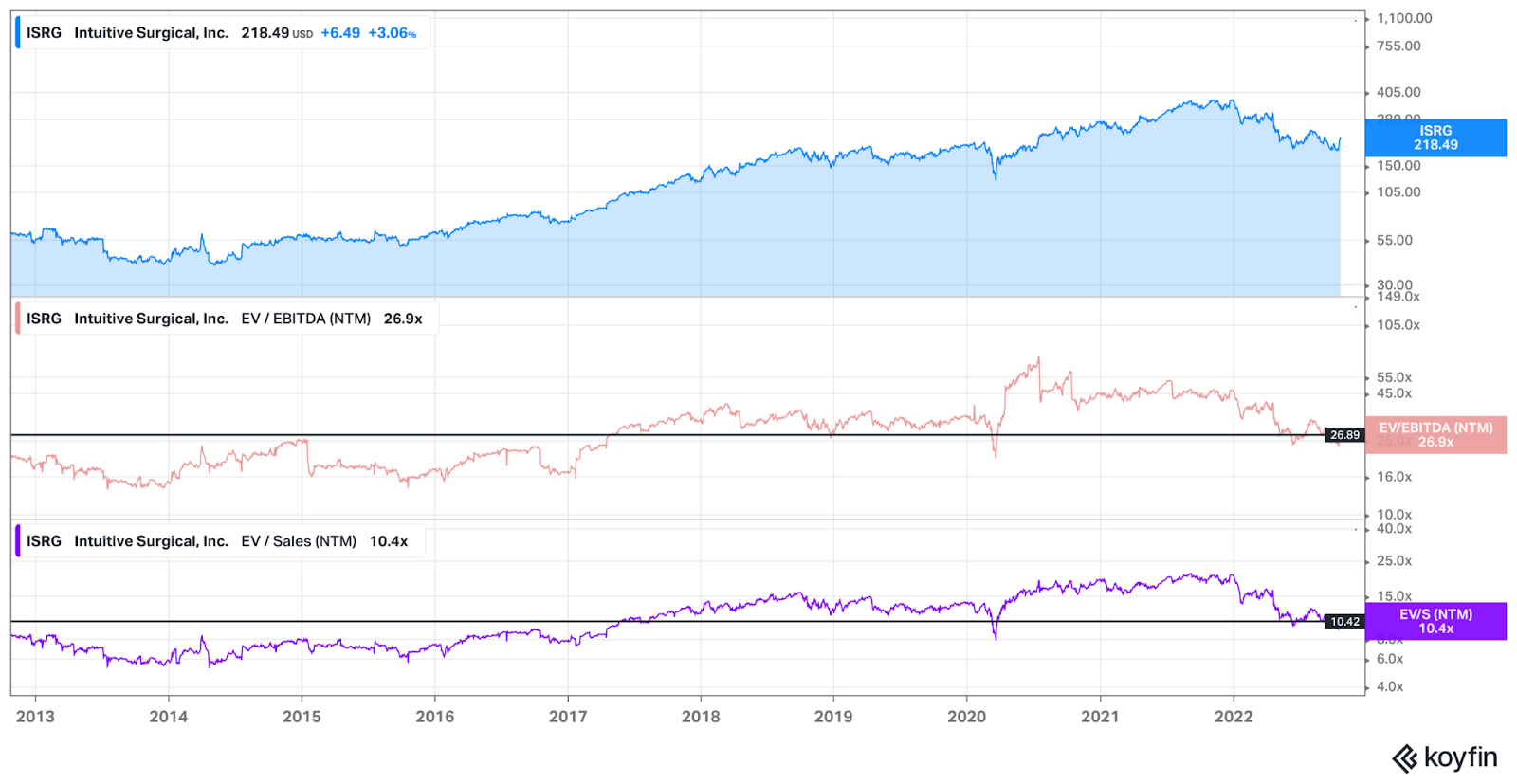

Intuitive’s valuation has come down over time. Both EV/EBITDA and EV/S multiples seem to demonstrate fair value. The multiples are above the average from 2013-217, but below the average from 2018-2022.

For a different perspective, we can look at possibilities 5 years out across EBITDA growth and multiple.

If over the next 5 years, Intuitive is able to

Grow EBITDA 10% per year and trade at a 25x multiple, that would yield a 8.4% CAGR

Grow EBITDA 15% per year and trade at a 25x multiple, that would yield a 13.3% CAGR

Grow EBITDA 15% per year and trade at a 30x multiple, that would yield a 17.5% CAGR

While it is impossible to predict the future, this framework seems to imply the shares look to be, at least, fairly valued.

Closing

While Q3 results have generally been positive, it is still early. Only 20% of the S&P 500 companies have reported so far.

Next week, over a quarter of the S&P 500 companies will be reporting earnings, including big tech and many more. Portfolio companies reporting include Google, Visa, Moody’s, Microsoft, Meta, ServiceNow, Stag Industrial, Mastercard, and Amazon. Stay tuned for updates.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.