Market, Earnings, and DDOG - November 11, 2023

Market commentary, portfolio company earnings results, and a deeper look into Datadog (DDOG)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

The market has been on a tear — the S&P 500 is up nearly 8% in the last two weeks alone.

After passing the 200-day moving, the market took off. It jumped passed the 50-day moving average. The market sold off one day and found strong support at 50-day moving average.

This week closed out at 440.61, clearing the most recent high of 438 set on October 17. This is important as it breaks the lower-high pattern.

If the market holds above its current level, expect it to build momentum throughout the end of the year. The last couple of months of the year have been historically strong months.

Year-to-date performance across indices:

Nasdaq +41.95% (re-approaching the peak of 45%)

S&P 500 +15% (re-approaching the peak of 20%)

Dow Jones +3.43% (re-approaching the peak of 7.5%)

In our previous article, we mentioned “Cash-producing assets will become more attractive as interest rates begin to decline.” That turns out to be the case. Equities bounced back as long-term yields retraced.

Long term yields look to have peaked in late October — October 25th to be exact.

As an interesting aside, Bill Ackman of Pershing Square had been a vocal advocate of shorting long-term bonds, betting that yields would go up. Bond prices move inversely to yields.

He opened a short position in August and closed it out on October 23rd. His timing couldn’t have been more perfect — he sold out almost exactly at the top.

Why did long term yields decline?

Employment data came in below expectations. Unemployment ticked up to 3.9% vs. 3.8% expected.

The Fed seems to be done with rate hikes. In a recent conference, Powell commented “We’re in the place where we have restrictive policy, and probably significantly restrictive policy, and we’re watching the effect carefully on the economy.”

The US treasury reduced the amount of debt it planned.

Inflation is also supportive, holding steady at 3%.

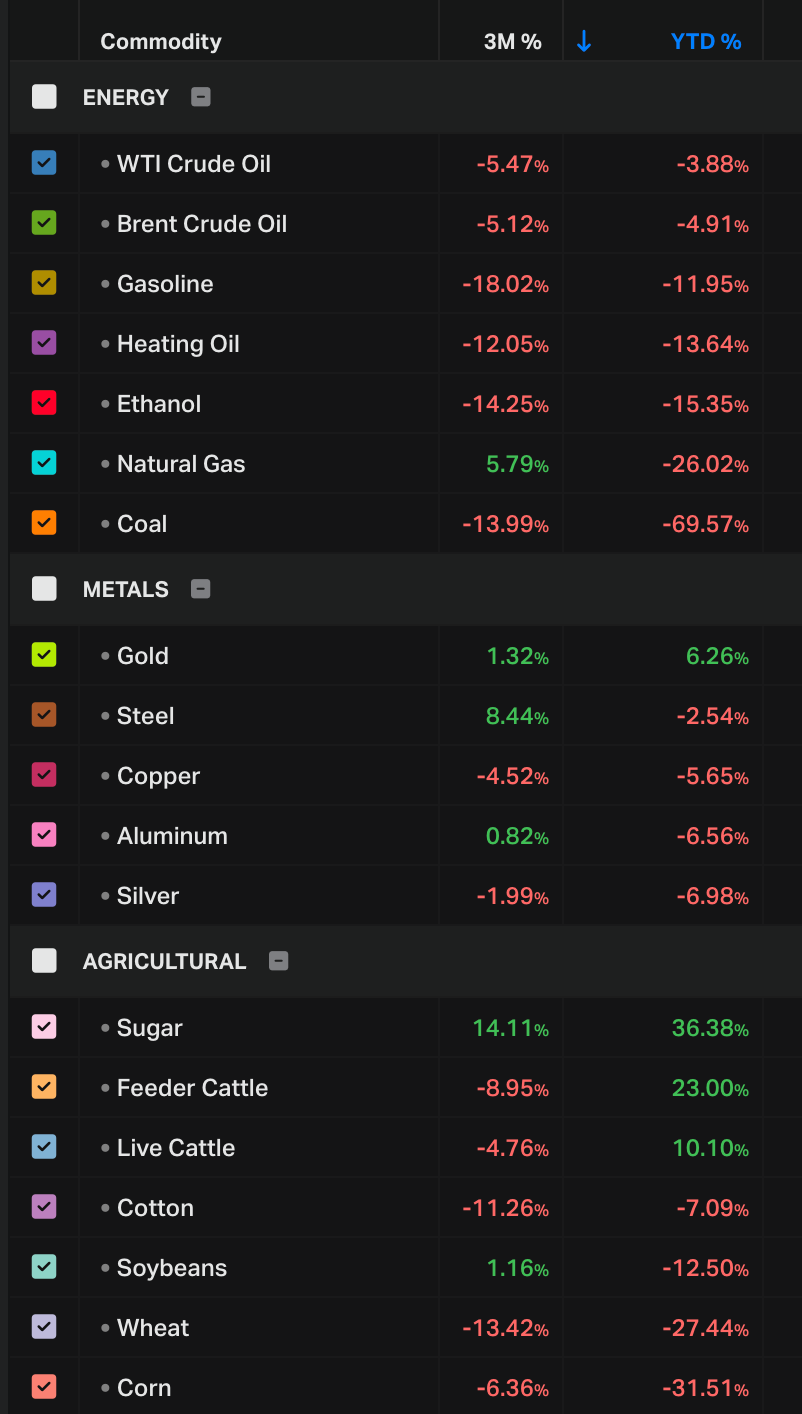

Underlying inflation, commodities are seeing significant pressure this year. Energy is down significantly; metals are mostly flat; agriculture is even on average. Lower commodity prices lead to lower inflation, which helps ease up on rates.

Growth companies have benefitted. Growth investing has been a particularly successful style this year. In fact, it is the only style that has outperformed the S&P 500.

The primary drivers are the “Magnificent Seven”: Alphabet, Amazon, Apple, Meta, Microsoft, Tesla, and Nvidia. These are the top 7 companies in the index, and they are up between 44% and 230% YTD.

Earnings

Over the last two weeks, 8 portfolio companies reported earnings.

Some notable callouts:

Paycom (PAYC) issued much lower guidance than expected. Shares cratered after hours, dropping nearly 40%. CEO Chad Richison explained that their new self-service payroll offering, BETI, is cannibalizing revenue. As employees validate their own payroll, errors are reduced and therefore reduce the need for any additional forms, processing, and other corrective measures. If this proves to be the true reason for the slower growth, it demonstrates the power and value of their offering.

PayPal (PYPL) announced strong financial results. Transaction margin pressure seems to be stabilizing. Incoming CEO Alex Chriss held his first earnings call. He came across as a strong leader, focused on unlocking the full potential of the PayPal platform. In the last 12 months, buybacks have reduced share count by 5%. They are continuing to buy shares at the current price. They expect to buy another 1%+ of shares back this quarter.

Cloudflare (NET) is one of our earliest, emerging compounders. The company is innovative and moving quickly. Shares are pricey at 15.5x NTM/revenue, and they are barely positive. Revenue growth remained strong and they continue to show progress towards more mature profitability. Shares dipped nearly 10% in the after hours, but then rallied the next day closing up over 10%.

The Trade Desk (TDD) is a high quality, high growth company. This quarter they reported slightly lower guidance, acknowledging some of the uncertainty. The premium pricing demands perfection. Shares were down nearly 17% the following day.

Datadog (DDOG) is another pricey, high growth name. This earning season, they exceeded expectations, and provided a strong outlook. Shares jumped up over 20%. More details below.

There was significant post-earnings volatility these last two weeks. Notwithstanding, we remain very confident in the long term opportunities and execution of our portfolio companies.

Datadog (DDOG)

Olivier Pomel and Alexis Le-Quoc met while working at a SaaS company. Olivier was running the development team; Alexis was running the operations team. They became good friends, but noticed how difficult it was for their teams to get along.

They became keenly focused on reducing friction between their teams, an intersection now known as “DevOps”. They envisioned a system that would bring those groups together – collecting data about both applications and infrastructure in one place.

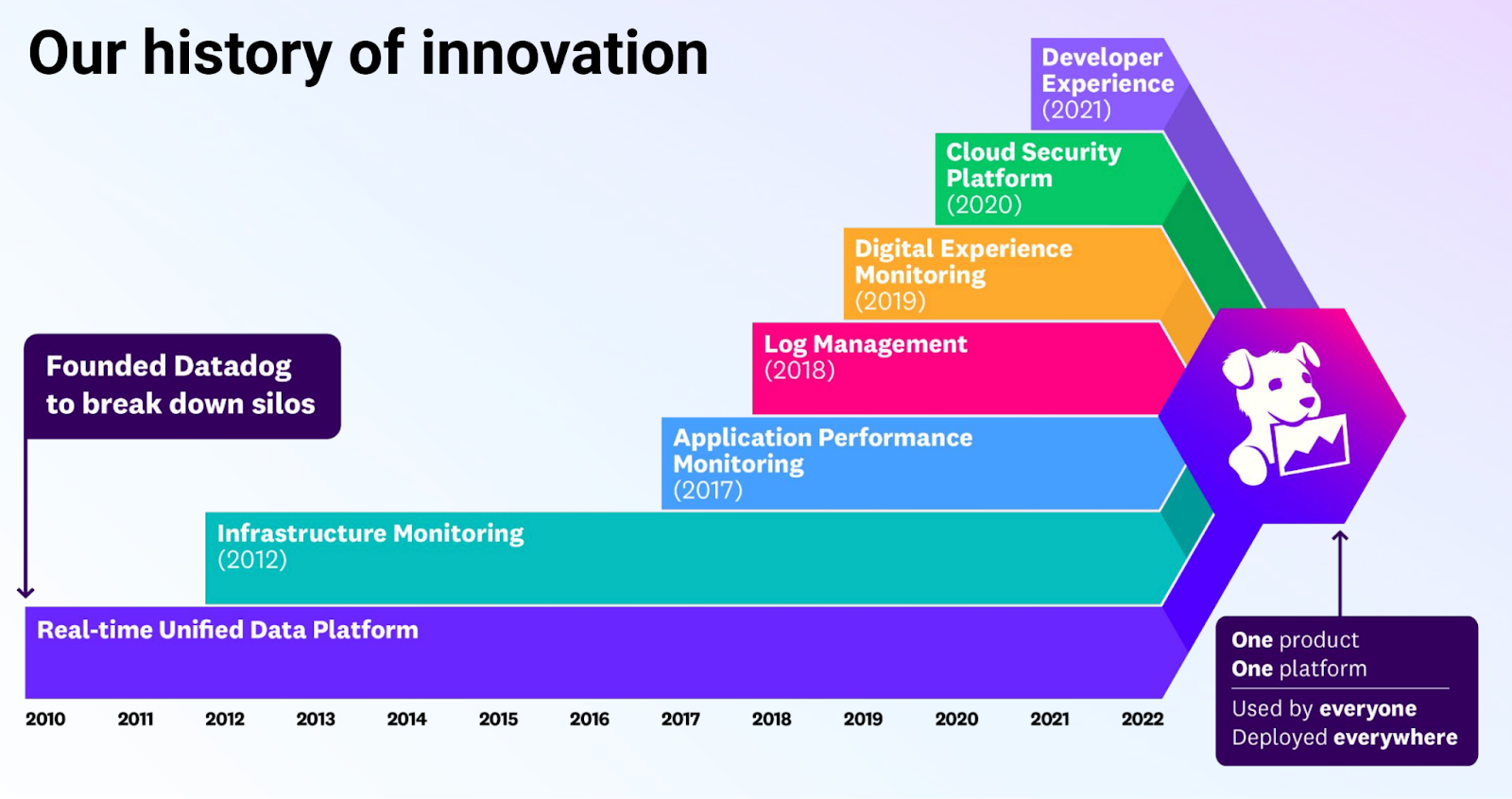

They founded Datadog in 2010 as one of the first cloud monitoring solutions.

What is a “monitoring” solution?

First, level setting on some basics:

Developers build applications by writing code. Software applications can have errors in them, often known as bugs.

Code gets deployed to servers (i.e. the “infrastructure”). Servers have limits – they have a certain amount of memory, CPU, etc. When pushed to the limit, a server might become unresponsive, or otherwise fail to do its job of serving the application to end users.

Any of these errors might cause an application to perform suboptimally, or not work at all.

For many companies, software applications are a critical part of their business.

Imagine if a bank’s website, or an e-commerce site is down. At the most extreme case, consider the cost of downtime for Google, which earns over $600 million per second from google.com.

Even degraded performance is costly. Amazon found that every 100ms in page load time cost them 1% in sales!

A monitoring solution provides the critical visibility into any issues happening on those servers. In the simplest of terms, Datadog provides a dashboard to see what is happening. They provide views, filters, metrics, alerts, and much more to help teams identify and proactively address any issue.

Datadog runs a consumption-based business model. In contrast to a seat-based model that charges per user, Datadog charges per usage – for example, # of servers or applications being monitored.

Datadog has a proven track record in innovation. They continue to stack new offerings and solutions on top of their platform.

Datadog serves around 27,000 customers – 82% use 2+ products, 46% use 4+ products, 21% use 6+ products.

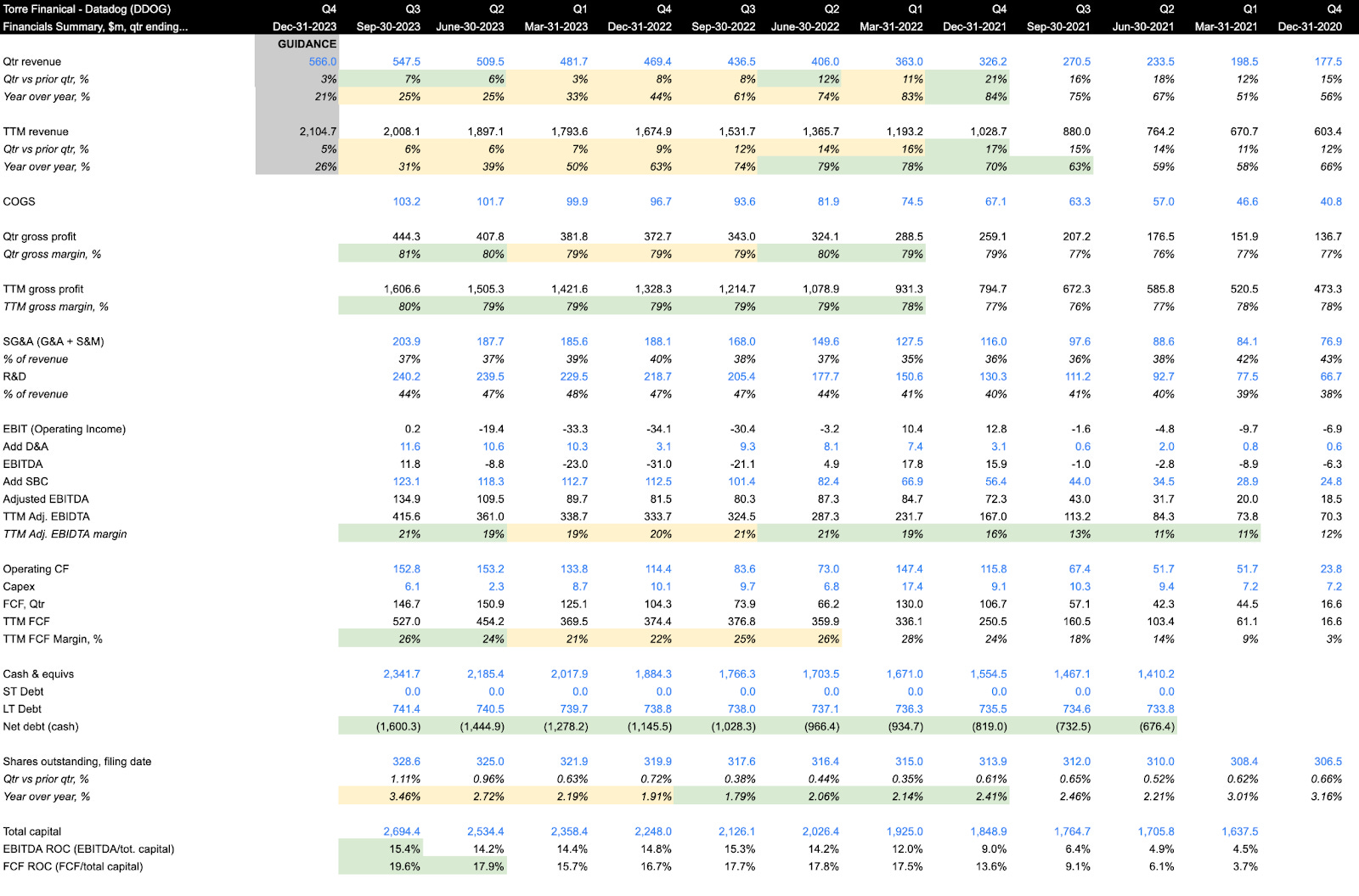

The company is profitable and in their short 14 year history have grown annual revenue to over $2 billion.

Turning to the financials:

Revenue growth in the low 20% range seems to be stabilizing. The last 2 quarters have had accelerating growth q/q.

Gross margin of 80% is best-in-class, and trending upwards.

EBITDA margins of 21%, also trending upwards.

FCF margin of 26% is very healthy, indicating a strong focus on converting income into FCF. A higher FCF margin is often due to charging customers upfront, an indication of pricing power.

The balance sheet is looking very good, with cash building up quarter over quarter. They have $2.34 billion in cash, up from $1.76 billion a year ago.

Share count is up 3.5% y/y, and showing an increasing trend. This dilution is primarily due to stock-based compensation. For a fast growing company with a clear opportunity ahead, dilution can be an effective way to drive execution. That being said, we would not like to see it go much higher. 1-2% is the preferred range; 3-4% is the maximum range. If there is dilution, there must be commensurate revenue growth.

Efficiency ratios are strong and improving. EBITDA return on capital is 15%; FCF return on capital is up to nearly 20%. Note that stock based compensation is included in the total capital denominator.

Similar to many other high growth software companies, Datadog shares have been on quite a roller coaster the last few years.

In 2021, the shares went on a steep climb. The company posted accelerating revenue growth, with annual growth rates of 51%, 67%, 75%, and 84% over those 4 quarters! Shares went from $60 to over $200.

Revenue growth started to stabilize in Q1 2022, and then slowly decelerated – 83%, 74%, 61%, 44%. Consumption slowed down as companies looked to optimize their spend. Shares came down from $200 to $80s.

Shares propped up in the first half of 2023, in anticipation of re-accelerating revenue growth. As that didn’t pan out, shares sold off at the end of the summer.

The most recent earnings call, however, added another point on the trendline demonstrating acceleration. Shares jumped up.

Momentum seems to be building, possibly implying a good risk-adjusted time to enter.

As for valuation:

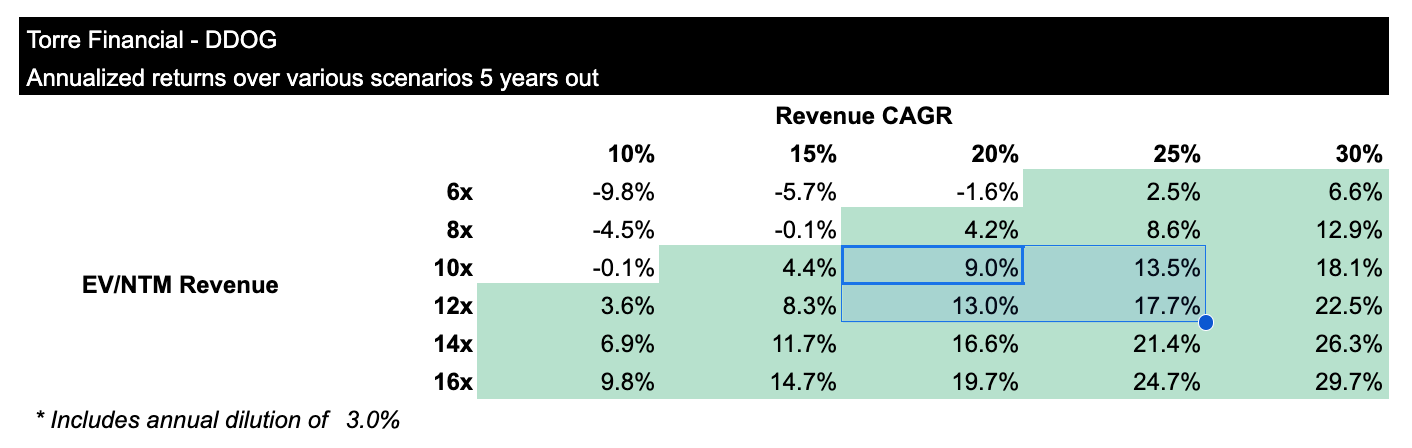

The company has an enterprise value of $32.5 billion and is expecting over $2.4 billion in revenue over the next 12 months.

A multiple of 13.3x on revenue and 55.7x on EBITDA is certainly not on the cheap side. The FCF yield of 1.6% – vs. treasury yields in the 4.5% area – helps put it further into context.

High quality companies tend to always appear “too expensive.” The compounding effects of 25%+ revenue growth, high profitability, and an innovation engine can lead to exponential growth. Humans intuitively underestimate exponential growth.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual dilution of 3%.

If revenue growth is maintained in the 20-25% range and the revenue multiple compresses slightly from 13.3x to 10-12x, shares could return between 9-18% per year.

Re-acceleration in revenue growth would result in outsized returns.

Closing thoughts

The macro landscape continues to evolve. Bad news is good news, as the weakening economy further solidifies the end of the rate hikes.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

We expect our companies to continue to post growth, even throughout weak economic times. The combination of continued growth with lower rates will be a tailwind across the portfolio.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.