Market & Earnings Review - May 13, 2023

Market commentary, portfolio company earnings results, and closer look into PayPal (PYPL)

Market

The S&P 500 has been steady over the last week. Holding above both the 200-day and 500-day moving averages, the sideways action can be considered bullish as the market builds support.

The market is up year-to-date. Returns across the board :

Nasdaq +21.9%

S&P 500 +7.4%

Dow Jones +0.5%

The divide amongst the indices is apparent when looking at each sector.

Communications (+24.8%), Technology (+21.6%), and Consumer Discretionary (+14.8%) are the top performers year-to-date by a wide margin.

Energy (-9.3%) and Financials (-6.3%) are rounding out the bottom.

Consumer Staples, Real estate, Materiales, Industrials, Utilities, and Healthcare – typically considered defensive sectors – are in the middle of the pack, with returns ranging between -2-4%.

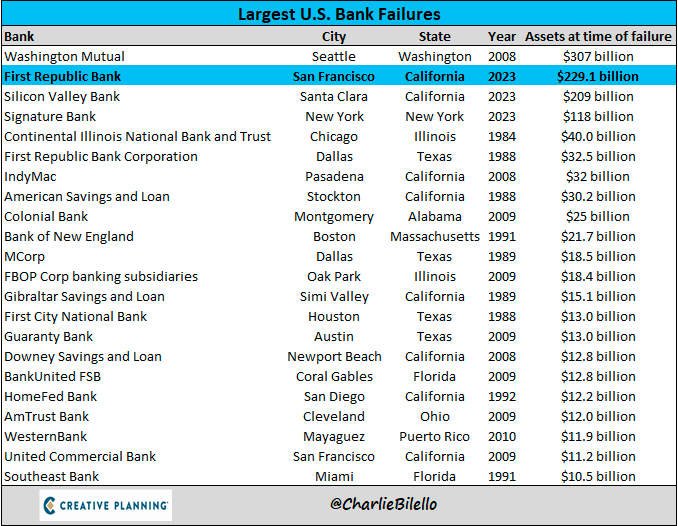

The Financial sector being down only 6.3% doesn’t do justice to the ongoing turmoil. Regional banks continue to be under pressure from a consumer confidence perspective. Following the failures of Silicon Valley Bank and Signature Bank, First Republic Bank was next. Even with a $30 billion injection from a collection of large banks, First Republic was unable to survive the more $100 billion in outflows faced in Q1.

First Republic was roughly 10% larger than Silicon Valley Bank and took its place as the second largest bank failure. JP Morgan acquired First Republic at a fire sale price.

Notwithstanding the banking turmoil, the Fed increased rates for the 10th time on May 3rd, taking the fed funds rate to a target range of 5-5.25%. The target rate is now above the PCE inflation rate, the Fed’s preferred inflation indicator. With a positive real rate, Powell finally seems ready to pause even after acknowledging the tight labor market.

CPI continues to decelerate, only up +4.9% year over year in April. Inflation is poised to continue its down trend as the trailing six-month annualized change is +3.3% and the trailing three-month annualized change is +3.2%.

Markets are expecting a pause for the Fed’s two summer meetings, with a possible rate cut as soon as September.

Q1 2023 Earnings

Earning season is well underway and the tone has been positive – much better than feared.

About 85% of the S&P 500 companies have reported their Q1 earnings, with 75% beating revenue estimates and about 79% beating earnings estimates. S&P 500 earnings are down about -2% in Q1 2023 vs the forecast of roughly -6% to -8%.

Over the last few weeks, 8 portfolio companies reported earnings.

PayPal (PYPL)

Established in 1998, PayPal has become a clear leader in digital payments & participating in the secular rise of e-commerce.

PayPal found early success in secure electronic payments, enabling payments via email addresses instead of via credit card numbers.

PayPal’s founders and early team include Peter Thiel, Max Levchin, Luke Nosek, Ken Howery, Yu Pan, Elon Musk, and many others. These entrepreneurs, known as the PayPal Mafia, have gone on to create or lead many other technology companies such as Tesla, LinkedIn, Yelp, YouTube, and many more.

Shortly after IPO’ing in 2002, PayPal was acquired by eBay. PayPal operated as a subsidiary of eBay for 12 years until 2014 when PayPal was spun out into its own separate publicly traded company.

PayPal’s ease-of-use and dominance in checkout has made it popular amongst consumers and enabled the build out of their two-sided network. As of May 2022, PayPal has nearly 400 million active customer accounts and 35 million merchant accounts.

Merchant adoption of PayPal, which is very sticky and difficult to remove, is significantly ahead of competitors and growing at the fastest rate.

Merchants add PayPal to their checkout because it increases conversion through not only ease-of-use, but also approving more transactions that otherwise would be declined, particularly international or other complicated transactions.

While PayPal has expanded to many different offerings including merchant services and credit/lending, the majority of their revenue comes from transactions. For 2021:

Transactions revenue was 23.4 billion (92% of total)

Other revenue was 2.0 billion (8% of total)

About ⅔ of their transaction volume is USA-based and ⅓ international. Cross-border transactions represent roughly 12% of the total payment volume.

PayPal has grown impressively over time.

PayPal has built up strong partnerships over time including with Amazon (ex. checkout with Venmo), Microsoft (ex. powering payments within Teams), Apple (ex. offering Apple Pay as a checkout option & integration PayPal into Apple’s Wallet), Starbucks, McDonald’s, and many more. PayPal also has strong beachhead customers showcasing some of their strengths, such as Uber and Airbnb for multi-party transactions via PayPal’s Hyperwallet.

On the consumer side, PayPal has been innovating with improvements such as passwordless login, a native sdk for a better mobile checkout experience, and financial products to bring consumers in. PayPal’s cashback credit card offers 2% on all purchases and 3% on PayPal purchases. PayPal’s high-yield savings account offers 4.15% APR.

Recently, however, there have been a few areas causing investor concern.

Dan Schulman, CEO of PayPal since 2015, is stepping down this year.

During the post-COVID boom, PayPal got carried away announcing bold, yet unlikely targets, such as trying to reach 700 million active accounts. They tried acquiring Pinterest. This got corrected quickly.

The company decided to focus on its core offerings and engaged users. Transactions per active account have been increasing. Q1 2023 was the first time active user accounts decreased q/q.

Competition has been heating up on both the merchant (Stripe, Adyen) and consumer side (Cash app, Apple Pay, Google Pay, etc). In response, PayPal has been focusing more and more on their unbranded checkout solution known as Braintree. Adapting to the environment, PayPal Complete Payments aims to expand their checkout presence from only consumer PayPal transactions to process all of the merchant’s transactions. By processing all of a merchant’s transactions, PayPal can help streamline their back office operations. While positive, this shift towards more unbranded processes can pressure the company’s margin profile.

A summary of their latest financials:

Q1 revenue growth of 9% is showing acceleration from prior quarter – a positive signal given the lapping of the COVID bump

Gross margins of 40%-42% are significantly lower than the 48-49% range from a few years ago. Gross margin compression typically signals higher competition/weakening pricing power. In PayPal’s case, the increased focus on unbranded processing is likely playing a part here. That being said, it is hard to disentangle the signals.

Operating costs, particularly SG&A, are coming down. SG&A is down to 13% of revenue from 18-19% of revenue a few years ago. R&D also has also seen some discipline, down to 10% vs 11-12% prior.

Adjusted EBITDA margins of 23% are healthy, but similarly show the same pressure on gross margins, coming down from 26-28% over the last few years

Cash conversion (calculated as EBITDA/FCF) is holding strong near 80%, a positive signal on the pricing power piece. Still down from 85-87% prior.

FCF margins are down to 18%, from 20-23% a few years ago.

As for the balance sheet, PayPal has a negligible amount of net debt.

Shares outstanding are decreasing at an accelerating rate. Shares outstanding are down 3.4% from the year prior. Looking at the trend, that may be 3.5%+ in the coming quarters.

Efficiency metrics – EBITDA return on capital and FCF return on capital – are mostly holding steady at 21% and 17% respectively. This is consistent with the earlier years, demonstrating a good balance between new lower-margin-higher-volume offerings, cost discipline, and share buybacks. These are arguably the most important metrics as they bring everything else together, so it is positive they have been maintained and are not deteriorating.

PayPal shares have been on quite the rollercoaster. After peaking above $300 in the summer of 2021, they have come down to low $60s. Over the last 5 years, PYPL has returned -22% vs a 51% return for the S&P 500.

As for the valuation:

At current prices, PayPal shares are not very demanding: FCF yield of 7.4% with revenue growth of 8-9%, and likely faster earnings and cash flow growth due to internal optimizations.

Exploring possibilities across an array of EBITDA growth and future EBITDA multiples, today’s price seems to offer attractive annualized returns ranging from 8% to 25% when considering most likely outcomes.

For another perspective, PayPal’s Fast Graph shows $96 is possible in a few years at a multiple significantly below historical measures – for annualized returns of 18%+.

Closing

There are plenty of puts and takes in the market. Q1 earnings have been surprisingly positive, catching many off guard. Inflation is coming down. The rate hike cycle is clearly closer to the end. These signals have provided some cautious optimism to the markets.

At the same time, the banking turmoil seems to be ongoing. Commercial real estate is beginning to show some cracks. There are lingering concerns about the impending recession and whether a hard landing can be avoided.

All that said, the market always offers opportunities. While some companies are looking expensive due to the optimism (i.e. Microsoft), others like PayPal are facing gloom and depressed sentiment. As long as PayPal can persevere, it may prove to have been attractively priced.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.