Earnings Roundup 6.4.2022

Commentary on the macro environment, review of recent earnings activity, recap of earnings from Salesforce (CRM), Veeva (VEEV), and Crowdstrike (CRWD)

Tale of two paths

There seems to be divergent opinions about the path for the economy, and the market, over the next 6 to 12 months.

Path 1: Inflation continues to climb

On one side, some people believe inflation will continue climbing. Driven by oil and global supply chain issues, inflation will become sticky and can begin to spiral. Higher prices will lead to higher wages which will lead to higher prices, and so on.

In order to avoid this situation, the Fed will have no choice but to raise rates aggressively.

There has been a severe decline in crude oil storage, pointing to higher consumption than production. This could put upwards pressure on gas prices.

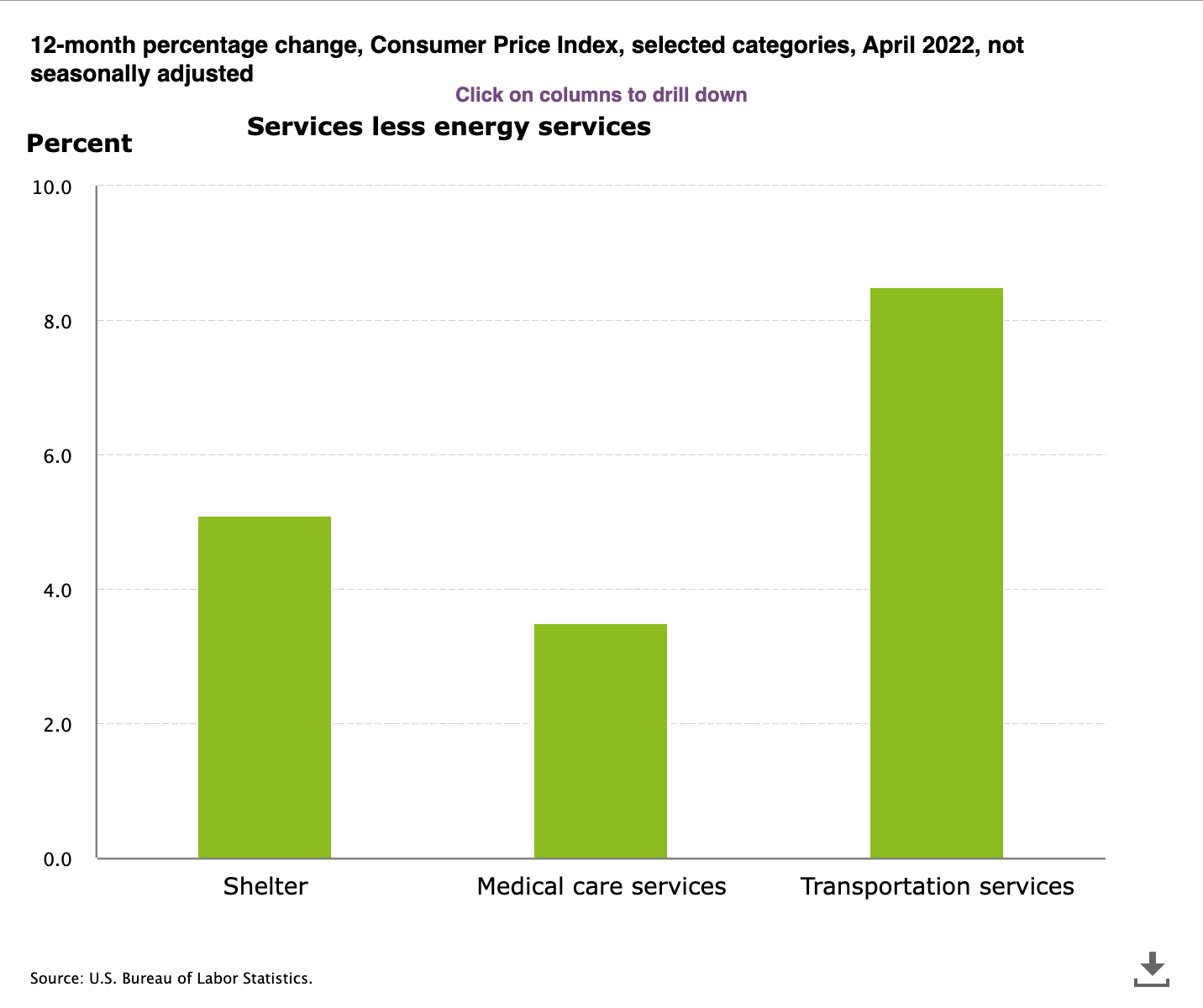

This in turn has led to significant price increases for transportation services, which continue to see 8%+ year-over-year inflation. Inflation for shelter, which is considered very sticky, is also elevated.

In addition to pricing pressures, the economy seems to be slowing down.

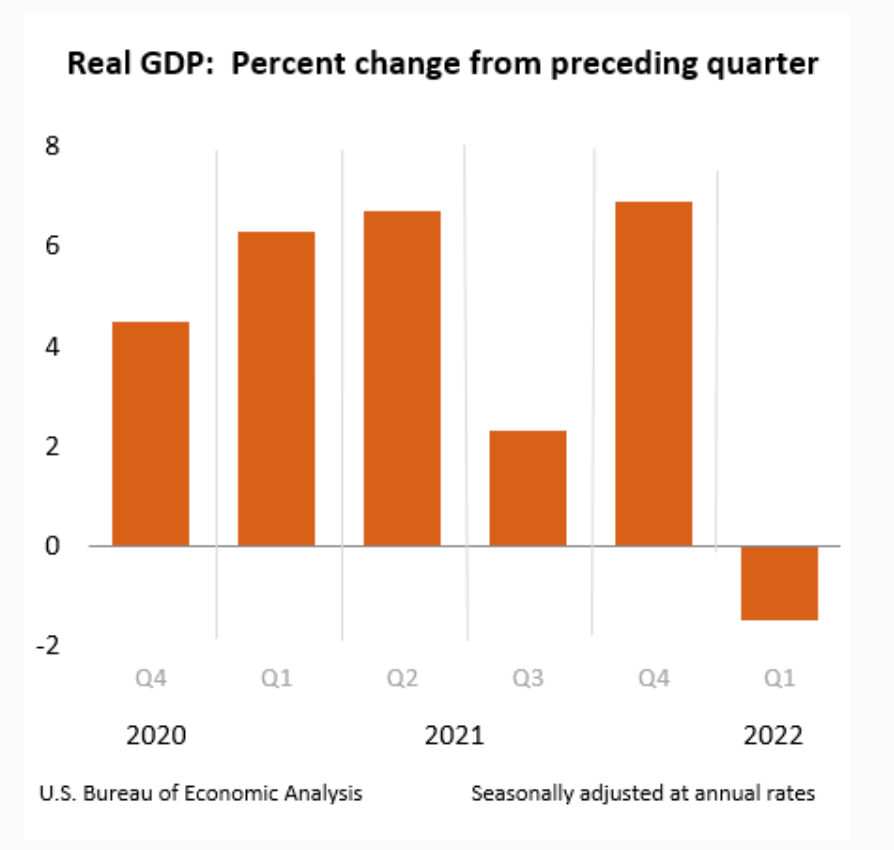

For Q1 2022, GDP decreased at -1.5%. A recession is defined as two quarters of negative GDP growth.

The combination of slowing, or stagnant, economic growth and high inflation is known as stagflation.

Stagflation is a challenging situation: growth is slowing and the Fed is not in a position to help – to the contrary, the Fed would likely be forced to increase rates, further hampering any growth.

Path 2: Inflation subsides

On the other side, there is the notion that inflation will begin to subside on its own.

The Fed, through their rhetoric and initial hikes, has already gotten the desired reaction. The excesses in the market have corrected, reducing the wealth effect & suppressing demand.

One example: mortgage rates are up dramatically, climbing from 3% to over 5% year to date, leading to a slowdown in housing sales.

That being said, the proponents of subsiding inflation believe the current inflation is not driven by demand-side, but by supply-side constraints. And, the Fed raising rates doesn’t help supply side issues.

On the supply-side, there is already a build up of inventory in retail goods. Inventory is at a historical high, significantly above trend, as companies are re-learning supply chain management post-COVID. The excess inventory will likely lead to markdowns and lower prices.

According to the U.S. Bureau of Labor Statistics, the entity that publishes the CPI report, the relative importance of the “all items less food and energy” is 78%, with food at 13%, energy at 8%, and services at 57%. Hence, retail inventory could move the needle.

Some experts forecast inflation ending the year in the 3-4% range. If inflation does begin to slow down, the Fed could begin to soften their tone. If the Fed ends up being less aggressive than the market expects, that could benefit equities broadly.

How to proceed from here…

It is impossible to know how the future will unravel. That being said, monitoring the data can give insights into which direction things are headed.

Sentiment is now at a record low.

Energy executives have started selling shares. They tend to be pretty accurate in timing optimism. This can be an indicator of a turn. Many tech executives began selling shares in Q3 and Q4 last year.

Cestrian Capital reports that the S&P 500 has hit a critical retracement level and claims it is poised for a move upwards.

Notwithstanding the plethora of concerns, both the Nasdaq and S&P 500 bounced off lows set on May 20th.

Is the tide turning?

The jury is still out whether this will be the bottom or whether the market retests the lows. The price action over the ensuing weeks should be revealing.

Investing isn’t always easy, but has always been rewarding in the long-term. Akre Capital stated it well in a recent article – Why Compounding is so Difficult.

Q1 2022 Earnings

The table below summarizes the performance of portfolio companies thus far. Earnings and revenue results are assessed against consensus estimates.

Over the last two weeks, the remaining 6 portfolio companies reported earnings: Intuit (INTU), Salesforce (CRM), Workday (WDAY), Veeva (VEEV), Crowdstrike (CRWD), and Okta (OKTA). A few results are highlighted below.

Salesforce (CRM)

“Salesforce is a leading provider of enterprise cloud computing solutions, with a focus on customer relationship management, or CRM. We introduced our first CRM solution in February 2000, and we have since expanded our service offerings with new editions, solutions, features and platform capabilities.

Our mission is to help our customers transform themselves into customer-centric companies by empowering them to connect with their customers in entirely new ways.” - Salesforce 10-K

Salesforce pioneered the software-as-a-service delivery model.

For Q1 FY2023, Salesforce reported revenue of $7.41 billion, up 24% year-over-year, and operating cash flow of $3.68 billion, up 14% year-over-year. The operating cash flow represents 49.6% of revenue.

EBIT operating margin was up versus the prior quarter, demonstrating improving efficiency during a difficult period.

With 27% free cash flow margins and $13.5 billion in cash, Salesforce is well positioned to take advantage of any market turbulence.

In terms of guidance, Salesforce decreased full year guidance from $32 billion to $31.7-$31.8 billion, citing a $600 million headwind from the strong dollar. The 20% annual growth is a slow down from their previous 25% rate.

That being said, current remaining performance obligations (cRPO) stood at $21.5 billion, growing 21% year-over-year. The entirety of their remaining performance obligations (RPO) are $42 billion. As a reminder, RPO measures sales that have been contracted but not yet recognized.

Salesforce’s main product, initially built over 20 years ago, continues to be more relevant than ever.

Additionally, Salesforce has fared well with strategic M&A, acquiring fast growing companies and leveraged their enterprise distribution platform.

Highlights from the earnings call with founder and CEO Marc Benioff:

“We're quite committed to consistent margin and cash flow growth as part of this long-term plan and model that we have to drive both top and bottom line performance. And as I said, this demand environment for our Customer 360 platform, as you're about to hear from Bret and from Gavin and from Amy and from others as well, it remains incredibly healthy.”

“So let me say that this is a time when every company, every industry, every government is investing in digital transformation, no company is better positioned than we are to help companies transform for the digital future.”

“I want to start by talking about the strong demand environment we're in. As Bret and Marc said, even in this volatile environment, companies are continuing to invest in their digital transformations, and we're seeing that in our strong pipeline and momentum in the business. I've been on the road this quarter across the U.S., Europe, Asia and most recently in Davos. And in all my conversations, there is a real sense of urgency with our customers. In this new or digital work-from-anywhere world, our customers need to create incredible customer experiences across every interaction to stay competitive. And at the same time, they need to realize productivity gains, efficiencies and resilience from their technology investments. … We're seeing this play out in the growth of transformational deals, customers making longer-term multi-cloud investments in Salesforce.”

“We're really excited about Sales Cloud growth. Not only did it grow 18% year-over-year in the quarter, but in constant currency grew 20%, which I think is a symbolic threshold or as you said, the product that Marc and Parker built 23 years ago, it is still as relevant today as it ever has been.”

“It's really driven by disciplined decision-making and trying to really unlock incremental efficiencies across the entire business. We've asked each leader to step up to really look across their business and to strategically prioritize their investments. And this is really to make sure that we're getting the highest return for every dollar that we invest.”

Veeva Systems (VEEV)

Veeva is a leading global provider of industry-specific, cloud-based software solutions for the life sciences industry. Serving pharmaceutical, biotech, and other life science companies, Veeva gives them a path to realize the benefits of modern cloud-based architectures and mobile applications without compromising industry-specific functionality or regulatory compliance. Veeva’s CEO, Peter Gassner, was SVP of Technology at Salesforce prior to founding Veeva.

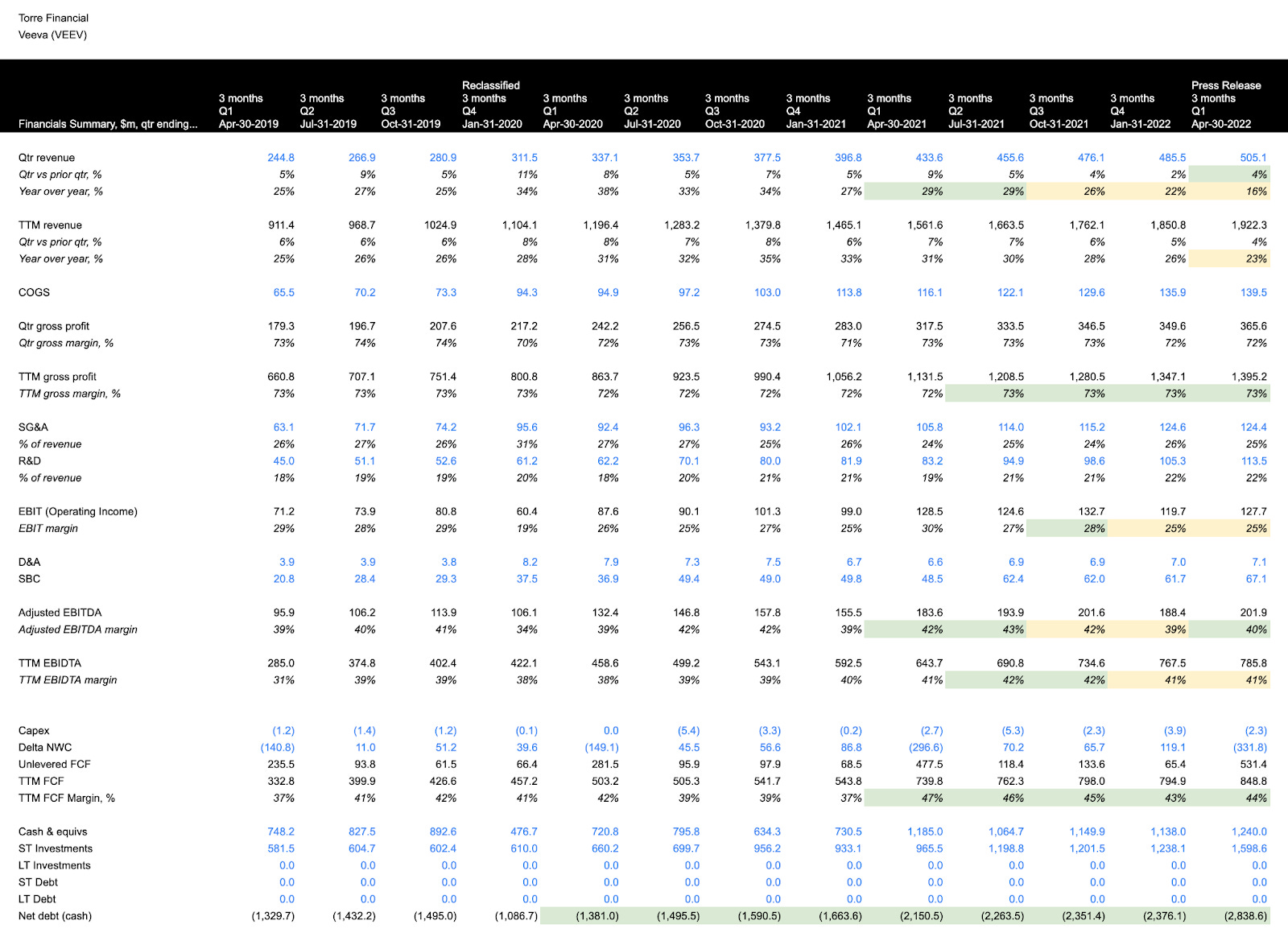

For the first quarter, Veeva announced revenue of $505 million, up 16% year-over-year, and GAAP net income of $100 million for a net margin of 20%.

For the full year, Veeva is guiding for revenue of $2.165-2.175 million, representing 17% growth year over year. They expect $835 million in non-GAAP operating income, or adjusted EBITDA, representing a margin of 38.5%.

Veeva is a stable, durable, and highly profitable business. They have a strong foothold in the life sciences industry, which would be very difficult to displace, and they continue to innovate and expand their offerings. Veeva’s balance sheet is strong, and growing stronger as they build cash quarter after quarter, giving them flexibility and options for the future.

Highlights from the prepared remarks and earnings call with founder and CEO Peter Gassner:

“This quarter we reached a $2 billion revenue run rate with strong profitability and high durability.”

“We started on the software side, and the bulk of our business is still in software, but data and consulting are starting to play more significant roles today and this trend will continue as we move forward.”

“In R&D, we are making progress on our vision to establish Veeva Development Cloud as the operating system for drug development. In the quarter, a top 20 pharma selected Veeva Development Cloud to help streamline and accelerate the development of innovative medicines. Spanning 12 products across clinical, quality, and regulatory, it’s one of our largest deals ever, and a landmark for Veeva and the industry. While it’s not typical for a top 20 to go all in across so many areas of R&D all at once, we increasingly see companies partnering with us deeply in this way on a long-term vision and roadmap for drug development.”

“It’s early days for Veeva in R&D. We’re only 15% into our current $7 billion total addressable market opportunity. There is a long tail of growth ahead for our established products and we have a number of major products very early in their lifecycle like Vault CDMS and Vault Safety.”

“So we do have $2.8 billion in cash and our business model has consistently been able to generate cash. So, we're very pleased with that. And our focus is primarily to invest for growth. And specifically, we're going to be looking at ways like M&A to – for use of our cash, right? But we're going to take a disciplined approach as we look at M&A.”

“Yes. Clinical is certainly a long runway. It's a very big area of life sciences. … And we're there now with eTMF, and there's a network of -- a network effect … Probably the next furthest along is our CTMS and study start-up products. They’re getting to be pretty dominant products. And then the clinical data management is yet to come. That's very early in its life cycle, CDMS, the clinical data management. And beyond that, you have the digital trials, the MyVeeva for Patients, things right out to the patients…. So, a really long runway of growth in clinical. It's a big critical area. And macro level, we're just getting started there. And you're right, eTMF is a very strong base, because that's the foundational system of record of documentation for a clinical trial that every pharmaceutical company is required to have.”

“People feel that, and so there's a flight to quality. So, hiring has been a bit easier for us. So, in summary, I'd say it's a good hiring environment, and we certainly don't have any hiring freeze.”

CrowdStrike (CRWD)

A leader in the cloud-native cybersecurity space, CrowdStrike pioneered the Security Cloud with their AI-driven endpoint security protection.

For the first quarter, CrowdStrike reported revenue of $487.7 million, a year-over-year increase of 61%. Levered free cash flow grew 34% year-over-year to $158 million, representing 32% of revenue.

CrowdStrike raised guidance for the year, now expecting full year revenue of roughly $2.2 billion, an increase of 52% year-over-year.

CrowdStrike has always maintained a keen focus on innovating and creating new offerings, with now 22 distinct modules to sell into new and existing customers, as well as constantly improving on their go-to-market strategy.

CrowdStrike’s platform is resonating with the market, fueling the strong growth. Their market share has grown consistently: 7.9% in 2019, 12.2% in 2020, 14.2% in 2021.

Highlights from the earnings call with founder and CEO George Kurtz:

“We believe our Q1 results exemplify that we have a winning formula that includes scale, growth, profitability and free cash flow.”

“We saw strength across the platform, including a record quarter for modules deployed in the public cloud and over 100% year-over-year ending ARR growth for our emerging product group, which includes our Discover, Spotlight, Identity Protection and Log Management modules”

“We are seeing more and more customers standardize on the Falcon platform. The number of customers adopting 6 or more and 7 or more modules, both grew more than 100% year-over-year. We believe this underscores our wide competitive moat and our opportunity to drive long-term sustainable growth in both, our core and expansion markets.”

“In 8 out of the last 10 quarters, we have delivered 30% or greater free cash flow margin. Our powerful combination of growth, profitability and cash flow is reflected in our continued performance well in excess of the SaaS industry’s Rule of 40 benchmark. In Q1, we achieved a Rule of 78 on a non-GAAP operating income basis and when calculated on a free cash flow basis, a Rule of 93.”

“The demand environment we see is more robust today than this time last year as cybersecurity is not discretionary. Additionally, the competitive environment has remained favorable to CrowdStrike.“

“In Q1, subscription customers with 4 or more, 5 or more and 6 or more modules increased to 71%, 59% and 35%, respectively. Given subscription customers with 4 or more modules surpassed the 70% milestone and is now commonplace, we are retiring this disclosure and raising the bar by introducing a new metric, customers with 7 or more modules, which reached 19% at the end of Q1. We are pleased with our strong module performance across the Falcon platform in both, our core and expansion markets.”

Closing

Despite the challenging macro environment, portfolio companies continue to grow and demonstrate impressive results.

Fundamentals tend to be much more stable and predictable than price action, which can be noisy and volatile.

As long as there is no fundamental change to the underlying business and the original thesis stays intact, investors may be best served by staying the course and being patient. When it comes to investing, patience, and even inaction, can be a valuable competitive advantage for an investor.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.