Market & Earnings Review - May 27, 2023

Market commentary, portfolio company earnings results, and closer look into Workday (WDAY)

Market

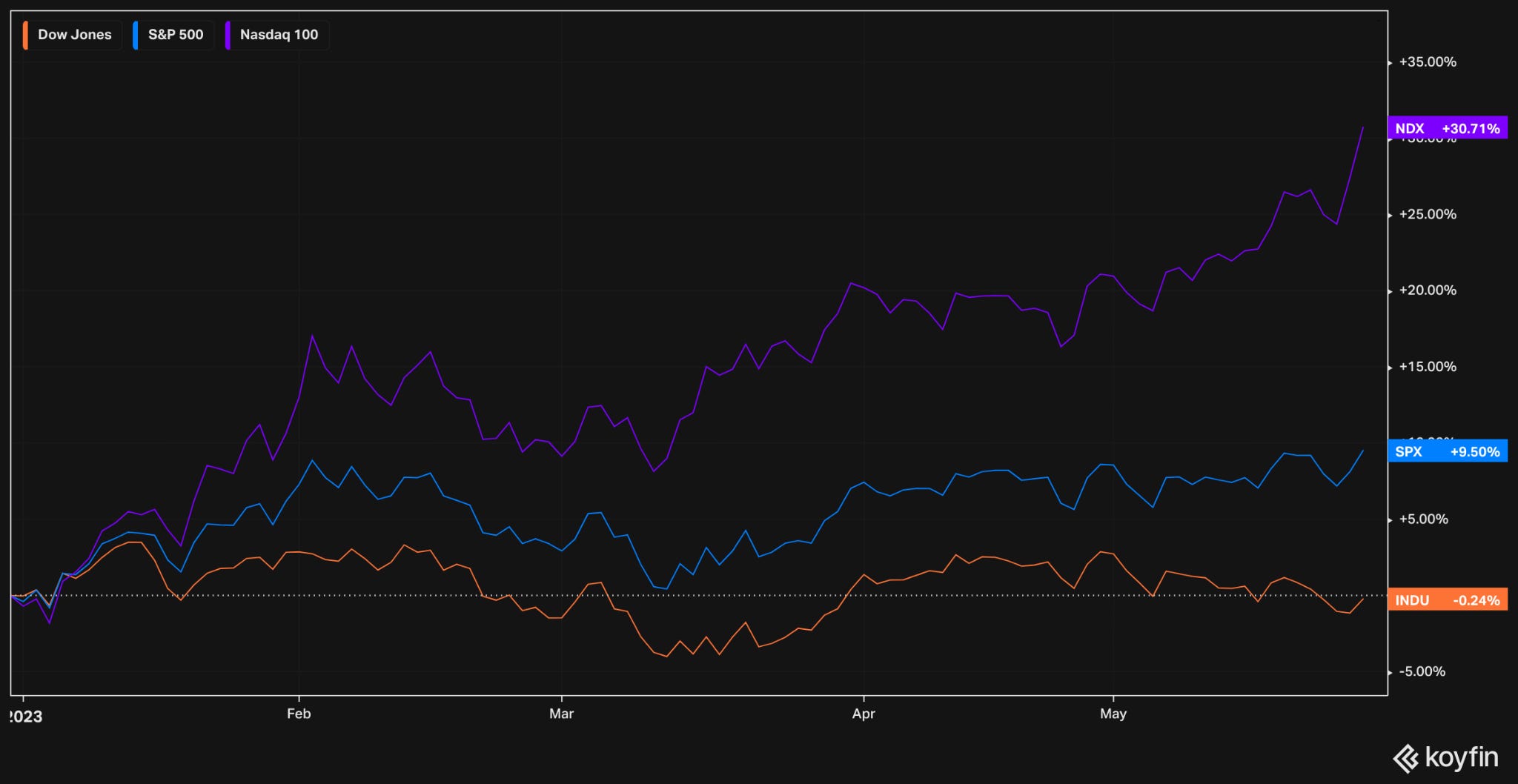

After trading sideways for a few weeks, the S&P 500 appears to be staging a breakout to the upside. The index continues to build support and the technical picture continues to strengthen as prices hold steadily above recent moving averages. The 420 level recently marked firm resistance – it will be critical to see how it plays out on this current move up. The S&P is up 9.5% YTD.

2023 is turning out to be quite the opposite of 2022. The Nasdaq is up nearly 31% for the year, leading the S&P 500 and Dow Jones by a wide margin.

Looking deeper, the underlying trends have clearly reversed.

The top areas of the market in 2022 – energy & value – are significantly underperforming in 2023.

The worst performers in 2022 – technology & growth – are the top performers in 2023.

What is driving markets in 2023? In short: rates, money supply, earnings, and AI.

Interest rates act as gravity on equities. Lower inflation (4.9% YoY) and expectations of steeper deceleration have helped pave the way for a pause in rate hikes. The Fed is expected to hold, and possibly cut, rates for the remainder of the year.

Money supply is another important aspect. “M2 is the U.S. Federal Reserve's estimate of the total money supply including all of the cash people have on hand plus all of the money deposited in checking accounts, savings accounts, and other short-term saving vehicles such as certificates of deposit (CDs).”, per Investopedia.

Since COVID, M2 money supply has trended significantly higher compared to prior years. There is still a lot more money out there than there was pre-COVID. Ample money supply will naturally result in higher asset prices.

Earnings have also been strong, coming in better than expected for Q1. With 93% of companies having reported, S&P 500 earnings are up 8% year-over-year, significantly better than expected. Additionally, profit margins have expanded to 11.8%, the highest since Q1 2022. Margin expansion is likely driven in part to the major cost cutting initiatives.

And finally, artificial intelligence, or AI.

Chat GPT unleashed AI to consumers, propelling a significant push to advance AI across nearly every conceivable use case. An increasing number of companies are pushing AI in their narrative.

The investing frenzy around artificial intelligence has been so strong that without it, US stocks would be down for the year, according to Societe Generale. S&P 500 is estimated to be -2% YTD if AI stocks are excluded.

Performance this year has been led by a select group of companies, mainly big tech.

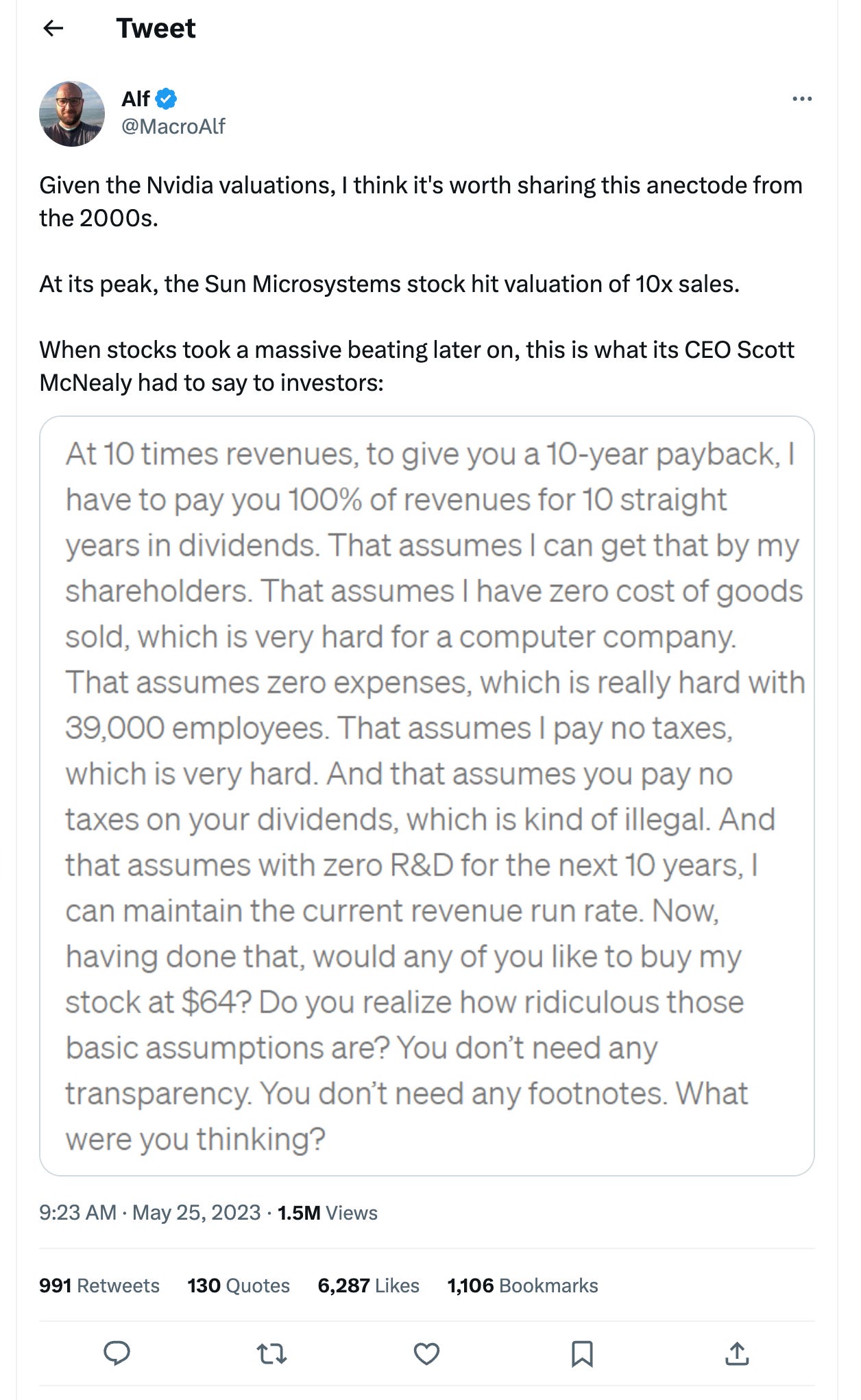

On timing the market, valuations, & NVDA

Timing the market is tough.

Cathie Wood, CEO of Ark Invest, invests in innovative, high growth companies. Their flagship fund closed out a position in NVDA in early January, only to see it skyrocket shortly after.

Shares of NVDA have nearly tripled since.

NVDA seemed expensive back in January, trading at roughly 15x sales.

The following tweet captures the sentiment rather well:

From that logic, Cathie’s decision to exit seems reasonable.

The multiple, however, continued to climb, up to nearly 30x in mid-May!

Given the divergence in the last-twelve-month and next-twelve-month multiples, it is clear that something happened at the end of May. The guidance Nvidia provided in their most recent earnings report made a big splash.

Nvidia called for Q2 revenue of $11B while analysts were expecting $7.18B. The provided guidance represents 53% growth q/q, and 64% growth y/y. What seemed prohibitively expensive all of a sudden seemed a bit less so. From an already extreme price point, shares jumped as high as 30% adding up to $200 billion to its market capitalization.

Valuation multiples are based on the known or expected data. Nvidia surprised everyone with their guidance. Fundamental shifts support a change in valuation. Markets are quick to price in any change.

Nvidia has made a strong case to back up the AI hype so far. They still have to deliver, and then maintain their growth. The market certainly has high expectations.

Is the current valuation fully supported? If they continue to surprise to the upside as they did in the last quarter, it very well might! From my perspective, however, it is still too pricey. There’s too much future growth baked into today’s price. It will be very difficult to maintain the high growth rates that come with the lofty expectations.

Q1 2023 Earnings

Over the last two weeks, 3 portfolio companies reported earnings.

Workday (WDAY)

David Duffield, founder and former CEO of PeopleSoft, and Aneel Bhusri, former chief strategist at PeopleSoft, founded Workday in 2005. Aneel continues to lead the company today, now as Co-CEO alongside Carl Eschenbach.

Workday has become a significant player in the enterprise stack, offering critical solutions to manage people & money. Workday started with Human Capital Management solutions, covering areas such as HR, talent, and payroll. They then expanded into offering Financial services including accounting, planning, spend management, and more. They have a vast amount of data and are very active with machine learning and artificial intelligence models to bolster their offerings.

Their offerings have resonated with the market. Workday serves over 10,000 global customers, including 50%+ of the Fortune 500.

Their growth has been steady and consistent as they continue to expand the breadth and depth of their offerings.

Diving into their financials:

Year–over-year revenue growth has historically wavered between 15-20% q/q. Recently, it has been trending down towards 15% from the peak of 22%. Given the macroeconomic environment, this is not necessarily unexpected. It will be important to look for growth to stabilize, potentially marking an inflection point.

Gross profit margin increased to 75%, the highest in the last few years. Very positive as it demonstrates pricing power.

Costs don’t seem to be under the same level of scrutiny as in other companies. SG&A and R&D costs have increased alongside revenue.

Over the last few years, FCF jumped and is now reverting back to the norm in the 18-20% range. It should hold in that range.

Cash continues to build up. Workday boasts net cash of $3b, up from $0.6b just a few years ago.

Dilution primarily due to stock based compensation is somewhat high. It peaked at an annual rate of 5% in 2021. It has come down to under 3% recently. For 15-20% growth, dilution of 3% seems to be quite expensive. For an alternative data point, consider CRWD – dilution is under 3% for nearly 50% growth.

Efficiency from a cash flow perspective seems inline. 18-25% returns on capital are more than healthy.

Workday shares peaked in late 2021, alongside the rest of tech. After free falling in 2022, the share price seems to have found its footing. Trends are positive: price is holding above moving averages while locking in higher lows & higher highs. The price gapped up over 10% after the Q2 earnings release.

As for the valuation:

Workday shares are not necessarily cheap. That being said, given their competitive advantage – being deeply embedded with larger enterprises, leading to very high switching costs – does seem quite durable. They are likely to maintain their positioning and growth for many years to come.

Considering the current trajectory of 15% EBITDA growth and 3% dilution, the following chart shows a range of future possibilities.

I highlighted the most plausible range of outcomes from my perspective. Assuming some multiple compression (from 35x today down to 20-30x in 5 years) and steady growth, shares at today’s price could return between 2-15% per year.

For another perspective, Fast Graph shows $300 is possible by January 2026, implying a roughly 13% annualized return.

Closing thoughts

Timing the market is hard (impossible?) to do consistently. Zooming out to the last few years, the whole market, and clearly the underlying industries, have been on a roller coaster.

Although it was difficult to hold on throughout 2022, it is rewarding to see things bounce back in 2023. At the same time it is important to keep a cautious eye and keep risk management top of mind. While the exuberance can continue for a while, reversions tend to occur very quickly.

As for Workday, although shares are not screaming cheap, I find it to be a solid company with great economics & sticky offerings. The outlook is positive and full of opportunities. People and money are arguably an enterprise’s most critical assets. I continue to hold our position.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.