Market, Earnings, and Atlassian (TEAM) - April 27, 2024

Market commentary, portfolio company earnings results, and a deeper look into Atlassian (TEAM)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

The market is experiencing a technical correction, having pulled back nearly 6% from the peak before bouncing back.

Volatility has picked up over the last few weeks, with 1-2% moves seemingly becoming the norm.

The decline accelerated as the index fell below the 50-day simple moving average (SMA). The market is sitting just below the technical indicator.

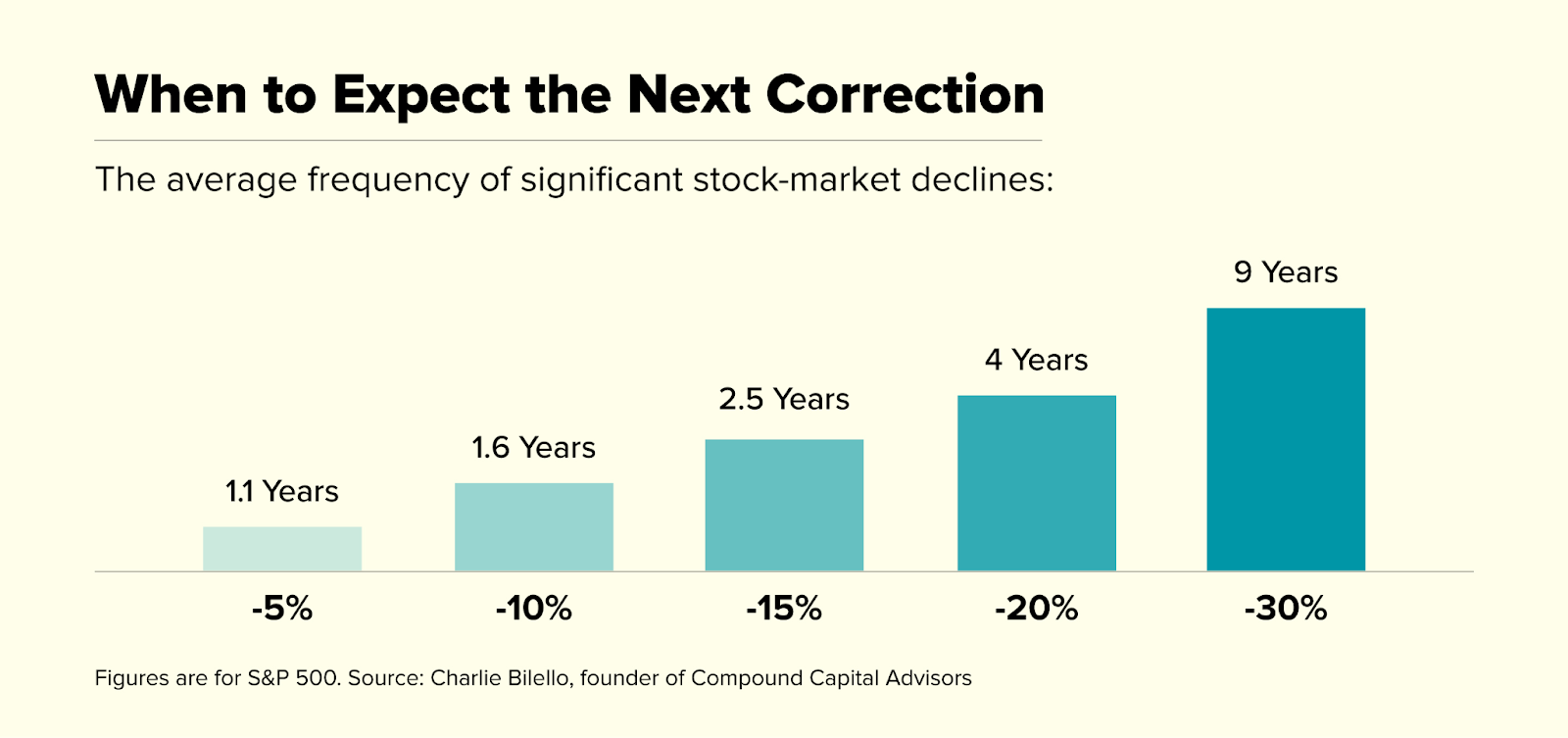

A 6% pullback is normal and even healthy. Drawing from historical data, a 5% decline can be expected every 1.1 years and a 10% decline every 1.6 years.

The backdrop and broader trend remains bullish. The next week or two will be informative as the technical picture unfolds and first quarter earnings continue to roll in.

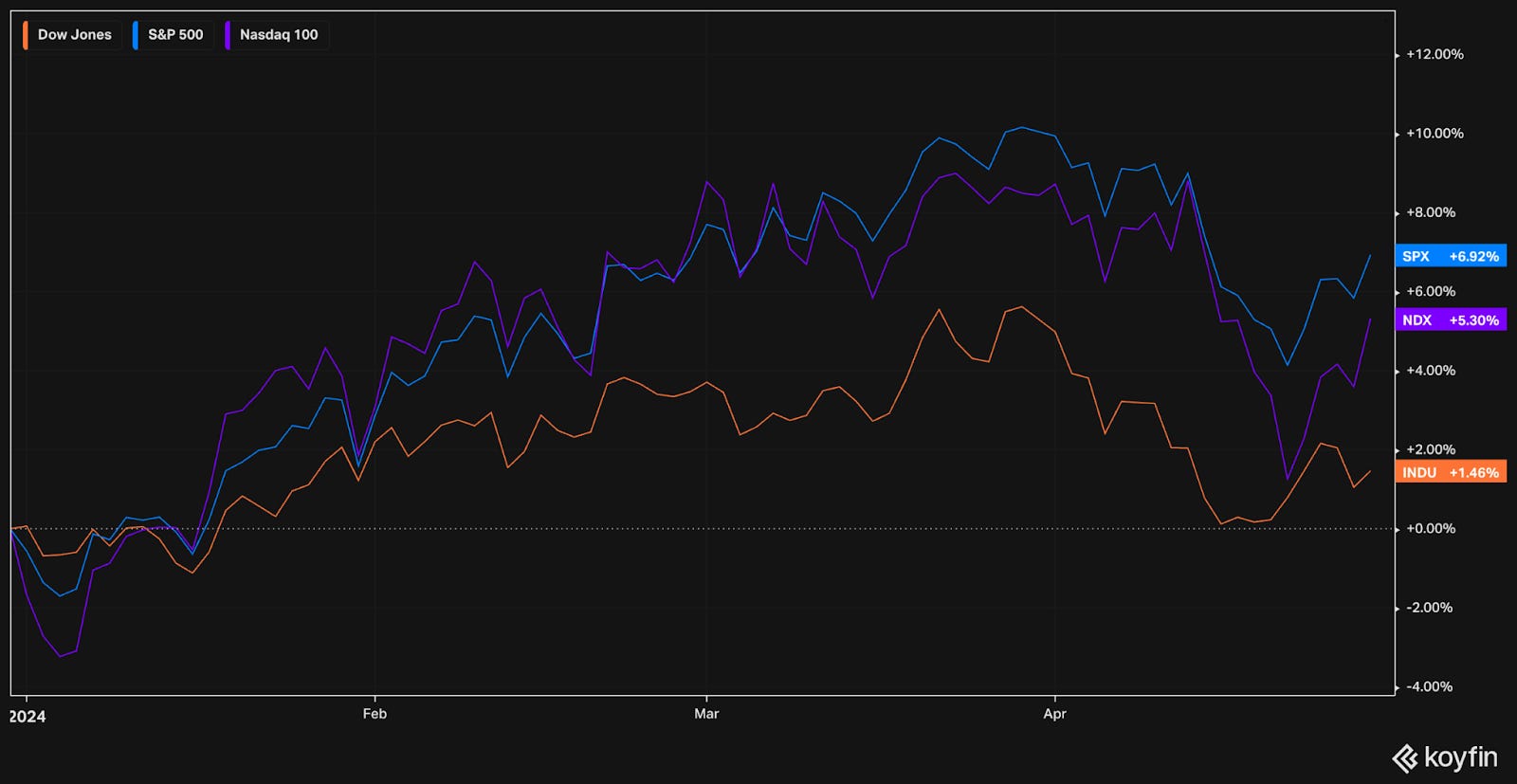

Year-to-date performance across indices:

S&P 500 +6.9%

Nasdaq +5.3%

Dow Jones +1.5%

Yields have been climbing all year, side-by-side equities for the beginning. The US 2-year treasury yield recently crossed above 5%.

The last time the 2-year treasury reached 5% was in July 2023. That was right about when volatility started, driving the market down to the October low. As rates started coming down below 5%, the market started building confidence and climbing.

As for sector performance year-to-date, leadership and laggards have been mostly consistent. Energy (XLE) continues to benefit from higher rates. Real estate (XLRE) continues to lag.

Notably, technology (XLK) is now in the middle of the pack.

Rate cut expectations continue to push out further. The market is not expecting a rate cut until at least September. Even so, the odds of a hike in September or November are rather low.

Earnings

Ten portfolio companies reported earnings over the last 2 weeks.

Atlassian (TEAM) – Initial Coverage

“Our mission is to help unleash the potential of every team.”

Founded in 2002 by college graduates Scott Farquhar and Mike Cannon-Brookes, Atlassian has become a powerhouse in digital productivity tools for team collaboration.

While their friends took jobs at prestigious companies upon graduating, Scott and Mike were set on paving their own path. They did not want to conform to the politics and bureaucracy of corporate life.

Based in Sydney, Australia, they started offering technical support services to companies across the globe, primarily in the USA. They were doing all the work themselves.

In an effort to streamline their workflows, they started building a bug tracking tool. Soon thereafter they realized their customers could benefit from their tool and they’d be able to secure recurring revenue by selling the software instead of troubleshooting services.

Jira, the original bug tracking tool, was launched in 2002.

Confluence, an internal documentation tool, was launched in 2003.

By 2005, Atlassian had 1,000 customers.

By the end of the 10th year, Atlassian reached $100 million in revenue.

Jira Service Desk, an IT ticket management system, launched in 2013.

The company IPO’d in 2015.

In 2021, Atlassian launched Jira Work Management, a project management suite of tools.

Customers purchase per-seat licenses for each individual product. As an example, the Jira pricing page is shown below.

Today, Atlassian has over 300,000 customers across nearly all industries, including NASA, Reddit, Rivian, Domino’s Pizza, and Paypal.

Annual recurring revenue is north of $4 billion and growing at 20-30%. They have a long runway with their current offerings, as many large companies continue prioritizing their digital transformation.

Atlassian has over 10,000 employees across 13 countries. Over 50% of employees are involved in R&D.

The company culture is exemplified by the core values.

Atlassian has a very long-term focus. They believe in building a company that can grow and prosper over decades. In multiple speaking events, they talk about building the company for the next 100 years.

Atlassian has demonstrated their ability to invest in R&D to drive innovation. In addition to the core offerings mentioned above, they have launched many other organic products including Bitbucket, Align, OpsGenie, Compass, Jira Product Discovery, Atlas. They have made acquisitions such as Trello and Loom and integrated them successfully. They continue to invest and build out new products through a formal program called Point A.

Atlassian is uniquely positioned to deliver value to companies and teams with AI. They have architected their platform such that they are able to build solutions once and integrate them across their product portfolio.

For a deeper look, tune into the upcoming investor day, Atlassian Team ‘24 on May 1st, 2024.

Diving into the financials:

TTM revenue grew 24% y/y. Although it has come down from the recent peak of 35%, the deceleration has been moderate when compared to other high growth companies. Growth appears to be steady in the 20s.

Gross margin came in at 82%. This is very strong, even within the software industry.

R&D expenses are nearly 50% of revenue. This is very high for a typical company. It demonstrates Atlassian’s commitment and opportunity for growth. Software companies have significant discretion in their level of spend here.

TTM EBITDA margin came in at 27%, and has been steadily increasing the last few years.

TTM FCF margin came in at 31%, also increasing over time and higher than EBITDA margins. This is a great sign, demonstrating their pricing power and ability to collect timely payments.

The balance sheet is strong, with over $2.1 billion in cash and less than $1 billion in debt.

Shares outstanding have increased more than 1% steadily over time. This seems acceptable given the combination of growth and profitability the company is driving.

Efficiency metrics EBITDA return on capital and FCF return on capital are very, very strong, reaching roughly 50%. The company has invested less than $2.4 billion in total capital since inception and is generating nearly $4.2 billion in revenue and $1.3 billion in FCF every year. This is very impressive and shows the effectiveness of the founders, the team, and the culture they have developed.

Looking at the chart:

The trend over the last year is mostly constructive. The stock sold off in February, and has exhibited some weakness since. Most recently, the stock gapped down as the company announced that Scott Farquhar, one of the founders, will be stepping back from the day-to-day operations.

More recently, the technical picture looks more challenging with the 50-day SMA crossing below the 200-day SMA, also known as the “death cross.” Some investors may prefer to wait until the stock builds support. The 170 level has provided support in the past.

As for valuation:

Atlassian has an enterprise value of $45.5 billion, or just below 10x NTM revenue.

The EV/NTM EBITDA of 45.5x seems high in absolute terms, yet justified for a high-quality, high-growth company.

FCF yield of 2.8% coupled with 24% revenue growth also seems very fair.

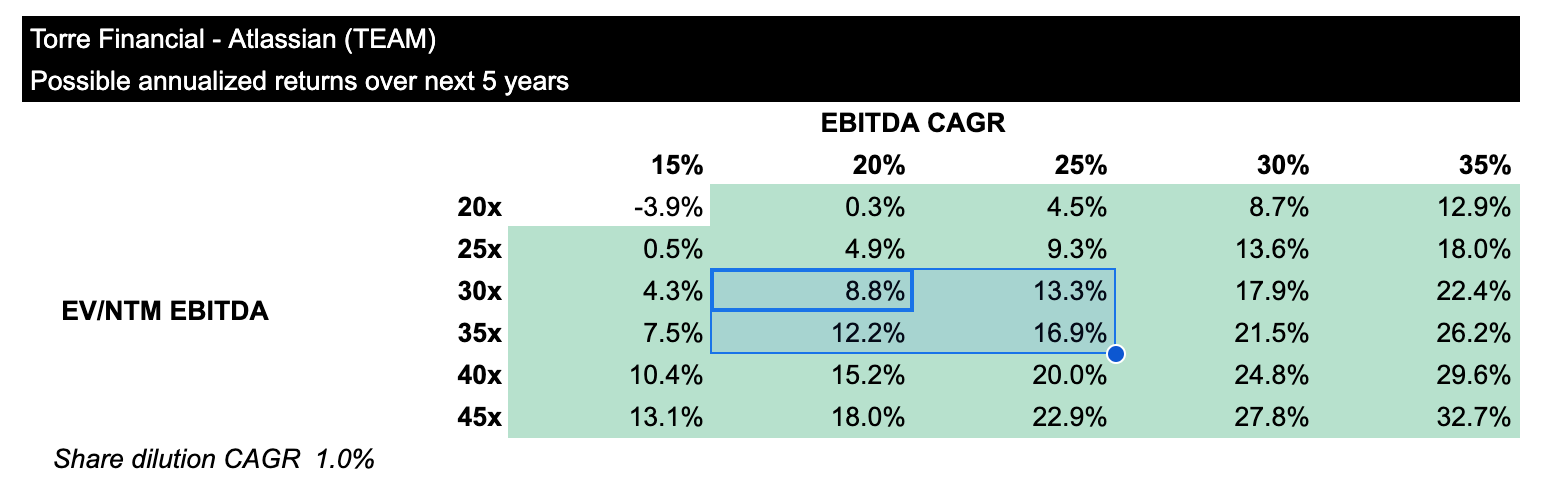

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 1.0%.

Analysts expect revenue to continue to grow at 20%+ and EBITDA to grow 20-30% per year over the next few years.

Assuming EV/NTM EBITDA multiples compress to 30x and EBITDA CAGR of 25%, investors could expect annual returns of 13.3% per year.

Fast Graphs provides another perspective.

Shares have historically traded at 61.5x P/FCF. Today, shares trade for nearly 40x. The stock has rarely traded below 40x.

If shares trade at the same 40x multiple in the future, the stock could return 21% per year.

If shares trade at down to 30x, shares could return 6.5% per year.

Closing

The pullback in the market is not unexpected. While they can be scary and unnerving, investors should keep their mind on what matters most.

Over the next year or two, rates are most likely going to be coming down. That will be supportive for all asset classes, including equities.

If inflation remains stubbornly high, that is because companies continue to charge ever higher prices. Companies with pricing power and asset-light companies that do not require capital to grow can continue to be successful in this environment.

Atlassian is a great example of a company that is well managed, highly effective, and able to grow without requiring significant amounts of capital.

At Torre Financial, we focus on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We assess primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

Next week we’ll hear earnings results for 10 portfolio companies, including Amazon, PayPal, American Tower, Mastercard, Booking, and more.

--

Torre Financial is an independent investment advisory firm focused on companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.