Market & Earnings Review - March 18, 2023

Market commentary, portfolio company earnings results, and closer look into Crowdstrike (CRWD)

Market

The market has been trending lower since the beginning of February. The January low looks to be providing support, with the market bouncing off the $380 level. Notwithstanding, the market closed out the week just below the 200-day moving average.

There has been plenty of activity these last few weeks.

On March 7th, Jerome Powell addressed Congress and reinforced the need for more rate increases: "The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.”

Economic reports came in strong, particularly the jobs market. The March 10th report showed non-farm payroll significantly exceeding expectations, rising 311k vs 225k expected. The gains are concentrated in hourly earners, with strength in leisure, hospitality, manufacturing, and retail offsetting weakness in technology.

The February CPI report was released on March 13th. Results were inline with expectations, showing inflation of 6% year-over-, and +0.4% month-over-month.

While macroeconomic indicators show persistent strength, the significant pace of rate increases is starting to cause issues. There is a delay between the rate increases and the impact to the economy. It takes time for the changes to work themselves through the system. Cracks are not only starting to show, but also starting to spread.

In July 2022, a large crypto hedge fund, Three Arrows Capital, declared bankruptcy

In November 2022, a large crypto exchange, FTX, declared bankruptcy.

On March 8th, one of the main banks for the crypto industry, Silvergate Capital, declared bankruptcy.

On March 9th, the primary bank for startups and the technology industry, Silicon Valley Bank (SVB), announced the need for more capital and failed on March 10th after a run on the bank. SVB was a top 20 bank in the USA with over $200 billion of assets.

How did this happen?

Focusing on tech startups, SVB benefited from huge inflows the last few years from startup fundraising efforts. SVB invested those funds in long duration assets such as 10-year mortgage-backed securities and bonds. A notable error in risk management, SVB did not hedge the duration risk. As rates rose, those assets were worth less.

Startup fundraising slowed down, which meant fewer deposits for SVB.

Startups kept spending money, drawing down SVB’s deposit base.

In order to fund the withdrawals, SVB had to sell assets at a huge loss. SVB’s attempt to make up for the gap by raising new capital was quickly interpreted by the market as a significant liquidity issue. Concerned for their money, startups started moving their cash out. VC firms instructed their startups to move their cash. On Thursday alone, depositors tried to pull $42 billion. SVB was unable to fulfill all the withdrawals. Regulators took possession of the bank on Friday, March 10th. After operating for over 40 years, SVB was dismantled in 36 hours.

On March 12th, regulators also took over a New-York-based real-estate bank that had recently gotten into crypto, Signature Bank. Concerned about crypto exposure, real estate investors withdrew significant amounts to avoid any possibility of loss. Signature Bank had been in operation for over 24 years.

The Fed and FDIC partnered to backstop to depositors of SVB and Signature Bank. While equity and debt holders may get wiped out, all depositors will be made whole.

On March 14th, one of the biggest financial institutions in the world, Credit Suisse, disclosed “material weaknesses” with their reporting and hit by a bank run.

Rising rates have hammered the value of existing bonds that banks hold. Beyond concentrated bank runs, many banks are seeing customers move their deposits into higher-yielding alternatives such as money-market accounts, fueling the issues.

Given the current concerns, banks are likely to tighten their lending standards, resulting in tighter monetary conditions.

The Fed’s recent actions to backstop and support the financial system are effectively a form of quantitative easing, contradicting their push for higher rates.

The market was quick to realize the significance of the events since the unfolding of SVB.

Yields have come down dramatically.

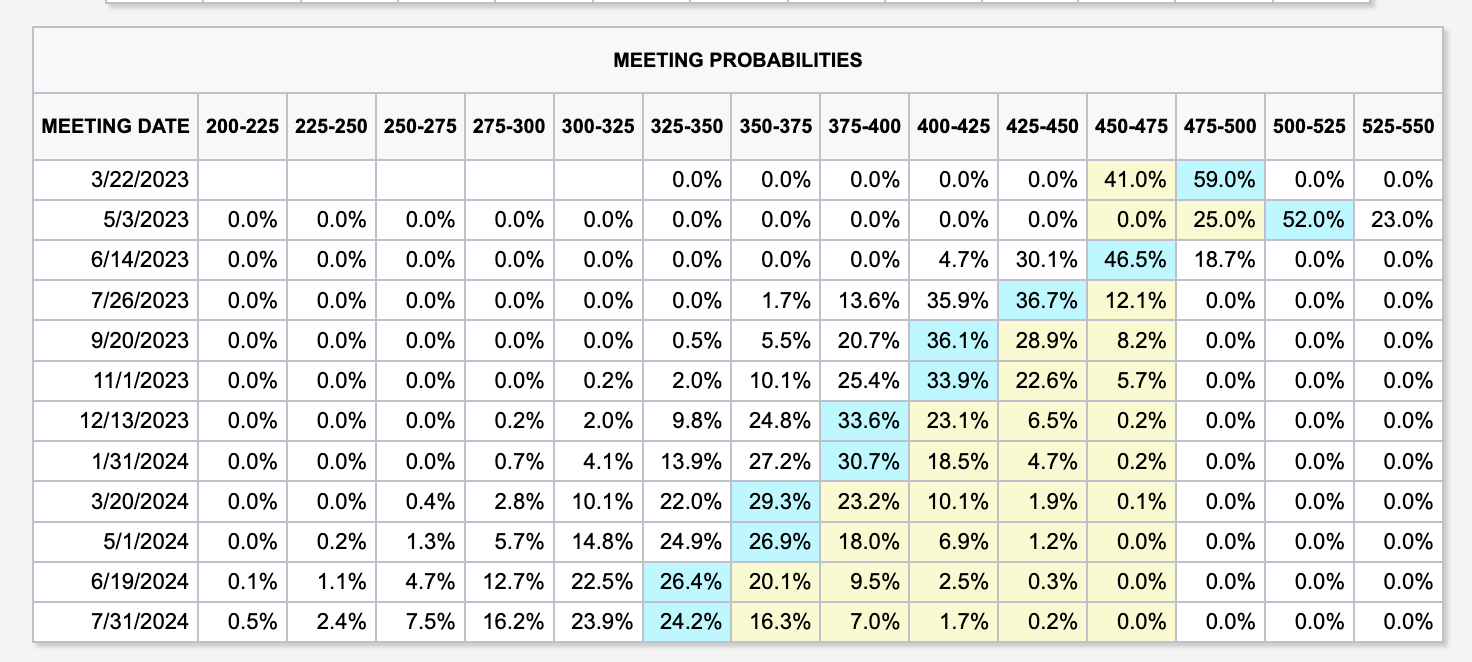

Relatedly, expectations of future rate increases have shifted.

One week ago, there was a 60% chance of a 25 bps increase and 40% chance of a 50 bps increase.

Today, there is a 60% chance of a 25 bps increase and 40% chance of no increase!

The market is currently expecting two 25 basis point hikes and cuts starting as soon as June.

Powell and the Fed are in a difficult spot choosing between financial stability and fighting inflation.

While the job market may be hot for now, commodities prices, a leading indicator of inflation, seem to be backing off.

Q4 2022 Earnings

Over the last two weeks, two portfolio companies reported earnings: Crowdstrike and Adobe.

Adobe surprised to the upside, demonstrating the resilience of their business model. Growth is expected to continue at a rate of nearly 10%. Adobe’s strong outlook, high margins (88% gross margins, almost 50% FCF margins) and valuation of 18x EV/EBITDA presents a compelling opportunity at 18x EV/EBITDA. The Figma acquisition is still under review, but expected to go through.

CrowdStrike (CRWD)

CrowdStrike is a cloud-native leader in the cybersecurity space.

Starting in endpoint security, CrowdStrike created their Falcon Platform as a way to build an intelligent threat graph. With visibility into signals across many customers, their platform is able to identify and block bad actors through pattern recognition via machine learning models.

This cloud-based solution quickly displaced traditional antivirus software, which relied on downloading databases of known attacks and could only prevent those enumerated attacks.

Today, their platform now offers over 20 modules covering endpoints, cloud systems, threat intelligence, identity, sec ops, observability, and more. The land-and-expand approach has been working for them, as 62% of their customers have over 5+ modules.

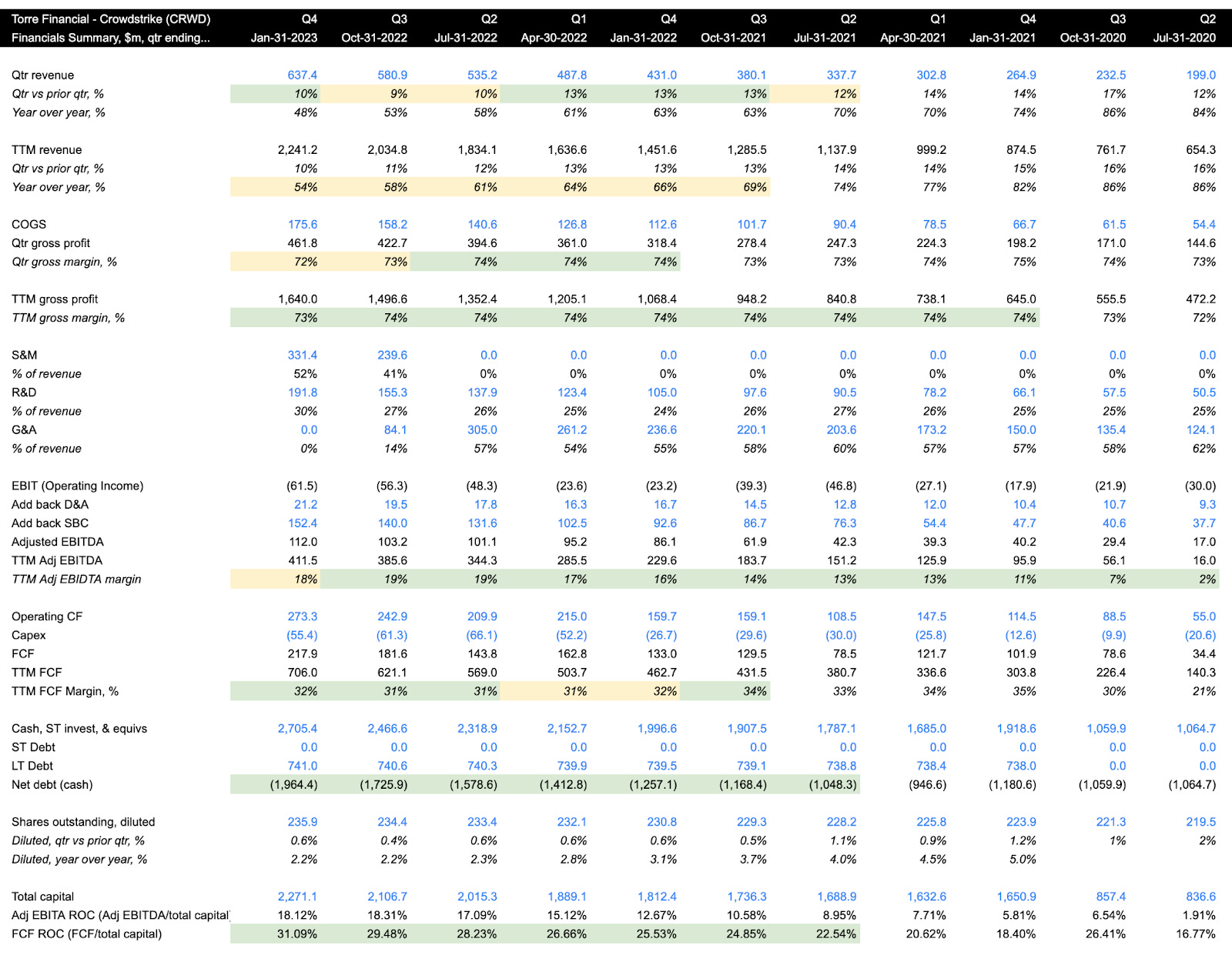

A summary of their financials:

Revenue accelerated q/q to 10%, a notable feat in the current environment

TTM revenue came in at 54% and has been declining since peaking in mid-2021

Gross margin is ticking down, now at 72%. This is important to keep an eye on. SentinelOne is an emerging competitor. They are much smaller, but have been offering a comparable solution at a competitive price point. It will be important for CRWD to demonstrate their competitive advantage.

EBITDA margins came in at 18%, seemingly peaking at 19%

Comparing EBITDA ($112m) to Operating Cash Flow ($273) reveals some of their pricing power. The difference between the two values is primarily due to working capital. CRWD is effective at bringing cash in the door, even before recognizing the revenue.

This helps yield strong FCF margins > 30%.

Cash in the bank has been increasing. Net cash has increased to nearly 2b from 1.2b a year prior.

Shares outstanding are growing, as they are using stock based compensation to attract and retain talent. The y/y rates have declined to 2.2%. Consider the tradeoff between the 50%+ growth and the 2% dilution.

In terms of efficiency, CRWD is generating FCF return on capital north of 30%. It has progressed nicely over time, and given the negligible marginal costs of selling software, this can continue to increase.

As for the outlook, the company is calling for

Revenue of $676.5m for Q1, an increase of 6% q/q

Revenue of nearly $3b for the full year, or growth of ~33% y/y

FCF margins of 30% for the year

Less than 2% dilution

Given the strong fundamentals and significant opportunity (CRWD’s market is expected to grow 13% per year!), the premium valuation shouldn’t come as a surprise.

Since peaking in late 2021 at nearly $300, shares have been on a downtrend. There have been a few attempts to break out to the upside, only to see a dip lower. Starting in 2023, the technical picture seems to be improving.

Closing

Crowdstrike and Adobe rounded out the final earnings results for this season. Both are fundamentally sound companies, albeit in different phases of maturity.

The Fed will be meeting on March 21-22. Stay tuned for the commentary. The market is expecting a 25 bps increase. While that may be well known and priced in, Powell’s commentary and tone will give some insight into what is to come.

--

Share

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.