Market, Earnings, and Workday (WDAY) - May 25, 2024

Market commentary, portfolio company earnings results, and a deeper look into Workday

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

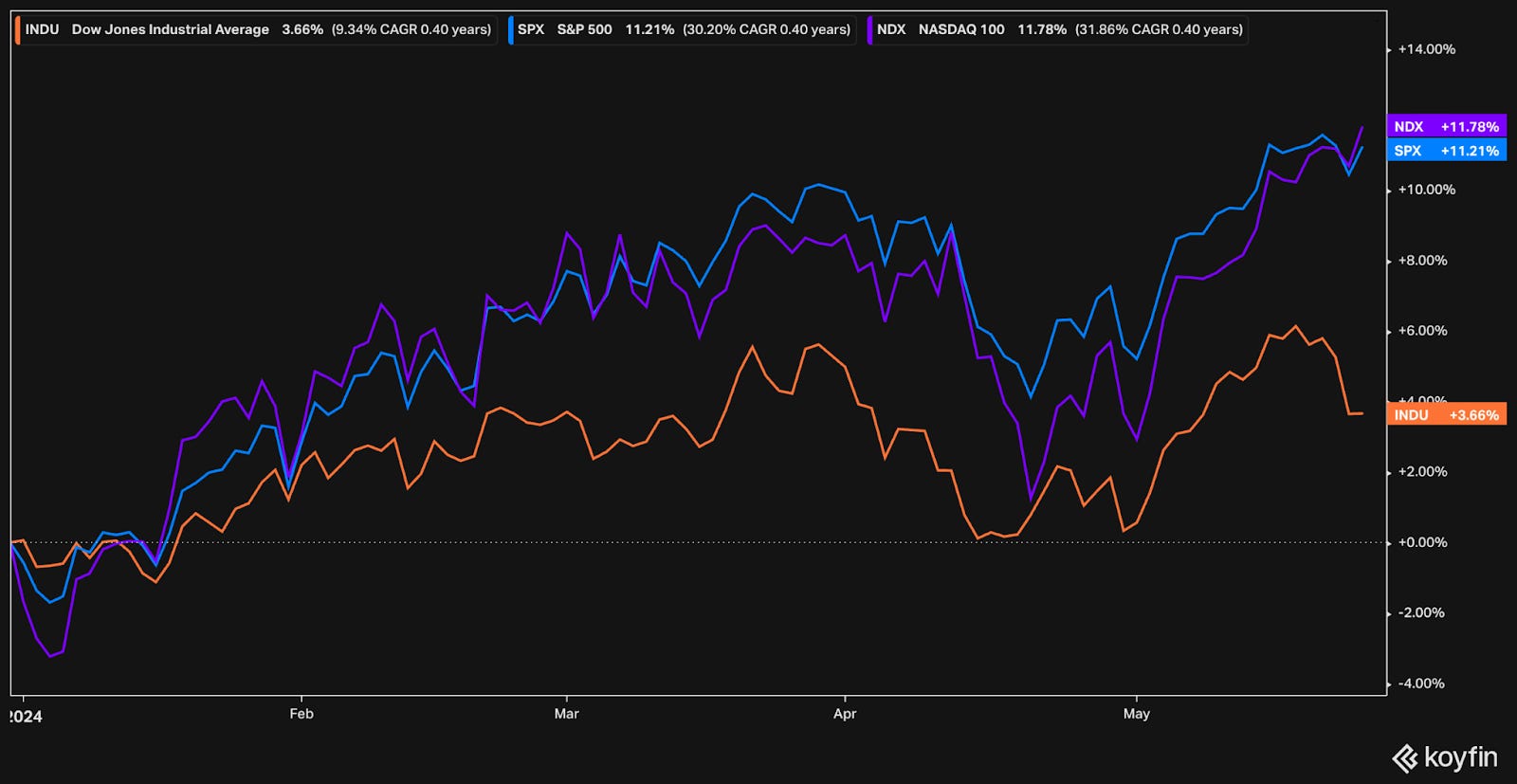

The S&P 500 broke through to another all time high. The swoon in April was short lived, as buyers stepped in and drove the market up for a consecutive 4 weeks. This last week, the 5th in the series, experienced more volatility yet was able to finish out flat.

The near-term price action may be foreboding. Volatility can breed more of itself, and the uncertainty can make investors nervous. That being said, the backdrop remains bullish as investors have been willing to step in on any sell off.

Year-to-date performance across indices:

Nasdaq +11.8%

S&P 500 +11.2%

Dow Jones +3.66%

The S&P 500 is currently going for a FCF yield of 2.96% and EV/NTM EBITDA of 15x, a premium compared to the 10-year averages of 3.78% and 12.6x respectively.

This week, all eyes were on Nvidia’s earnings report. Over a year ago, Nvidia became the AI poster child as demand for their GPU computer processors exploded. Once again, they blew past their own guidance and analysts’ estimates alike. Revenue for the quarter was up nearly 4x to $26 billion, up from $7.2 billion a year ago. Earnings grew 461%. They also announced a 10-for-1 split.

NVDA shares are up over 564% in the last 1.5 years, compared to 32% for the S&P 500.

CEO Jenson Huang confirmed there is no apparent slowdown in the demand for the chips that power artificial intelligence.

“All of the work that’s being done at all the [cloud service providers] are consuming every GPU that’s out there,” Huang said. “Customers are putting a lot of pressure on us to deliver the systems and stand it up as quickly as possible.

While the fundamentals have supported a meteoric rise, the stock seems to be building on its momentum. Momentum can be a powerful force. In either direction.

As for the broader market, things are calm. The VIX put in a new low at 11.92.

The rate narrative continues to be a driving force in the market.

The Fed released the minutes from their last meeting, wherein some members "mentioned a willingness to tighten policy further should risks to inflation materialize in a way that such an action became appropriate." That release pressured the market.

At the same time, Fed Chair Jerome Powell commented during a press conference at the end of that meeting: "I think it's unlikely that the next policy rate move will be a hike."

The action was sufficient to drive yields up. The 2-year treasury moved up to 4.96% while the 10-year inched up to 4.47%.

The market is still expecting rate cuts to come in this year, possibly as soon as September, if not by November.

Earnings

Two portfolio companies reported earnings over the last 2 weeks.

Workday (WDAY)

Prior coverage: Market & Earnings Review - May 27, 2023

Workday is a cloud leader in human capital management (HCM) and financial management software. They serve large enterprises and help them take care of their most important assets: people and money.

Workday services over 10,000 organizations, including 60% of the Fortune 500. Retention is strong with 100%+ net revenue retention and 98% gross revenue retention rate.

Workday has a proven track record in building and innovating for their large enterprise customers. From modules on the HCM platform, to AI features, or even an entirely new offering, Workday has been able to deliver results. Having started with HCM, Workday now offers applications for financial management, spend management, planning, and analytics and benchmarking.

About 75% of the financial management software market remains on-premise. Workday is well-positioned at the heart of those digital transformation efforts.

Workday has been invested in and developing AI for many years. With the recent macro attention, Workday has made it a focus to better enable their customers with AI. They have built over 50 features including the ability to generate job descriptions, write annual reviews, and much more.

After being co-CEO for over a year, Carl Eschenbach became the sole CEO on February 1, 2024. Former co-CEO and co-founder Aneel Bhusri is still at the company, more focused on strategic plans and growth initiatives. Prior to Workday, Carl was a general partner for more than 6 years at venture capital firm Sequoia Capital.

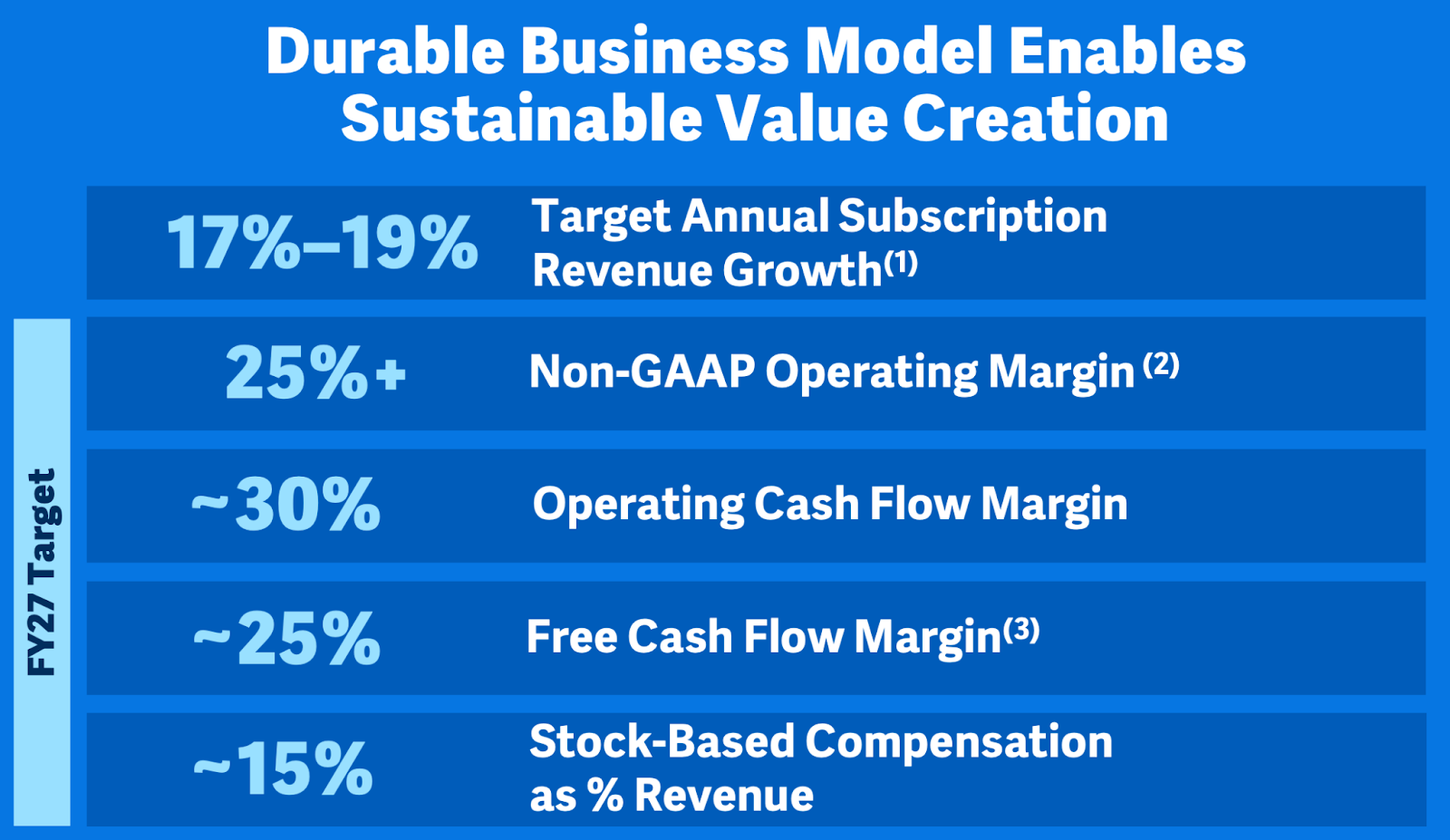

The company is very confident in their ability to deliver over the long term. In their 2023 financial analyst day, Workday released long term targets for FY2027. Strong, durable revenue growth coupled with profitability and a clear competitive advantage is exactly what we look for.

On Thursday, Workday released their Q1 earnings.

Results for the quarter were strong. Revenue came in at $1.99 billion, ahead of consensus estimates of $1.97 billion. EBITDA was $590, also beating estimates of $559 by 5.5%

Full year revenue guidance for the year – which was just set in the prior quarter – was lowered by roughly $35 million. While not particularly significant, it is not a great sign when guidance is revised downwards just a few months in.

On the positive side, the company also revised their adjusted operating margin forecast to 25%, up from 24.5%.

CFO Zane Rowe commented on the earnings call: "Our updated subscription revenue guidance reflects the elevated sales scrutiny and lower customer headcount growth we experienced during the quarter. At the same time, we are increasing our margin outlook as we focus on driving increased efficiencies across the company."

Also mentioned on the call, whereas before they would sell the HCM and/or finance offerings separately, new customers have been evaluating the full platform. While this introduces more decision makers to the process and can draw it out, it can also uncover differentiated capabilities to give Workday the edge and closer larger deals.

Diving into the financials:

TTM revenue held steady at 17% y/y. This quarter’s revenue came in above, at 18%, while guidance is just under at 16%. Net, net, it seems like Workday’s revenue growth is holding steady. Acceleration would be a very positive catalyst.

TTM gross margin was steady at 76%. The trend has been positive, with incremental improvement nearly every quarter over the last year and half.

EBITDA margins have also been ticking up now at 26%. It is great to see those gross margin efficiencies trickle through.

FCF margins are also strong at a similar 26%. Strong EBITDA-FCF conversion demonstrates pricing power and ability to collect on those sales.

The balance sheet is very strong, with over $7 billion in cash & equivalents and less than $3 billion in debt.

Shares outstanding increased 1.3% y/y. This is a very reasonable amount for the combination of growth and profitability. Another positive note is the trend – dilution used to be as high as 4-5% y/y in years past. That has come down significantly to a much more reasonable level.

Efficiency metrics look very strong, with EBITDA return on capital and FCF return on capital both at 27%. This shows that any use of additional capital has been put to good use.

Taking a look at the chart:

Workday shares have been in a relative uptrend over the last year. The SMA indicators are trending positively, and the shares held above the 50-day for the majority of the first half.

In February, Workday announced Q4 results and initiated their full year guidance. The stock sold off and looks to have initiated a downtrend. In May, Workday announced Q1 results and revised their revenue guidance for the year downwards. The stock sold off 15%.

The technical picture seems to be deteriorating. It is likely that the 50-day SMA will cross below the 200-day SMA shortly, putting in a “death cross.” While the long-term opportunity is still in play, the shares may experience heightened volatility before continuing upwards.

As for valuation:

Shares trade for 6.2x EV/NTM revenue or 22.3x EV/NTM.

The FCF yield is 3.68% at current prices. The S&P 500 has a FCF yield of 2.96% and is growing at a much lower rate than Workday.

The valuation is not demanding for such a high quality company with strong growth, sticky offerings, and a long runway.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 0%.

Over the next 5 years, if the multiple compresses to 20x and EBITDA is able to grow at 18% (just slightly above revenue growth), shares could return 12% per year.

Fast Graphs provides another perspective.

At $220.91, shares are right around the fair value multiple of 30x FCF. If the estimates play out and shares trade at 30x in the future, WDAY could return 15-16% per year.

Closing

Markets will always fluctuate – they will be expensive, cheap, growing, not growing, etc. Knowing where the market will go is a fool’s errand. Even sometimes being right can be wrong if the timing is off. The expensive can get more expensive; the cheap can get cheaper.

Our approach is to stay invested in equities, because we know that over time they will generate the best returns.

At Torre Financial, we focus on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We assess primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

Workday looks to be a compelling opportunity today. While it may or may not pay off immediately this year, the company is set up for success in the long term. As they move past these transient headwinds over the course of the year, investors are likely to be rewarded.

--

Torre Financial is an independent investment advisory firm focused on companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.