Earnings Roundup 5.7.2022

Review of recent earnings activity plus commentary on Paycom, Datadog, and Cloudflare

Earning season unofficially kicked off in early April, as the big banks began sharing their results.

The following Key Metrics from Factset’s Earnings Insight on May 6th, 2022 give a good overview of where things stand today:

“Earnings Scorecard: For Q1 2022 (with 87% of S&P 500 companies reporting actual results), 79% of S&P 500 companies have reported a positive EPS surprise and 74% of S&P 500 companies have reported a positive revenue surprise.

Earnings Growth: For Q1 2022, the blended earnings growth rate for the S&P 500 is 9.1%. If 9.1% is the actual growth rate for the quarter, it will mark the lowest earnings growth rate reported by the index since Q4 2020 (3.8%).

Earnings Revisions: On March 31, the estimated earnings growth rate for Q1 2022 was 4.6%. Ten sectors have higher earnings growth rates today (compared to March 31) due to positive EPS surprises and upward revisions to EPS estimates.

Earnings Guidance: For Q2 2022, 50 S&P 500 companies have issued negative EPS guidance and 22 S&P 500 companies have issued positive EPS guidance.

Valuation: The forward 12-month P/E ratio for the S&P 500 is 17.6. This P/E ratio is below the 5-year average (18.6) but above the 10-year average (16.9).”

Portfolio Overview

The last few weeks have been busy, with many companies announcing their results in late April and early May.

The table below summarizes the performance of portfolio companies thus far, followed by a few highlights.

Paycom

Paycom provides cloud-based human capital management software solutions, including payroll and other human resources functions.

Paycom reported first quarter revenues of $354 million, up 30% year over year and fairly above the $342-344 million guidance that was shared in the fourth quarter.

Key metrics across the board seem to be going in the right direction for Paycom.

As for forward guidance, Paycom expects revenue in the range of $308-$310 for Q2. Note that Q1 benefits from increased activity related to reporting taxes. The mid-point of the guidance represents 27.6% year-over-year growth when compared to prior year’s Q2 revenue of $242.1 million.

Full year revenue guidance was raised to $1.333-1.335 billion, up from the $1.314-1.316 billion guidance in the last earnings call. This would represent 26.5% year over year growth for fiscal 2022.

This unique combination of healthy margins and revenue growth is a fundamental characteristic of compounders.

Highlights from the earnings call with founder and CEO Chad Richison:

“This quarter has set us up really well to strong financial performance for the remainder of the year and we are raising our full year guidance as a result. With our new full year outlook for revenue growth and adjusted EBITDA margin, I now believe we can exceed the Rule of 65.”

“Employee usage continues to trend higher as more companies embrace our self-service solutions and push ownership of the data out to the employee. Increasing employee usage is a key component of the ROI that our clients realize and we believe our employee usage strategy is a competitive advantage and a driver of our very strong growth.”

“Beti is fundamentally a better way to run all payroll processes to the benefit of the employer and employee. We will continue to innovate Beti to deliver even more value to our clients, making it even more compelling. Beti is the future of payroll.”

“Just a few years ago, we celebrated leading sales reps who sold over $1 million in a year. Today, we are celebrating sales reps exceeding $2 million in sales in a year.”

“As a reminder, we only have approximately 5% of a very large and growing TAM and a long runway for rapid growth for many years to come.”

“The strength of our results and our raise guidance clearly reflect our confidence in the market demand for our solutions and the success we are having in expanding our market share from the roughly 5% share of the TAM that we have today. We have a high margin recurring revenue model, a strong balance sheet, and with the investments we are making and the success of our sales model, we are very well positioned to deliver another year of rapid revenue growth and robust adjusted EBITDA margin.”

“[Regarding interest rates] We had a 25 basis improvement towards the end of first quarter. … The guidance we gave is really kind of where we are today on what we're earning today. So that included that first 25 basis point increase. So, they're talking about additional raises even this week. So we kind of have to see how those layer into our earnings.”

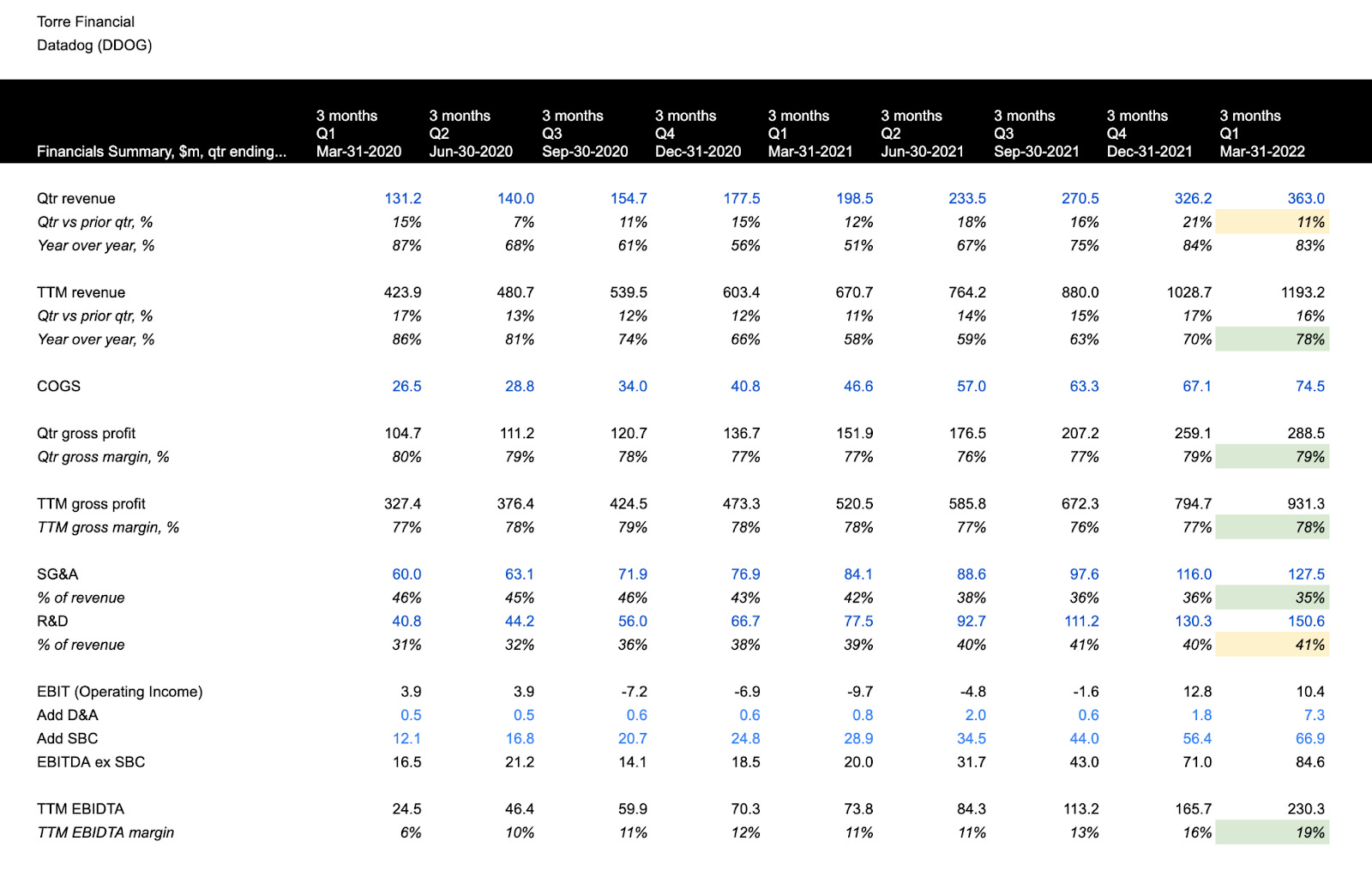

Datadog

Datadog provides solutions to help monitor and secure cloud-based applications.

They reported another quarter of strong results, continuing to benefit from the secular tailwinds driving digital transformation.

Revenue for Q1 came in at $363 million, an increase of 83% year over year. The company reported $129.9 million of free cash flow, representing 35.7% free cash flow yield.

Although quarter-over-quarter sales growth showed a deceleration, Datadog continues to show strong performance.

As for guidance, they expect revenue between $1.60-1.62 billion for the year, which would represent 57.5% growth over prior year’s $1.029 billion.

Datadog has been able to consistently deliver above expectations.

Highlights from the earnings call with co-founder and CEO Olivier Pomel:

“We are seeing strong efficiencies in our business model with free cash flow of $130 million and free cash flow margin of 36%. And our dollar-based net retention rate continued to be over 130% as customers increased their usage and adopted our newer products.”

“At a high level, we saw positive business trends in Q1. Usage growth from existing customers was strong and consistent with historical trends as customers continued on their cloud migration and digital transformation journeys, and the Datadog platform continued to expand and deliver more value. New logo ARR was very robust and churn remained low and in line with historical rates.”

“Next, our platform strategy continues to resonate in the market. As of the end of Q1, 81% of customers were using 2 or more products, up from 75% a year ago. 35% of customers were using 4 or more products, up from 25% a year ago. And 12% of our customers were using 6 or more products, up from 4% last year.”

“Remember that we are still in early stages with our security efforts and have much to do to further build out this product, but we are pleased with our progress so far and the usage we are getting from our customers.”

“We keep improving on those partnerships and developing them. I think we've announced this quarter some improvements to our Azure partnership, for example, where we are now part of the Golden Pass presented by Azure for migrating to the cloud. And we're seeing some great customers onboarding, thanks to that.”

Cloudflare

Cloudflare, with the mission of building a better internet, has become a key player in the next generation infrastructure of the internet.

For Q1, they reported revenue of $212.2 million, an increase of 54% year over year. While they have demonstrated positive free cash flow in the past, for Q1 free cash flow was negative $64.4 million as they continue to invest heavily in the business.

Growth and gross margin metrics are headed in the right direction. The consistent, sustained revenue growth hovering around 50% is quite remarkable.

As for guidance, Cloudflare expects revenue of $955-959 million for the full year, representing growth of 46% versus the prior year’s $656 million.

The 46% year over year growth does signal a drop below the historical sustained growth rates.

Similar to Datadog, Cloudflare has consistently beat expectations in the past.

Highlights from the earnings call with co-founder and CEO Matthew Prince:

“Our land and expand motion continues to improve, with dollar-based net retention hitting a new record of 127% in the quarter, up 400 basis points year-over-year. New products and an increased interest in consolidating behind a single trusted vendor for network services has been the key to our continued customer expansion.”

“Efficiency has always been a hallmark of our business. And even in these inflationary times, we achieved a gross margin in the quarter of 78.7%, up 110 basis points year-over-year. That continues to be above our target gross margin range of 75% to 77%, and affords us the opportunity to selectively target competitors' customers, offering them bundles of products that work seamlessly together, reducing the number of vendors they need and providing them with modern solutions, all while saving them money at the same time. We are finding this is an especially compelling value proposition when it seems everyone else is raising prices or can't even say for certain when they'll be able to deliver their legacy hardware boxes.”

“We closed our largest acquisition ever in the quarter, buying Area 1 Security for $162 million. We have a very high hurdle rate for acquisitions being strongly biased towards internal development but Area 1 technology and team are special. We started out as a customer. I remember shortly after we implemented their solution, writing to our Chief Security Officer to ask if something was wrong, I hadn't seen any phishing reports in a few weeks, where usually our team would report double digits per day. It turned out Area 1 and their incredible e-mail security tech was the answer. … E-mail is the #1 source of network threats. That no leading zero trust vendor has truly integrated e-mail security is a major blind spot the industry was guilty of.”

“It turns out doing the right thing and being there when some on the Internet needs us has always been core to Cloudflare and has always turned out to be good business for us over the long term. It's why I love my job.”

“As mentioned last quarter, we expected to see some cash flow variability in the first half of 2022, but we continue to expect to return to positive free cash flow in the second half of this year. Remaining performance obligations, or RPO, came in at $688 million, representing an increase of 10% sequentially and 57% year-over-year. Current RPO was 76% of total RPO.”

Closing

This earning season has been challenging to navigate. Companies that fall short of expectations are seeing drastic negative reactions. Many companies that beat expectations for earnings, revenue, and are even raising guidance have also seen negative reactions in their share price.

The market seems to be more sensitive to macro concerns, such as inflation, supply chain issues, and interest rates, than the performance of companies. The negative sentiment is driving prices down via multiple compression.

Similar to the fact that interest rates could not stay at 0% forever, multiple compression will not continue indefinitely.

Whereas the last few years growth received a lot of the attention, now valuation and profitability has come to the forefront.

While short term price action can be concerning, it is important to focus on the destination. The companies that are building fundamentally sound businesses, are creating value for their stakeholders, and continue to execute well will ultimately be recognized by the market.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.