Market, Earnings, and The Trade Desk (TTD) - February 17, 2024

Market commentary, portfolio company earnings results, and a deeper look into The Trade Desk (TTD)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

Throughout the week of February 5-9, the market pushed higher to gain another 1.6% and closed above the 500 milestone level.

Last week, however, the index pulled back slightly, losing 0.34% for the week. The index closed at 499.5.

The overall trend continues to favor the bulls. Momentum tends to be a strong force in the markets and certainly could keep driving markets higher. Investors have been eagerly buying the dip over the last few months.

That being said, the recent stall can create some doubt and give some investors a pause. Stalls can turn into inflection points rather quickly. After such a strong start to the year, a pullback would not be unexpected.

Year-to-date performance across indices:

Nasdaq +5.1%

S&P 500 +5.0%

Dow Jones +2.5%

The economy continues to chug along. In the most recent release, GDP growth came in at 3.3% quarter-over-quarter, a decline from the prior reading of 4.9% but still higher than prior readings in the 2% range.

Inflation came in higher than expected. For the month of January, CPI rose 0.3% month-over-month (m/m) vs. expectations of 0.2% m/m.

On an annualized basis, CPI was 3.1% y/y.

Markets adjusted quickly to the new data. Earlier in the year, cuts were expected as soon as March. Now, the first cut isn’t expected until June and that is only with a 59% chance.

Many assets, including equities and bonds, increase in value as interest rates decline. Given the recent climb, it seems markets have been anticipating these rate cuts. The more they get deferred, the more likely the market will get impatient.

Earnings

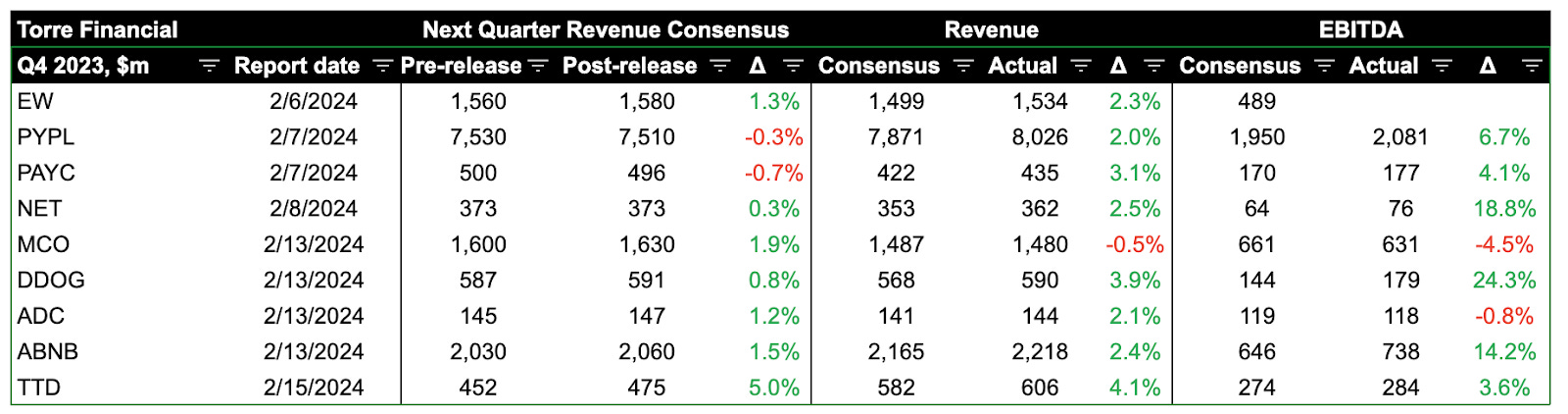

Over the last two weeks, 9 portfolio companies reported earnings.

The Trade Desk (TTD)

Prior coverage:

Market, Earnings, and TTD - August 19, 2023 TTD at $72.18

Earnings Review - November 19, 2022 TTD at $50.51

Founded in 2009 by CEO Jeff Green, The Trade Desk is a digital platform for buying advertisement placements known as “demand side platform.”

In short, The Trade Desk is essentially an open platform where advertisers can go to buy ads. They can place and understand the effectiveness of their ads across a wide range of properties.

In contrast, Google or Meta provide closed platforms. Advertisers can purchase ads from them and see their effectiveness, but only on their respective platforms.

For a deeper dive, see our coverage from August 2023.

TTD has been profitable since 2013 and has grown their revenue consistently over time.

They are an emerging leader in the advertising space and continue to drive innovation. One of the most important elements of effective ads is targeting the right audience – showing the right ad to the right person.

In an effort to enhance effectiveness, The Trade Desk has been spearheading an effort called “Unified ID 2.0”. TTD is building this open-source solution that converts an email address to an anonymized ID. Many leading organizations across industries have opted in. This is a win-win – companies that leverage it can get a better ROI on ad spend; more companies tend to opt in because of that; ads are overall more effective and better tracked.

Highlights from CEO Jeff Green on the most recent earnings call:

“I’m even more excited about 2024 and beyond. I’ve never felt more confident heading into a new year. I believe we are uniquely positioned to grow and gain market share not only in 2024, but well into the future, regardless of some of the pressures that our industry is facing, whether it’s cookie deprecation, growing regulatory focus on walled gardens, or the rapidly changing TV landscape.”

“Our platform is set up to make the most of any signal that can help advertisers drive relevance and value. Our platform now sees about 15 million advertising impression opportunities per second. And we effectively stack rank all of those impressions better than anyone else in the world based on probability of performance to any given advertiser—without the bias or conflict of interest that plague most walled gardens. With UID2, Kokai, and advances in AI in our platform, we now do this more effectively than ever before. And our work in areas such as CTV, retail data and identity are helping build a new identity and authentication fabric for the open internet.”

“The open internet will continue to challenge the walled gardens as the place where the very first advertising dollar is spent. Because for the most part premium content is outside of walled gardens and all the questionable user generated content is inside of walled gardens”

“Connected TV (CTV) continues to be the fastest-growing channel at scale for The Trade Desk.”

“The math is obvious, a dollar CPM turns into 70 cents with cookie deprecation. We’re often seeing a $1 dollar CPM turn into a $1.30+ when UID2 is layered on it. So, when publishers get to consider the contrast of $1.30 versus 70 cents—the math is more obvious than ever”

“We are reinforcing our position as the ad tech AI leader. We’ve been embedding AI into our platform since 2016, so it’s nothing new to us.”

Diving into the financials:

TTM revenue growth ticked down to 23%. Guidance calls for acceleration to 24%. Possibly indicative of an inflection point, growth seems to have steadied in the mid 20s and can increase from here.

Gross margin ticked up to 83% on a quarterly basis. Gross margin of over 80% is top tier. It tends to vary somewhat, likely due to seasonality. The TTM gross margin is much smoother, consistently between 81-82%.

TTM EBITDA margin came in at 39%. Slightly down from the recent peak of 43%, yet very strong nonetheless.

TTM FCF margin similarly ticked down to 28%, down from 33% the prior quarter. This looks to be due to increased capex, which appears to be an annual pattern.

The balance sheet is very strong, with net cash of $1.1 billion.

Shares outstanding have decreased year-over-year for the first time. This is quite meaningful. Dilution of 2% was not extreme for a fast growing company. Today the company continues to grow quickly and is also reducing outstanding shares.

Efficiency metrics – EBITDA return on capital and FCF return on capital – are both very strong in the 30s and 20s respectively. For every $100 invested in the business, TTD is generating $23 of free cash flow per year!

The Trade Desk share price has been volatile over the last few years. Like many other fast-growing companies, TTD’s share price declined through most of 2022 as the Fed was aggressively hiking interest rates.

Bottoming in January 2023, TTD shares were able to stage a steady comeback up climbing from ~$40 up to $90. The stock has been in consolidation since the summer of 2023.

In December 2023, the 200-day moving average crossed above the 50-day moving average. This is known as the “golden cross”. And, rightfully so, shares have moved up meaningfully since. The most recent earnings were met with enthusiasm, sending the stock up nearly 20%.

As for valuation:

The company has an enterprise value of $42 billion. From an EBITDA perspective, the multiple of 44x is not unreasonable. Standalone, it is a premium multiple. However, TTD is one of the highest performing companies in the market, considering revenue growth, gross margin, FCF margins, and efficiency.

From a revenue perspective, 17.8x seems steep. Since the company is already profitable however, the EBITDA multiple makes for a better assessment. For unprofitable companies, investors need to guesstimate what the profit margins will be. When a company is profitable, that data is known.

FCF yield of 1.3% is low, but again within the context of a 15-25% growth rate, it is not unreasonably expensive.

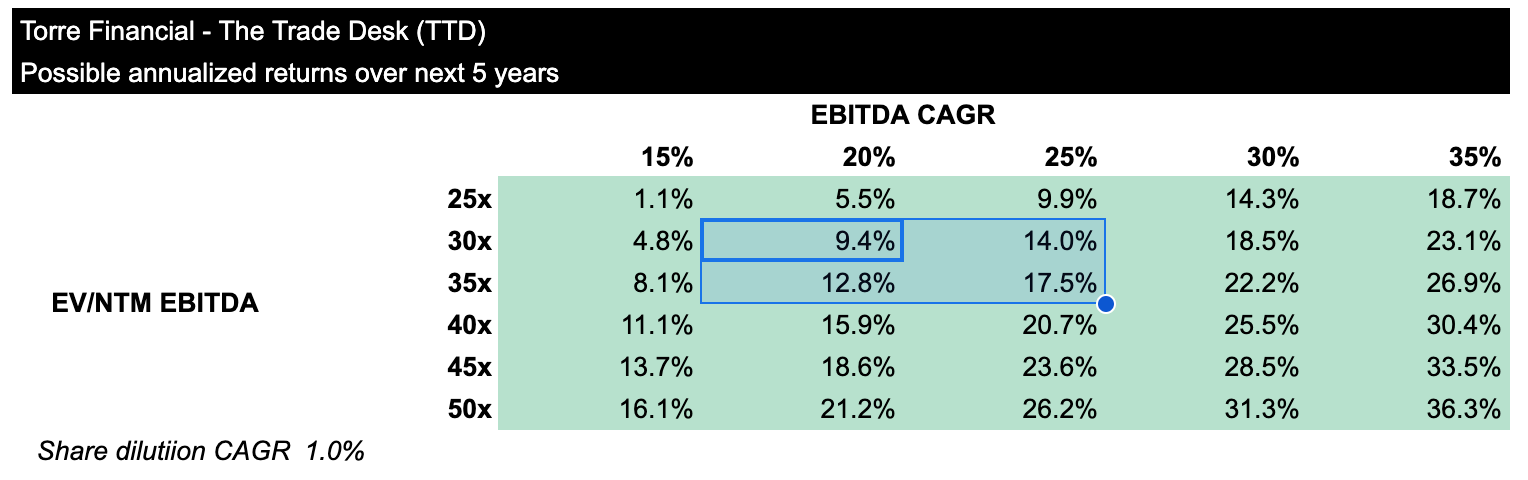

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 1%, in an effort to be conservative.

Analysts expect EBITDA to grow 24%, 22%, and 34% for FY 2024, FY 2025, and FY 2026 respectively.

Shares currently trade for 44x EV/NTM EBITDA. Notwithstanding, even at today’s price of $89, investors can still achieve double digit growth over the next 5 years.

On the lower range, if the multiple compresses to 35x and EBITDA grows at 20%, TTD shares could generate returns of 13% per year.

On the higher end, if the multiple is steady at 45x and EBITDA grows 25-30%, TTD shares could possibly generate returns of 24-28% per year!

Closing thoughts

The market’s undeterred climb from the October lows has been a boon for investors that have stayed invested. We remain cautiously optimistic today, acknowledging that there is certainly more volatility to come the rest of the year.

At Torre Financial, we’re always on the lookout for the best investment opportunities. We try to incorporate all the data we can to make the best informed decisions. We focus primarily on finding the best businesses and are, secondarily, attentive to valuation. Throughout the last few months we’ve been rotating from high-fliers to more sensibly valued portfolio companies. While TTD could be thought of as a high-flier due to its seemingly premium valuation, we find the valuation reasonable still today, given the quality and opportunity of the business.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.