Market, Earnings, and ADC - October 14, 2023

Market, Earnings, and ADC - October 14, 2023

Market commentary, portfolio company earnings results, and a look into Agree Realty (ADC)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

Since peaking in late July, the market has sold off and formed a series of lower lows.

Lower lows show a deteriorating technical picture, as buyers are unable to form a stable base.

Notwithstanding, the market bounced firmly off of the 200-day simple-moving average and is now sitting at 431. We’ve been tracking this level for a few months as it provided support in late June and in mid-August. If the market is able to turn this level into support, it may provide a solid base and help the market keep climbing.

Year-to-date performance across indices:

Nasdaq +37.1%

S&P 500 +12.7%

Dow Jones +1.6%

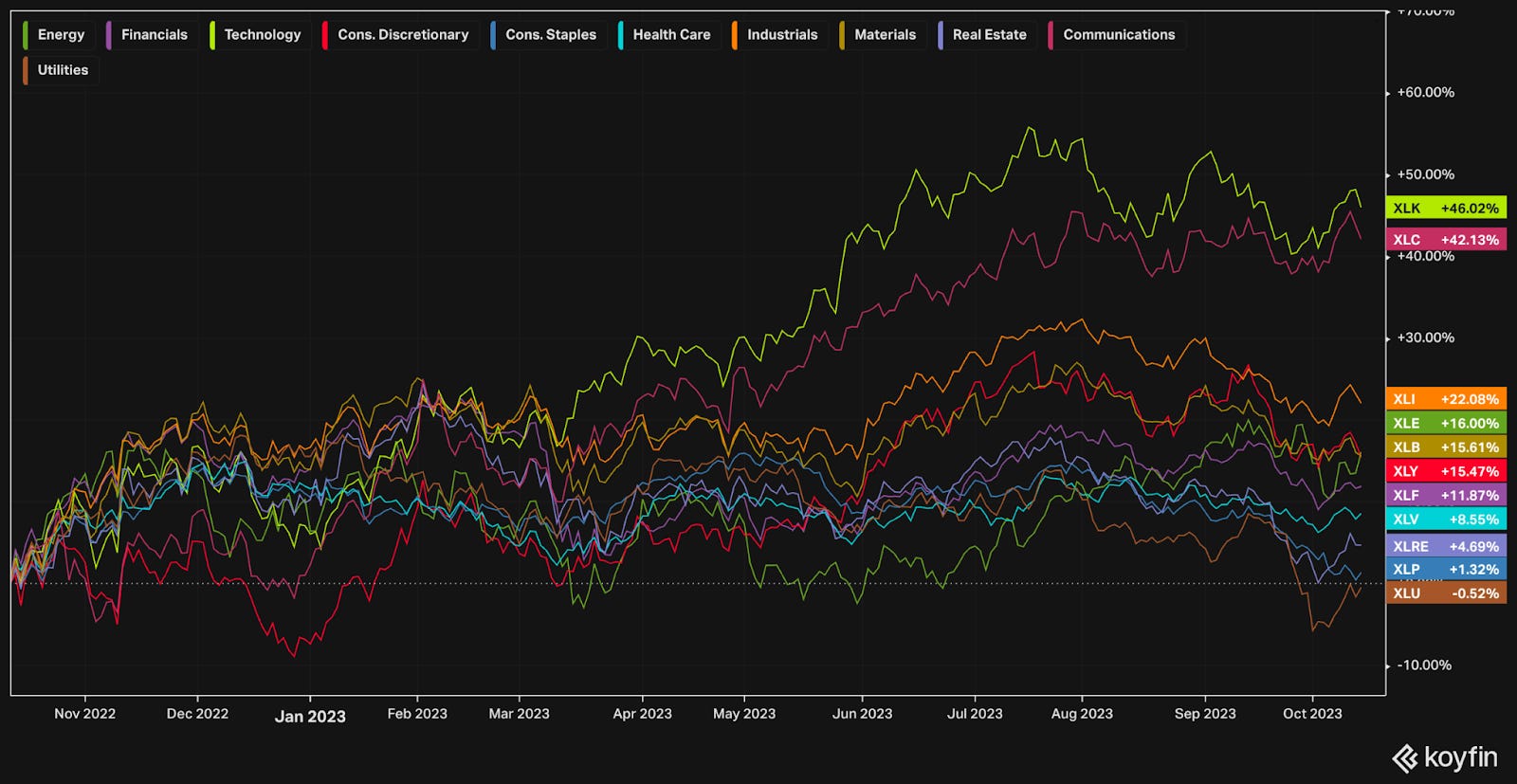

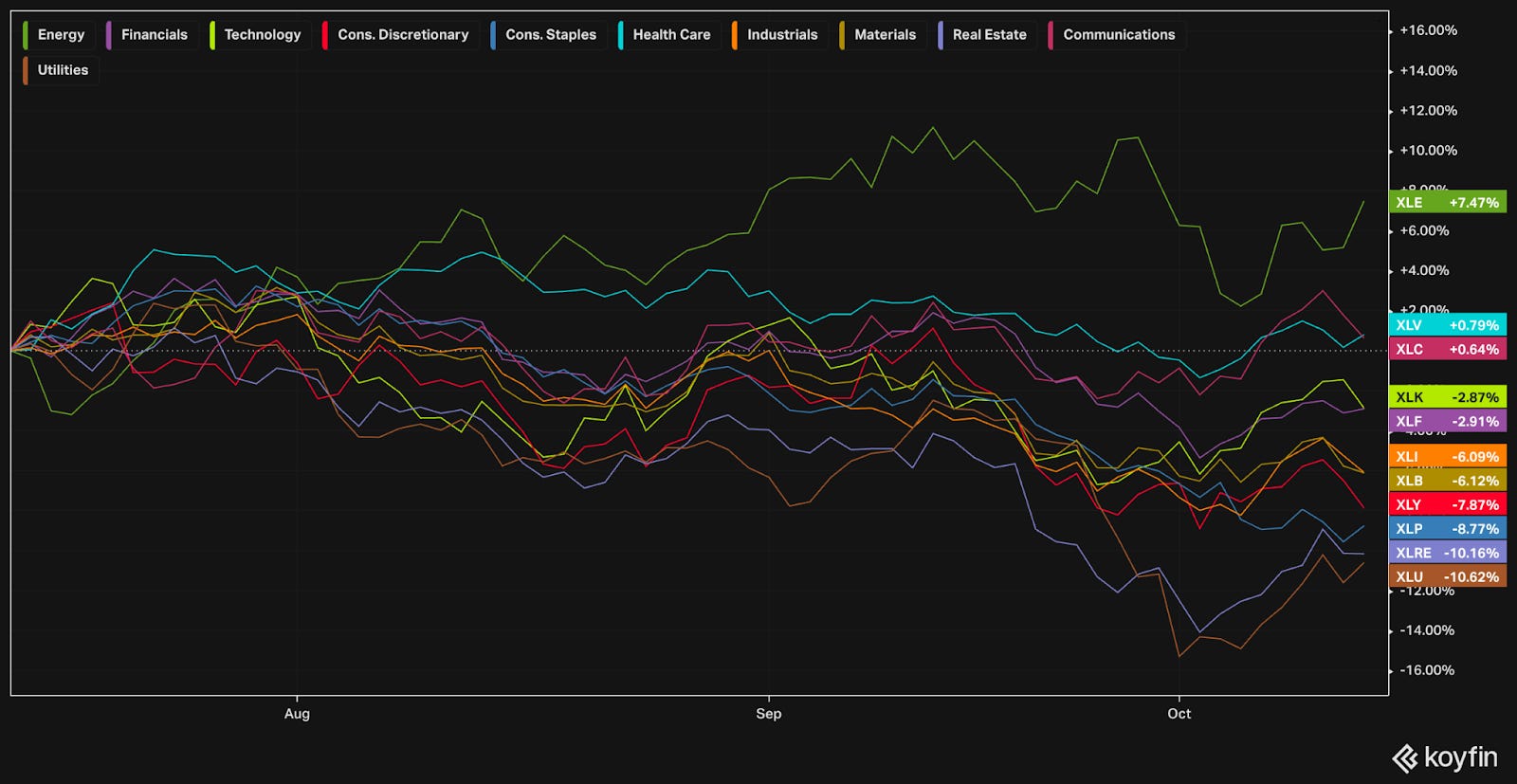

Looking at performance across sectors can give insight into the undercurrents.

Over 1 year (1Y)

Year-to-date (YTD)

Over 3 months (3M)

Over 1 month (1M)

Takeaways:

Technology and Communication have held up well across all timeframes

Consumer Staples, Utilities, and Real Estate have been laggards across all timeframes

Industrials, Materials, and Financials have been steadily in the middle of the pack

Healthcare was lagging, but seems to be showing relative strength in the more recent timeframes – it could be worthwhile to dive in and explore opportunities.

Consumer Discretionary was leading, but seems to be showing relative weakness in the more recent timeframes – it could be worthwhile to consider lowering exposure.

Momentum is a powerful force in markets. Understanding sector rotation can help investors position themselves accordingly.

Typically when yields rise, equities fall. During the first half of the year, however, yields and the market were moving upwards in tandem.

As of mid-August, this relationship reverted and equities have been moving inversely to yields.

With yields being such a powerful force, it can be helpful to understand how they move.

Short-term yields (1y, 2y, 5y) are driven primarily by the Fed Funds rate. Long-term yields (10y, 20y, 30y) are primarily driven by supply and demand, i.e. investors. The Fed tries to influence long term rates, for example by stating they will keep rates “higher for longer.” Note that the Fed can also purchase or sell bonds as necessary.

The yield curve inverted in mid-2022 and has remained inverted. A yield curve is said to be inverted when shorter duration bonds have higher yields than long duration bonds.

As the Fed started hiking rates, the short end of the yield curve moved up quickly. Investors believed that the hikes could be short-lived, perhaps resulting in a recession and forcing the Fed to cut rates quickly.

More recently, the long end of the yield curve started moving up. Investors started believing that rates would stay higher.

While July saw an increase in funds to long-term treasuries, it was also the month with the largest short position. Well known investors such as Bill Ackman were vocal about shorting treasuries, stating long duration yields could climb up to 5.5% or above.

Those trades have seemed to pay off, as prices move inversely to yields.

Long term treasury ETFs are down about 9% this year.

The move up in longer-term yields has taken pressure off the Fed.

Markets now expect a pause in November (94% probability) and in December (70% probability).

It is increasingly likely that the Fed may be done with this hiking cycle.

If so, it could be a catalyst for sector rotation. Laggards, particularly Real Estate and Utilities,, could see some buying interest. These sectors, known for their dividends, have faced stiff competition against high, and increasing, short term rates.

Earnings

Earnings season unofficially kicked off with big banks reporting on October 12, 2023.

Over the last two weeks, one portfolio company reported earnings.

UnitedHealth Group beat across the board. The market had a positive reaction, with the stock moving up 2.5% against a -0.5% decline for the S&P 500.

United Health, a leader in health insurance, continues to have a compelling growth story as they successfully expand into value-based care, pharmacy offerings, and more.

Agree Realty (ADC)

Founded by Richard Agree in 1971 and originally named Agree Development Company, Agree Realty owns and operates over 2,000 properties across 49 states.

Joey Agree, Richard Agree’s son, was named CEO in 2013. Joey has been a transformational leader, driving ADC’s growth from $300 million micro-cap development REIT to a $8+ billion market leading REIT.

Joey Agree’s initiatives include focusing on highly valuable risk-reward opportunities such as triple net leases & ground leases, building a portfolio of high-quality investment grade tenants, clearly outlining their focus on “rethinking retail”, building out investor relations, initiating a monthly dividend, amongst many others.

Today, Agree Realty is one of the highest quality REITs, with a resilient customer base and boasting one of the strongest balance sheets.

About 68% of annualized base rents come from investment grade retail tenants.

They are prudently diversified across sectors in the retail space, with a strong focus on recession resistant areas such as grocery stores, auto service, dollar stores, convenience stores, and more.

The portfolio is 99.7% leased with a weighted-average remaining lease term of approximately 8.6 years.

While ADC still does some development, the majority of their business is back-to-back. They essentially borrow or raise money at x% and put it to work at x+y%, making a healthy spread.

The table below shows their cost of debt.

About 84% of their $2.16 billion in debt comes from senior unsecured notes with yields below 4.5%. Some call outs:

$300 million is locked in at 2.13% until 2033

$350 million is locked in at 2.11% until 2028

The maturity schedule (i.e. when the debt is due) is very attractive, with no debt due imminently. They have plenty of time for markets to settle before needing to refinance or pay off debt.

Recently, they announced a new unsecured $350 million 5.5-year term loan at a 4.52% fixed rate. They are still able to get attractive financing even as rates have risen dramatically.

As for putting the capital to work, in the most recent quarter, they acquired properties at a weighted-average capitalization rate of 6.8% and had a weighted-average remaining lease term of approximately 9.9 years.

The spread is very apparent. That is the crux of the business – bridging the gap between capital markets and real estate cap rates.

As we have seen with the debt issuance, management has been savvy in raising capital.

They have also done so with equity. (Note that shares trade at ~$55 today.)

With attractive opportunities to raise capital and invest, ADC issued common stock at prices ~$65-66/share over the last 3 years.

The company has similar agreements this year.

“…the Company has entered into forward sale agreements through June 30, 2023 to sell an aggregate of 5,036,229 shares of common stock, for anticipated net proceeds of $345.6 million.”

This agreement implies that ADC sold shares forward this year at a price of nearly $69/share.

With the deterioration in the REIT market and a current share price of ~$55, these forward sales have turned out to be good moves.

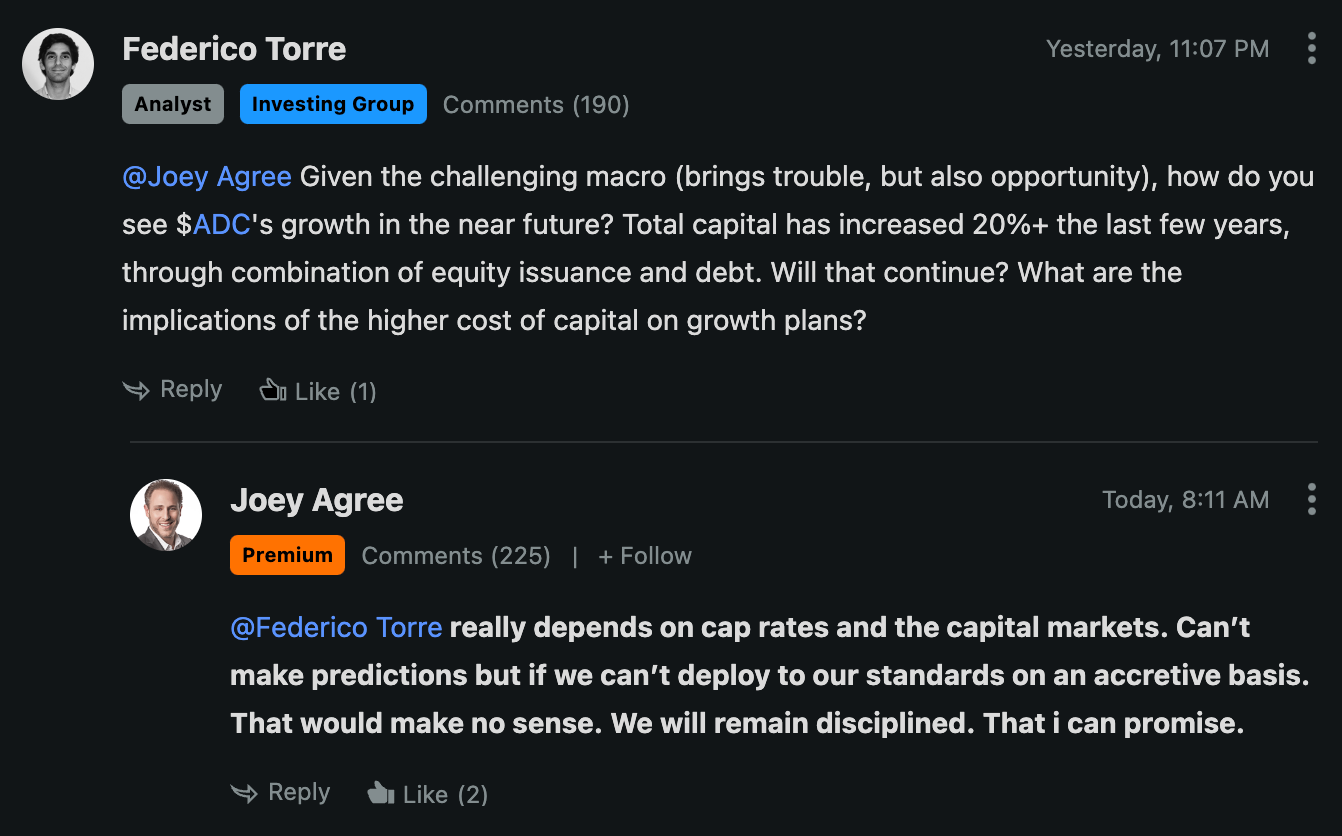

Management believes the current dip is an opportunity – they have been active with insider purchases all year. Year-to-date insiders have purchased over $10 million worth of shares, starting this year at $67.85 and most recently $53-55.

Joey Agree is quite active on SeekingAlpha, frequently responding to any questions people have in the comments.

Agree Realty CEO, director discloses purchase of 30,000 shares (NYSE:ADC) | Seeking Alpha

Perception Is Not The Reality: 2 REITs I'm Buying All The Way Down

Turning to the financials:

Revenue growth has been consistent, resilient even throughout COVID. In fact, the portfolio remained 99%+ leased throughout 2020.

Operating expenses primarily include depreciation, given the majority of the business is invested in hard real estate assets.

Adjusted EBITDA comes in at a high margin of 89-90%, which is expected and good to see. The business is basically collecting rents.

ADC continues to acquire new assets, deploying some $300-$400 million per quarter.

Debt balances have increased over time, as the company continues to grow. As long as it is being put to work in accretive investments, this shouldn’t be concerning.

Share counts continue to increase, seemingly quite dramatically. Again, this is a form of raising capital. As long as management puts it to work in a productive manner, it can be beneficial to shareholders.

The proof comes in the per share metrics. Revenue/share increased from $4.6 a year ago to $5.0 in the most recent quarter. EBITDA/share increased from $4.1 a year ago to $4.5 in the most recent quarter. This is very important, and good to see trending in the correct direction.

The share price was mostly range bound from 2021 up until the summer of 2023. Recently, shares dropped off a cliff, falling more than 20% in a couple of months. ADC is not alone in this – the broader REIT index has seen similar effects.

The primary driver is the macroeconomic backdrop – rates and commercial real estate.

With rates staying higher for longer, inventors looking for yield have more options. If the Fed is finished raising interest rates, that could be a catalyst for reversal.

The commercial real estate market is currently seen as unstable. There is a significant amount of debt maturing. Real estate assets are worth less, again due to higher rates. This combination can lead to mark downs, fire sales, and a significant sell off. The office sector is the poster child for this.

All that being said, ADC is fundamentally sound. With one of the strongest balance sheets across all REITs, they are best prepared to take advantage of any real estate crisis & scoop up assets at bargain prices.

As for valuation:

ADC trades at an EV/NTM EBITDA multiple of 15.7x. This is rather appropriately priced, indicating a yield of 6.4%.

REITs are commonly valued by funds from operations (“FFO”)/share.

Fastgraphs provides a good look.

Since Joey Agree took the helm in 2013, FFO/share has increased steadily from $2.13 to $3.95 for 2023. Shares haven’t traded at these multiples since 2015.

If shares were to trade near their average historical multiple over the next 5 years, investors could see annualized returns in the 10-15% range.

This return is inclusive of the dividend, which offers a forward yield of ~5.5% paid out monthly.

Closing thoughts

Agree Realty is the sole REIT in our portfolio. Although it is quite different from other holdings, it is one of the highest quality players in its space. The strength and commitment of the management team is very evident – this is not easy to find.

Agree Realty contributes significantly to the overall portfolio composition, providing uncorrelated movement and valuable diversification.

Although it has been a difficult position to hold these last few months, the combination of monthly cash flow and opportunity for capital appreciation is attractive.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.