Market & Earnings Review - June 10, 2023

Market commentary, portfolio company earnings results, and closer look into Zscaler (ZS)

Market

The S&P broke out to the upside, overcoming the critical 420 level which had been previously met with stiff resistance. The market looks to be building support, with the trendlines moving favorably. The August 2022 high of 435 appears to be the next level to watch.

Jobs and Wages

Dispelling recession calls, the job market remains resilient. ADP payroll report showed 339,000 jobs were added in May, significantly clearing consensus expectations of 190,000.

Wage growth for May came in at 0.3%, in line with consensus. Wages are up 4.3% over the last year, not quite keeping up with inflation.

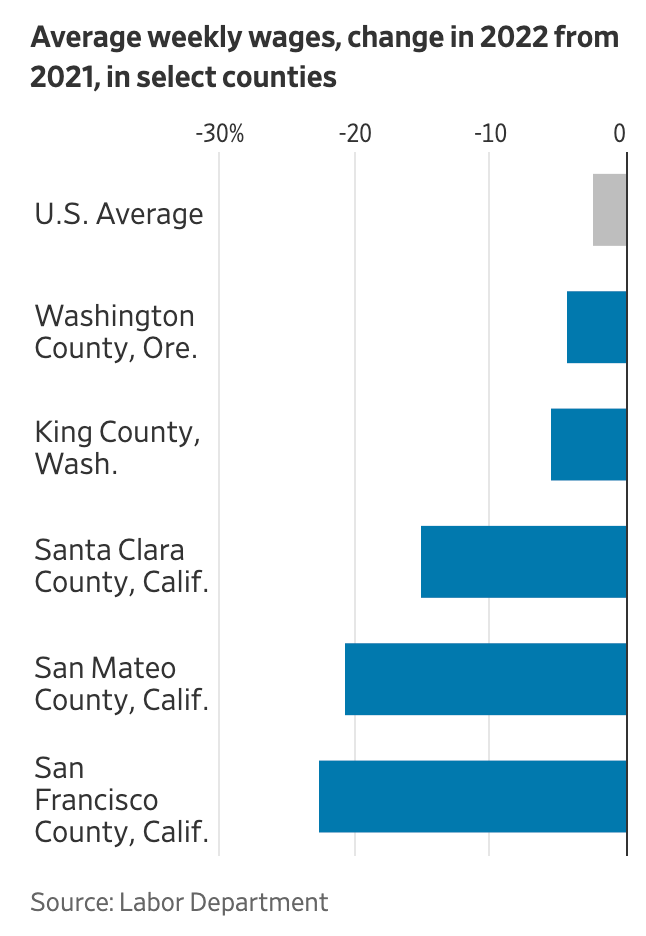

Not all areas are experiencing wage growth. Areas with high paying tech jobs have seen significant changes including mass layoffs and remote work. The result: wages are down. In San Francisco, average weekly wages are down 22.6% from a year ago. In Seattle, wages are down 5.4%.

Inflation

Inflation continues to subside. Leading indicators suggest US Core CPI could be in the 3% area by December. Inflation could come down to a high 2% in 2024.

With the exception of sugar, commodities are down 15%+ over the last year.

Shelter, as measured for the CPI, tends to lag negotiated rents. With the most recent CPI report showing the inflection point, the shelter component is likely to continue with a rapid decline.

Services have been another sticking point in recent inflation. Inflation in goods slowed down as consumption shifted to travel, restaurant, and other services. While services prices have been resilient, they appear to be moderating to below 3% shortly.

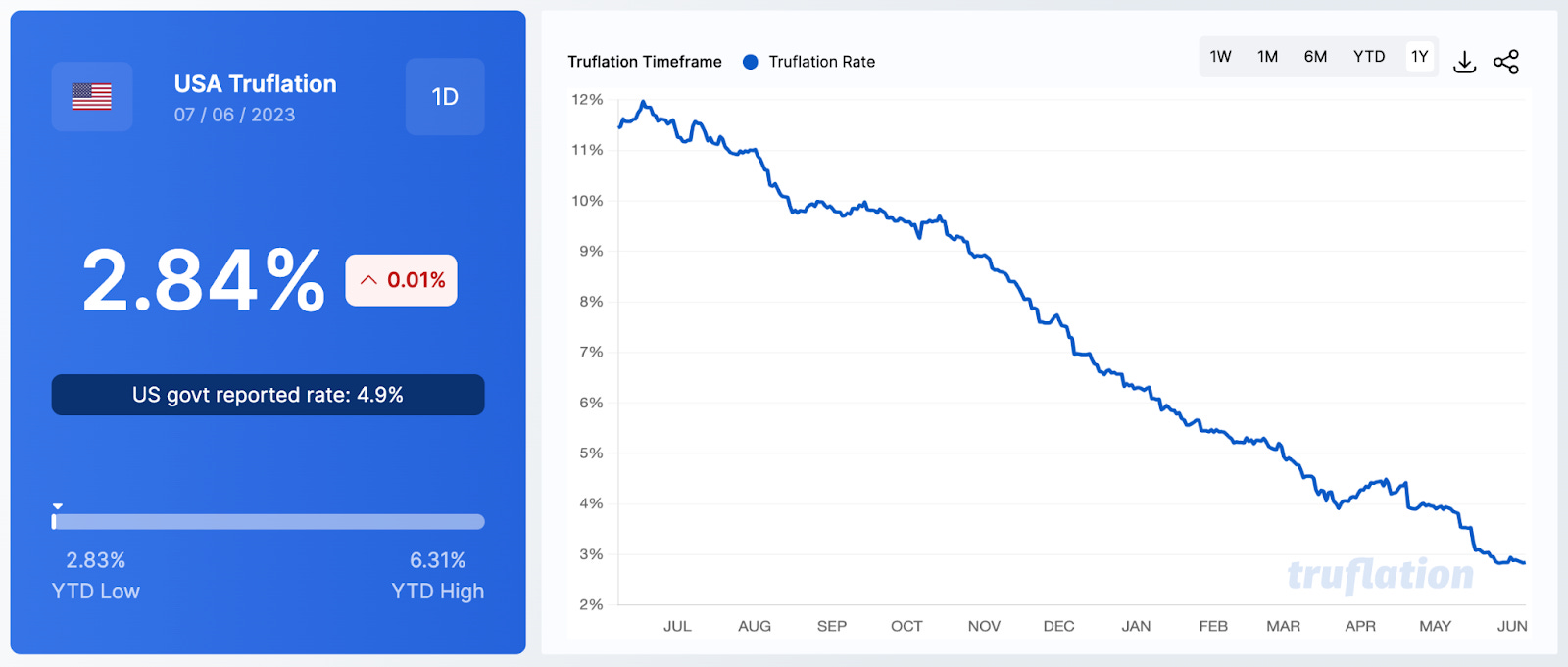

The leading indicators above coincide with the Truflation number.

“Truflation offers a more reliable view of inflation, contrasting with government metrics that have outdated methodologies and limited transparency. With over 10 million data points, it updates daily and has a dynamic and transparent methodology that responds to global market conditions.” For more about the methodology, see https://truflation.com/methodology.

Truflation marks inflation at 2.84% compared to CPI’s 4.9%.

Yields

After a tumultuous 2022, the bond market has generally steadied in 2023. The recent uptick in yields since April may be acknowledgement of the Fed’s “higher for longer” policy guidance.

Markets are expecting the Fed to pause in June, with a possibility of further hikes in July and September.

Business impact

Higher yields had a significant impact on the economy. Bankruptcies have started ticking up in 2023, coming in at nearly double the pace of 2022.

Given the recent failures, regional banks have been in the spotlight the last few months. Banks can expect more regulation going forward.

Commercial real estate is seen as the next area of concern. There are about $1.5 trillion in commercial mortgages coming due over the next 3 years. The vast majority (88%) are interest-only loans, wherein the principal must be repaid in a lump sum at the end. To make those payments, owners usually obtain new loans or sell the asset. Much higher financing costs, a less liquid market, and lower asset prices pose challenges ahead.

Office commercial real estate is particularly troubling. Vacancy rates on office space across the U.S. hit a record 16%. In certain cities, it is worse. Downtown office space in Los Angeles is seeing 30%+ vacancy.

Money supply

With the debt ceiling agreement in place, the government is looking to sell over $1 trillion of bonds by the end of the year to replenish their accounts. This will be a significant drain to the money supply, which has been above the historical trend due to the COVID response. Lower money supply results in tighter financial conditions, which can put downwards pressure on equities and bonds.

Sentiment

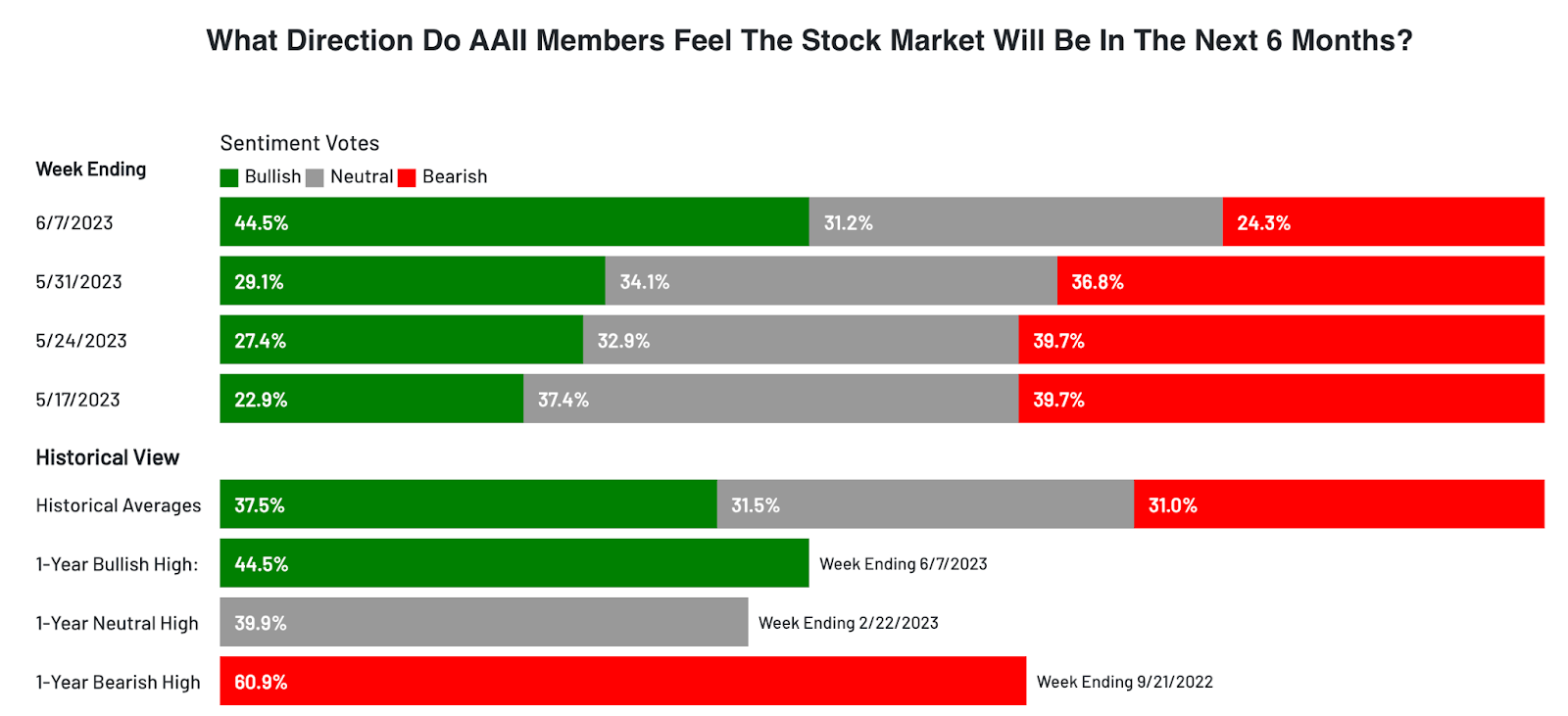

Sentiment seems to be turning for what some have called the most hated bull market. Bullish sentiment jumped to 44.5%, hitting a 52-week high.

https://www.aaii.com/sentimentsurvey

At the same time, volatility is at its lowest level since the start of the pandemic.

Are investors starting to get complacent, or is this the beginning of a new bull market?

Q1 2023 Earnings

Over the last two weeks, 4 portfolio companies reported earnings.

Zscaler (ZS)

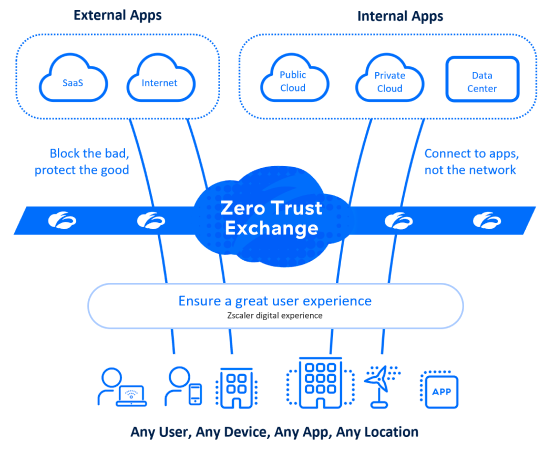

Founded in 2007 by Jay Chaudhry, Zscaler was built on the idea that the internet would become the new corporate network. An alternative to legacy VPNs and firewalls, Zscaler built a zero trust exchange that connects users, devices, and applications in a secure & controlled way.

Choudry and team were right on with their initial, visionary idea. With the emergence of the cloud and drive towards digitalization, nearly every company in the world is moving onto the internet. Zscaler provides a platform to enable them to do so securely and with flexibility. Users can access their systems from anywhere, enabling safe remote work & access. Zscaler’s solution is effectively acting as a middleman, checking all traffic and connections and only permitting access when authorized.

Jay Chaudhry, founder and CEO, owns 38.8% of the company today.

Zscaler is the clear leader in the space, serving over 40% of the Fortune 500. They have just over $1b in revenue and boast a $72+ billion serviceable market opportunity.

Customers love their solution. Zscaler boasts an NPS score greater than 70, compared to an industry average of 30.

The Zscaler team seems to be motivated and encouraged about their prospects.

Zscaler competes primarily against legacy, on-premise solutions. Contenders with next-generation solutions – including Cloudflare and Palo Alto Networks – have emerged in the wake of Zscaler’s success.

Diving into their financials:

Revenue growth is strong, coming in at 46% y/y for FY Q3. Zscaler has been able to maintain high rates of revenue growth for quite some time.

Guidance for Q4 shows some deceleration to 35% y/y growth. This is not unexpected given the macro environment and strong comparables. Zscaler’s growth has held up much better than other SaaS names, demonstrating Zscaler’s critical value proposition.

Gross margins are holding steady at 77%

EBITDA and FCF margins continue to demonstrate operating leverage, steadily climbing to 15% and 23% respectively

Cash conversion is very strong at ~107%, considering EBITDA of 76.7 million yielded FCF of 82.2 million

Balance sheet is strong, with the net cash position growing up to $753 million

Stock-based compensation (SBC) came in lower this quarter, apparent in both the GAAP expense line as well as a decrease in the share dilution. Dilution of 2.8% for 35%+ revenue growth and 23%+ in FCF margins seems reasonable.

Capital efficiency continues to improve alongside the margins. Note that total capital considers the impact of SBC. Free cash flow return on capital (FCF ROC) climbed to 18.6%, compared to 9.3% two years ago, showing the benefit of scale & negligible marginal costs software businesses are known for

Shares have been under pressure since the software peak in late 2021. The beginning of 2023 was no different, shares were down another 20% in the first 5 months of the year. In May, Zscaler had a press release pre-announcing their earnings. Their strong results served as a catalyst, and the price moved up from the low of $85 to over $150, gaining over 75%.

Trendlines are starting to turn. It seems plausible that the worst is behind. As support continues to build, shares seem to have plenty of room to run.

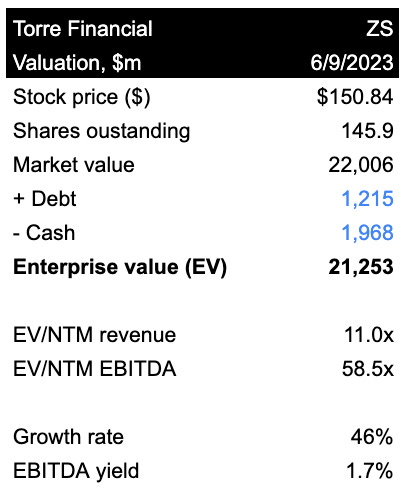

As for the valuation:

As a high-quality, high-growth technology company, Zscaler trades at a hefty premium. These high valuations are prime targets for volatility, as a lot of the value is expected to be realized in the future. The sentiment and overreaction can lead to volatile moves, such as the recent move from $85 to $150+.

Looking out 5 years across possible combinations of revenue growth and revenue multiples, Zscaler appears to be an appealing opportunity.

Considering 3% dilution each year, if the company is able to grow between 20-30% and fetch a reasonable multiple between 8-10x, annualized returns could yield between 8-23%. Note that this considers multiple compression, compared to the current multiple of 11x.

Closing thoughts

The market seems to be sending conflicting signals. Although there are plenty of concerns, the technical picture is poised for further upside. As the saying goes, markets tend to climb a wall of worry.

Long term investors with a business owner mentality focus on company fundamental performance and potential expected to help keep a level mindset.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.