Notes on 100 to 1 in the Stock Market by Thomas Phelps

Insights, learnings, and advice from a comprehensive study on companies that have grown more than 100x

“To make money in stocks, you must have vision to see, courage to buy and patience to hold. Patience is the rarest of the three.”

-Thomas Phelps

Having started his career at the Wall Street Journal, Thomas William Phelps (1902-1992) spent over 40 years in the investing world working as an investor, columnist, analyst, and financial advisor. In his quest to understand the markets, he was intrigued by the unimaginable success certain companies were able to achieve, many returning more than 100x an initial investment.

Originally published in 1972, 100 to 1 in the Stock Market is a study on those “100-baggers,” exploring the space and drawing insights on common characteristics in an attempt to identify opportunities early on.

In order to achieve 100-bagger status, a company must maintain high growth rates consistently over many years. The following chart shows how many years it would take for an investment to 100x given various compound annual growth rates, or annualized returns.

To achieve a 100x return on an investment in 30 years would require consistent returns of roughly 16.6%.

To achieve a 100x return on an investment in 20 years would require consistent returns of roughly 25.9%.

Although these numbers may seem beyond grasp, they are achievable. A sample of companies in Phelps’ study that have returned 100x includes Abbot Laboratories, American Express, Black & Decker, Disney, Deere, General Dynamics, Lockheed, Merck, 3M, Schlumberger, and Whirlpool.

Traits of 100-Baggers

“The reason that more people don’t make 10,000% on their money is that they don’t set their goals high enough!”

In the book, Phelps suggests looking for smaller, unknown companies that have progressive, research-minded management. These companies are best positioned for extended periods of high growth.

“When looking for the biggest game, never ever, shoot at anything small.”

An investor has to be able to envision the company operating at scales multiple times larger than the present day. Imagine a company operating at 10x, 50x, 100x the scale they currently operate at and assess the feasibility of those scenarios.

He specifically recommends looking for companies that address the following concerns:

Inventions that enable us to do things we have always wanted to do but could never do before.

New methods or new equipment that helps people do commonplace things easier, faster or at less cost than ever before.

Processes or equipment to improve or maintain the quality of a service while reducing or eliminating the labor required.

New and cheaper sources of energy.

New methods of doing essential jobs with less or no ecological damage.

Improved methods or equipment for recycling the materials used by civilized man instead of making mountains of waste and oceans of sewage.

New methods for delivering the morning newspaper without carriers or waste.

New methods or equipment for transporting people and goods on land without wheels.

He also dwells on “gates,” today often referred to as competitive advantages, moat, or barriers to entry.

How high and strong is the company’s “gate” against competition? If others can enter the business easily, the above average rate of return is bound to be whittled down.

How good are the prospects for sales growth? No matter how high the rate of return, the company cannot grow by plowing back earnings if it already has enough capacity to supply all foreseeable markets.

Growth Factors

The last comment is worth echoing.

“No matter how high the rate of return, the company cannot grow by plowing back earnings if it already has enough capacity to supply all foreseeable markets.”

A strong moat is insufficient to drive strong returns. Companies need to have opportunities for continued growth.

Phelps calls out the following factors as important contributors to growth:

Reinvesting earnings at a constant or rising rate of return on invested capital, above the average of around 9 percent.

Investing borrowed money to earn more than the cost of borrowing

Acquiring other companies by exchange of stock at lower price-earnings ratios for the companies acquired than for the company acquiring them

Increasing sales without having to increase invested capital. The greatest opportunities to do this are found in companies operating far below capacity. New methods, increasing efficiency, may have the same effect.

Discoveries of natural resources, such as a great new oil field, gold mine, or nickel deposit.

New inventions, processes, or formulas for filling human needs not previously met, or for doing essential old jobs better, faster, and/or cheaper.

Contracts to operate facilities for others, usually governments.

Rising price-earnings ratios.

More tactically, Phelps suggests that investors should closely monitor a company’s progress on the following criteria as indicators around the health of the business:

Sales growth

Profit margins

Rate of return on book value (equity)

Rate of return on invested capital

Ratio of sales to invested capital

Buildup of book value

While growth in share price is likely to follow the fundamental performance of a business, the market can create opportunity for additional returns through volatility in valuation. Consistent with guidance towards undiscovered stocks, Phelps encourages investors to look for opportunities of multiple expansion: The greatest gains in the market have been made by simultaneous increase of earnings along with increase in PE.

Buy and Hold

“Perhaps the greatest advantage of all in buying top quality stocks without visible ceilings on their growth is that when we do so we give ourselves the chance to profit by the unforeseeable and the incalculable.”

Phelps advocates that successful investors typically hold stocks for more than 10 years, often 20 or more.

“Far more money can be made by good stock selection, than by good market timing.”

Phelps acknowledges that money can be made by trading and timing the market, although cautions each investor to consider the odds for themselves as to which path allows higher certainty and consistency over time.

Phelps goes on to suggest that the temptation to rely on spotting the best time to enter a position can result in missing the biggest buying opportunities.

“The more successful one is at market timing, the greater is the temptation to rely on it and thus miss much greater opportunities of buying right and holding on.”

In his study, he found that many stocks could have been bought at 52-week highs for many years and still turn out 100 to one winners. All one has to do is identify them and stick to them.

Long-term winners can be rare. Phelps questions why an investor would sell a long-term winner to put the money into a worse business. This point, perhaps counterintuitive to the idea of rebalancing a portfolio, is consistent with letting winners run.

Perhaps a greater challenge than identifying a great company is having the resolution to simply hold onto those investments. Many investors tend to set arbitrary objectives for when to exit, targeting to sell the position once they achieve some % return.

Phelps advises investors should “never if you can help it take an investment action for a non-investment reason.”

A few of the non-investment reasons he calls out include:

My stock is “too high”

I need the realized capital gain to offset realized capital losses for tax purposes.

My stock is not moving. Others are.

Phelps argues that, for long-term investors, any sale should be considered a confession of an error.

Closing

Phelps advocates for buying quality companies for a reasonable price and holding on for the long term. He identifies large addressable markets coupled with strong competitive advantages, or moats, as prerequisites for 100 baggers.

He suggests investors should “buy right and hold on.” Investors do, however, have the responsibility to stay up-to-date and monitor the company’s progress, tracking performance across various indicators including earnings and growth.

Phelps demonstrates that achieving 100-to-1 returns on an investment is attainable (although not necessarily easy!). The most important aspect of all in the equation is time. Perhaps the reason very few investors have not made 100-1 on an investment is that most investors haven’t tried.

Appendix

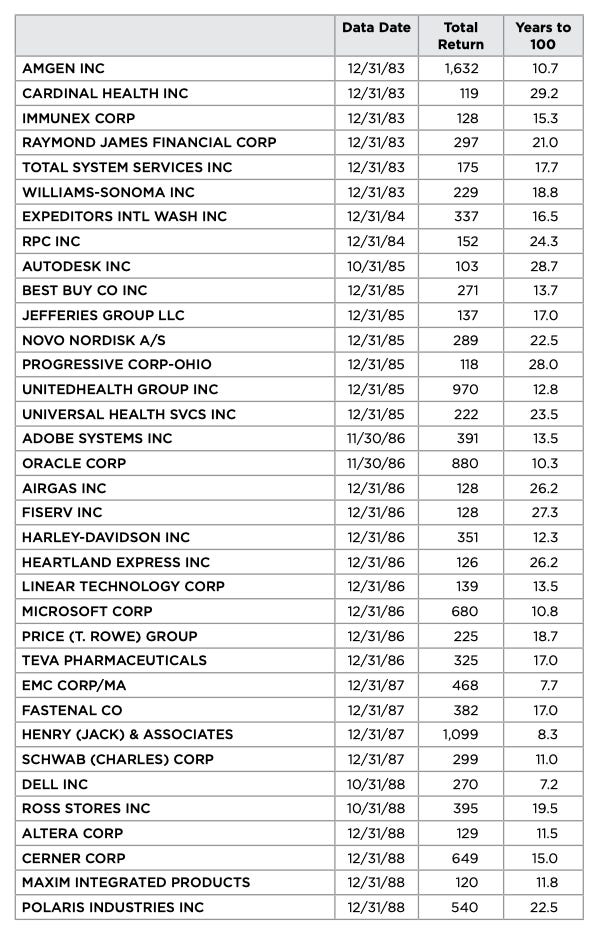

Inspired by Phelps’ work, Christopher Mayer published a follow up book, 100 Baggers: Stocks That Return 100-to-1 and How To Find Them, in 2015. He attributed the book to Phelps, drawing from and extending Phelps’ insights.

Mayer updated the study, identifying companies that have returned 100x starting from 1962 through 2014. A table of the more recent companies (starting since 1980) can be found below.