Market, Earnings, and ABT - November 25, 2023

Market commentary, portfolio company earnings results, and a deeper look into Abbott Laboratories (ABT)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

Happy Thanksgiving! There’s a lot to be grateful, including the stock market. The S&P 500 is up about 9% in November alone. The market has been up 16 of the last 19 trading days.

Over the last two weeks, the S&P 500 broke through resistance at the 50-day moving average and jumped higher. The market has now surpassed the two prior local peaks of 438 and 453, and seems poised to challenge this year’s high of 459.

Year-to-date performance across indices:

Nasdaq +46%

S&P 500 +19%

Dow Jones +7%

Two important themes driving the market higher include 1) the end of rate hikes and 2) AI.

The latest CPI report came in better than expected at 3.2% vs. consensus of 3.3%. This is the lowest reading since September 2021 and gives further evidence of inflation being tamed.

Truflation, a more realtime index, shows inflation at 2.85%.

Jerome Powell has yet to claim mission accomplished, stating “we are not confident” the benchmark rate is high enough to drive inflation down to 2%. He is keeping the option open for further hikes.

The market, however, is expecting no more rate hikes. In fact, cuts are expected in the first half of next year.

On the AI side, signals continue pointing to a massive, new market opportunity.

Nvidia reported earnings on November 21, 2023. Revenue of $18.12 billion was up 205% year-over-year, and beat expectations by $2 billion, or 12.5%. Guidance of $20 billion for Q4 calls for continued growth, and similarly exceeds the consensus estimate of $17.8 billion.

The AI opportunity is becoming increasingly clear as it translates into sales.

Nvidia primarily sells hardware – the chips on which AI applications run. This is step 1 in building out the ecosystem. As these chips are deployed and more capacity becomes available, the software AI ecosystem will explode.

Microsoft has similarly shown strong results, as they continue to infuse AI into all of their products. Github is a developer platform owned by Microsoft and its AI offering, Github Copilot, already exceeded over $100 million in ARR in October. In September, Microsoft launched a similar AI solution, Microsoft Copilot, for its enterprise business suite. Microsoft also owns 49% of OpenAI, the parent company behind ChatGPT, after having invested over $10 billion.

Relatedly, OpenAI made headlines recently as a board coup looked to shake things up at the $80+ billion startup. In short:

On Friday, November 17th, the board fired CEO Sam Altman on claims he was not being transparent in his communication.

Over the weekend Sam tried to negotiate his way back to the company, to seemingly no avail. Part of his ask was significant changes to the board.

Sam publicly announced he was joining Microsoft to head up AI efforts.

The majority of the OpenAI team mentioned they would quit if Sam Altman left.

Satya Natella of Microsoft offered to hire anyone from OpenAI. So did Salesforces’ Marc Benioff.

A few days later, OpenAI said Sam Altman will return as CEO and announced the formation of a new board.

For full coverage see WSJ’s Behind the Scenes of Sam Altman’s Showdown at OpenAI and OpenAI Says Sam Altman to Return as CEO.

Financial performance is validating the AI saga. It is real and worth pursuing.

The leaders, including OpenAI, Microsoft, Nvidia, Google, Meta, and Amazon, are well positioned to take advantage of this new secular growth opportunity.

Earnings

No portfolio company reported earnings over the last two weeks.

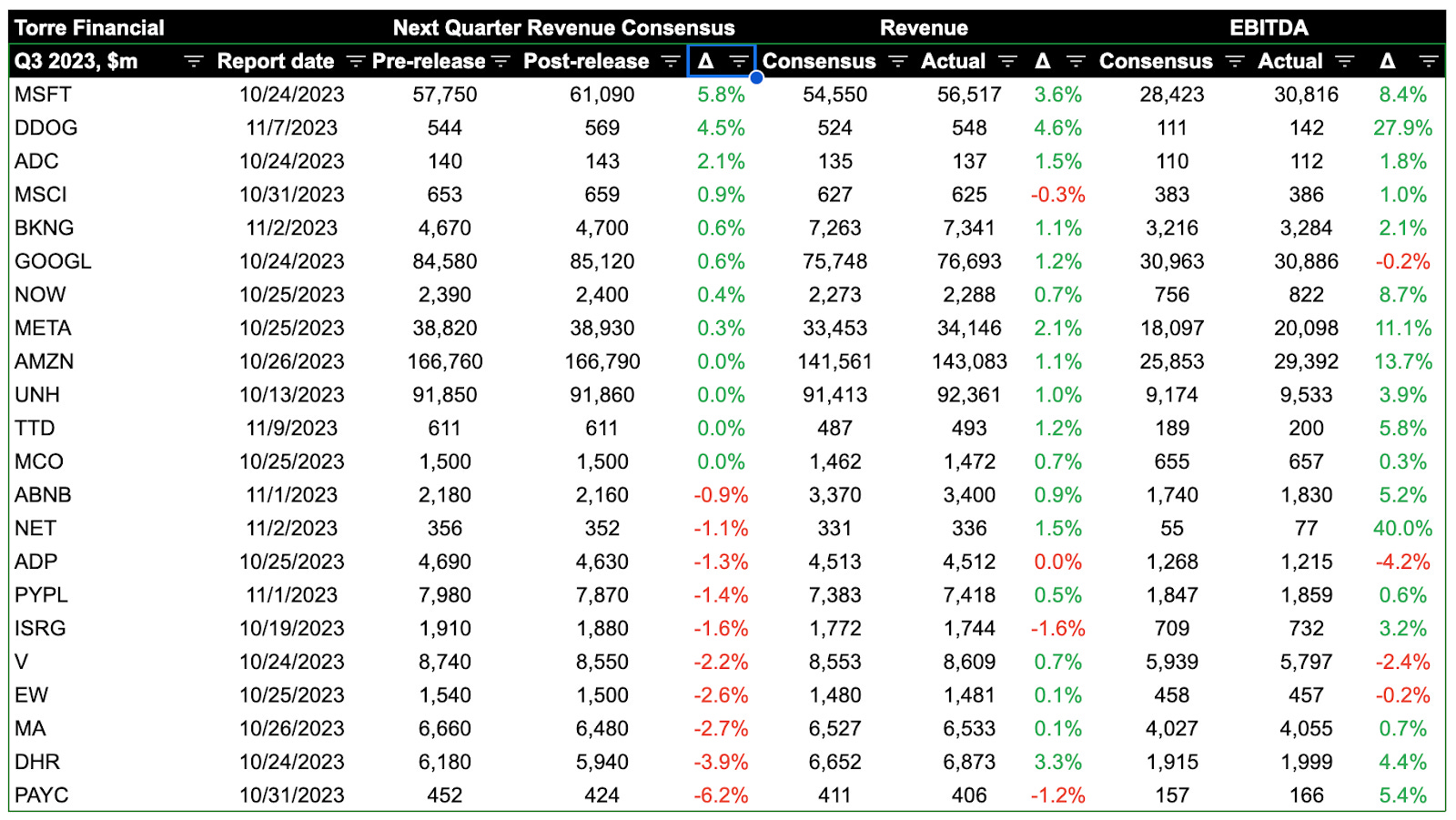

The following table summarizes Q3 earnings to date, sorted by the change in next quarter’s revenue expectations. Given the market’s forward looking nature, looking ahead gives the most insight of what is to come.

Microsoft, Datadog, and Agree Realty came in at the top with the largest increase against expectations. These three companies also beat current quarter revenue and EBITDA expectations healthily.

Paycom, Danaher, and Mastercard round out the bottom. Their current quarter results were generally strong. Paycom mentioned their new offerings are cannibalizing their current offerings – their new products are so good, that their customers have fewer errors and require fewer corrections which results in fewer fees. Danaher continues to search for the bottom in biotech processing spend. Primary factors include the high cost of capital, working through supply chain issues, the bottleneck in drug approvals, and slowdown in China. Biotech processing is a promising field, and Danaher is a top tier team. As this temporary slowdown turns around, Danaher is well positioned to capture the market and benefit from continued growth.

Abbott Laboratories (ABT)

“At Abbott we’re dedicated to helping people live more fully, in everything we do. We’re creating the future of healthcare through life-changing technologies and products that make you healthier and stronger, quickly identify when you have a medical need, and treat conditions to help you get back to doing what you love.”

Abbott is over 130 years old, having been incorporated in 1900.

Abbott is a healthcare conglomerate, covering a wide range of solutions.

The business is divided into four segments:

Diagnostic Products (38%) – Systems and tests sold to hospitals, laboratories, physicians, etc; these solutions to screen for cancer, cardiac issues, metabolic problems, drug abuse, alcohol usage, thyroid, fertility, neurologic issues, infectious disease, COVID, malaria, and many more

Medical Devices (34%) – Primarily focused on cardiovascular, diabetes, neuromodulation; Solutions include rhythm management, heart monitoring, vascular and structural heart (similar to Edwards Lifesciences)

Nutritional Products (17%) – Well known products including Similac, Ensure, Pediasure, Pedialyte, Zone Perfect, amongst others

Established Pharmaceutical Products (11%) – Essentially branded generics

Abbott focuses on attaining the top solution for the given market. They have many well-known brands, and many of their products are #1 in their use case.

Abbott has paid dividends for nearly 100 consecutive years. This year marked the 51st consecutive year of dividend growth.

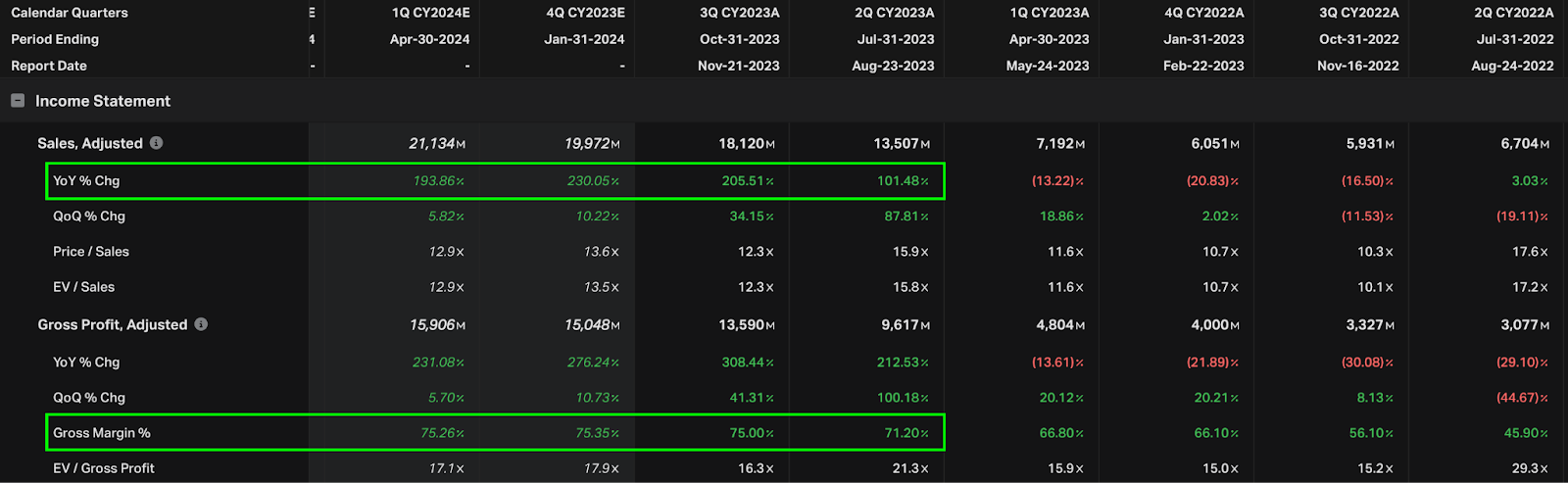

The COVID pandemic boosted Abbott’s diagnostic business – BinaxNOW was one of the most popular at-home COVID testing kits. Sales reached a peak of $43.6 billion in 2022.

Today, sales are nearly 10% to $40 billion. Overall growth is slightly muted, primarily due to difficult comps as the COVID testing boom fades and normalizes.

Growth rates, excluding COVID testing sales:

Medical devices growing at +14.7%

Diagnostics growing at +10.1%

Established pharmaceuticals growing at +11.1%

Nutrition growing at +18.1%

Notwithstanding the declining headline number, the underlying business is in great shape. These underlying numbers show the company’s durable growth. The bump from COVID testing was an anomaly, a change in behavior throughout a fixed period of time. Once the COVID bump headwinds pass completely, Abbott’s growth profile will return to normal.

Because of this dynamic, Abbott shares were available at a very reasonable price this year. This is a very high quality company that normally trades at a premium.

Diving into the financials:

Revenue is down 11% y/y, yet growth rates are improving. The last two quarters have shown gains q/q, indicating a possible inflection point. Although two data points is better than one, it is still early – a third showing acceleration would solidify the inflection.

Gross profit of 55% is lower than the historical norm of 58-59%.

EBITDA margins of 31% are higher than the historical norm, likely due to a push towards efficiency. Pre-covid the company had margins between 20-25%.

The gap between EBITDA and Operating Cash Flow is quite significant, implying that the company requires quite a bit of cash as working capital.

FCF margins of 11% have been trending downwards. We’d like to see this stabilize and turn upwards.

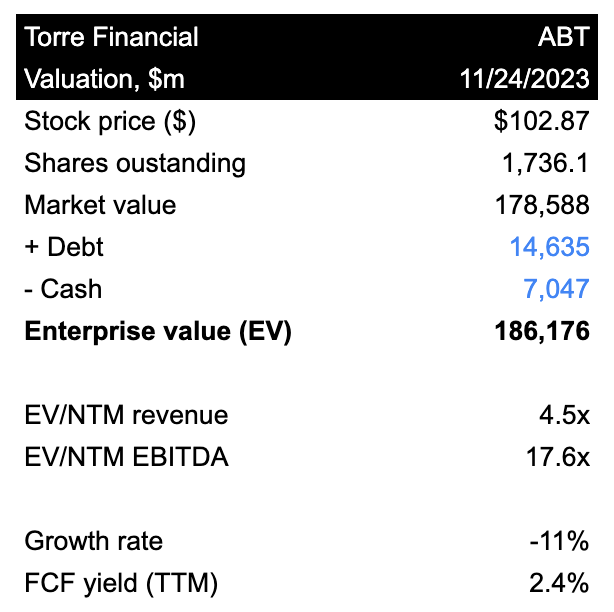

The balance sheet is healthy with $7 billion of cash and $15 billion of debt. The debt is easily serviceable with their $12.5 billion in EBITDA and ~$5 billion in FCF.

Shares outstanding have been trending steadily downwards as the company buys back shares.

Efficiency metrics, similarly to margins, have been trending lower.

Although the financial profile isn’t perfect, Abbott has lived the test of time and has a seasoned team with a proven track record. The business has been well-managed, consistently exceeding expectations. This interim rough patch has given investors the opportunity to get in at an attractive valuation.

The shares have been on the COVID rollercoaster the last 3 years. The shares climbed relentlessly up to $140 in December 2021. Shares started to come under pressure as testing and other COVD concerns started to ease up. Rates also started to rise. Local troughs in October 2022 and March 2023 rounded out at $94-96. The most recent bottom in October 2023 hit $89. We started building our position aggressively at $91-$92. Shares have since climbed out and currently trade nearly 15% higher.

As for the valuation:

Being a mature business, earnings and FCF are the better indicators. The valuation looks reasonable at 17.6x EV/NTM EBITDA. The TTM FCF yield of 2.4% seems a bit pricey. Considering next year’s estimate, however, the blended FCF yield jumps up to 3.5%.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share reduction of 1%.

The current price appears to offer annualized returns between 6-12%.

For a different perspective, Fastgraphs shows similar potential of price appreciation. If shares were to trade at their normal P/E multiple by December 2025, the shares would yield an annual rate of return of 8%.

Closing thoughts

Market sentiment has changed rapidly. After sulking for months, the stock market got a renewed jolt of energy. It is always more pleasant to see the market go up than down!

We’ve continued with our plan to build out a more resilient equity portfolio. Part of that plan has been to build out further diversification into healthcare.

Healthcare is one of the few sectors that beats the broader market over time.

Healthcare broadly has been under pressure this year. Today, there are more and more signs of healthcare being at a point of inflection.

It has been an opportune time to build long-term positions in high quality companies. Throughout the year we’ve built positions in Danaher, Edwards Lifesciences, and Abbott.

The competitive advantages in healthcare are clear – high barriers to entry, regulation, high risk to new entrants, etc.

Companies able to establish themselves are able to benefit from durable, stable growth. Healthcare markets are typically resilient to economic downturns, as people will always prioritize their health.

Regarding efficiencies and return on capital, we’ve focused on the best performers in the industry.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.