On Diversification and Concentration

Risk and volatility, diversification, concentration, target holdings in a portfolio, and sample portfolios from select investment managers

In his book The Aspirational Investor, Ashvin Chhabra shares results from a study conducted on the Forbes 400, a list of the richest people in America.

Breaking down the sources of wealth, the study found that 60% of the people on the list built their own business, 20% made it via finance, 12% inherited their wealth, and 8% accumulated wealth through real estate.

One particularly interesting observation is that nearly everyone on the list demonstrated usage of leverage and concentration.

This contradicts conventional wisdom found in many financial spheres. Vanguard has built a successful business and popularized passive index investing on the premise that investors should diversify their holdings.

It is important to note, however, that the same two factors that helped people make the list are the top two factors for people churning off the list.

Risk and volatility

Before diving into the core topics of diversification and concentration, it is important to clarify risk and volatility.

The more widely accepted perspective portrays risk as price volatility, also known as beta. This concept is embedded into many theoretical models, including the Capital Asset Pricing Model (CAPM) theory.

Depending on an investor's needs and behaviors, volatility in prices can be detrimental. High volatility securities are likely to be more affected by any market drawdown. If capital is expected to be available at any time, depending on the timing of any withdrawals, this could be very detrimental.

However, if investors are able to commit to investing for a longer period of time, short term price movement should become less risky.

Over the long term, value is fueled by business fundamentals. If the fundamentals are intact and growing, it should eventually be reflected in the price.

With this perspective, risk analysis is more concerned with the business itself including concerns such as product market fit, ability to execute, ability to innovate, valuation, enduring competitive advantages, amongst others.

Diversification

“Diversification is the only free lunch”

- Harry Markowitz, Nobel Prize laureate

Mainstream financial advice calls for diversification.

Conversationally, diversification is understood as spreading a portfolio across many investments. It is often understood to be the opposite of concentration.

Vanguard’s passive index funds are a pristine example of this concept. A small investment of a few hundred dollars can be distributed across hundreds of companies.

Diversification, however, is more nuanced than simply spreading investments out, and the concept is not limited to public market portfolios.

While diversification is the act of distributing risk across multiple investments, the core idea is for those multiple investments to be different, or more precisely uncorrelated. If one thing goes down, another thing goes up, reducing the price volatility of a given portfolio.

Diversification can be applied across many dimensions - geographical, asset classes, industries, investment styles (such as growth and value; low volatility and momentum), private and public investments, and much more.

Diversification does not call for a specific number of investments. The importance is the underlying countering forces.

Diversification seeks to limit excess exposure to any one factor.

Investors can leverage diversification to target specific areas of concentration, intentionally reducing exposure to any specific risk, such as any market-risk, asset-class risk, or company-specific risk.

Consider a business owner with the majority of their net worth tied to their private business in the commodities sector. The success of their business is likely highly correlated with public companies in the energy and commodity sectors. High-level opportunities to diversify may include real estate, given the inherent stability, or a portfolio of growth companies. While commodity businesses may benefit from increased inflation and interest rates, growth businesses are typically inversely correlated due to their long dated free cash flow.

Concentration

"Diversification is protection against ignorance. It makes little sense if you know what you are doing."

"A lot of great fortunes in the world have been made by owning a single wonderful business. If you understand the business, you don't need to own very many of them."

-Warren Buffet

Investors typically prefer to spread their investments out across multiple products such as ETFs, mutual funds, or sometimes individual stocks. Many investors have rules to ensure no single investment in their portfolio reaches a certain level of concentration. The idea of concentrated investments can be intimidating.

To truly understand an investor’s allocation and true concentration, one must zoom out for a holistic perspective.

People that own a business, have significant equity compensation, or own a home may be more concentrated than they may perceive. Depending on the relative size of these various assets, they may be highly concentrated in a particular area.

Consider a business owner with 80%+ of their net worth tied to their business. They will not typically stay up all night worrying about that fact. To the contrary, they express confidence and rest assured knowing they are in control of their wealth.

This same person may demand that their investment portfolio be significantly diversified, spreading the risk across hundreds of investments. The argument can be made that this person may be missing the forest for the trees.

One important difference between the business owner’s business and their equity holdings is the owner’s level of conviction.

Conviction is defined as a firmly held belief or opinion.

Having conviction in a particular allocation or investment helps investors stick through the difficult moments. Whether obstacles in managing a private business or the inevitable volatility in the public markets, these defining moments can make or break a successful investor. Investors that truly understand the businesses they are invested in will be more likely to endure these challenges.

Ideal number of holdings

What is an appropriate amount of holdings for a portfolio? It depends. While each investor will have their own objectives driving their needs, the following may provide some guidance.

Practically speaking, it is important to consider the size of the portfolio. The absolute portfolio size matters. Consider a professional earning $150,000 per year setting up a $500,000 portfolio from their savings. They might want to consider more robust diversification. What about a $50,000 portfolio?

Turning to academia, a study published in 1970, "Some Studies of Variability of Returns on Investments In Common Stocks", found that a portfolio of 32 stocks could yield 95% of the benefit of diversification. Extending the concept, any additional holdings beyond 32 would yield marginal benefits.

Benjamin Graham, the well known investor and mentor to Warren Buffet, stated that the target number is between 10 and 30.

Sample portfolios of select investment managers

As of December 2021, Berkshire Hathaway’s public equities portfolio manages $330.9 billion across 47 holdings. The top 10 holdings account for 89.54%. The top three holdings are Apple at 46.86%, Bank of America at 13.37%, and American Express at 7.38%.

As of December 2021, Tiger Global manages $45.94 billion across roughly 35 significant holdings (> 0.5%). The top 10 account for 47.44%. The top three holdings are JD at 8.20%, Microsoft at 6.21%, and Sea Limited at 5.55%.

As of December 2021, Valley Forge Capital manages $2.64 billion across 9 holdings. The top three holdings are S&P Global at 19.86%, Mastercard at 19.58%, and Moody’s at 15.18%.

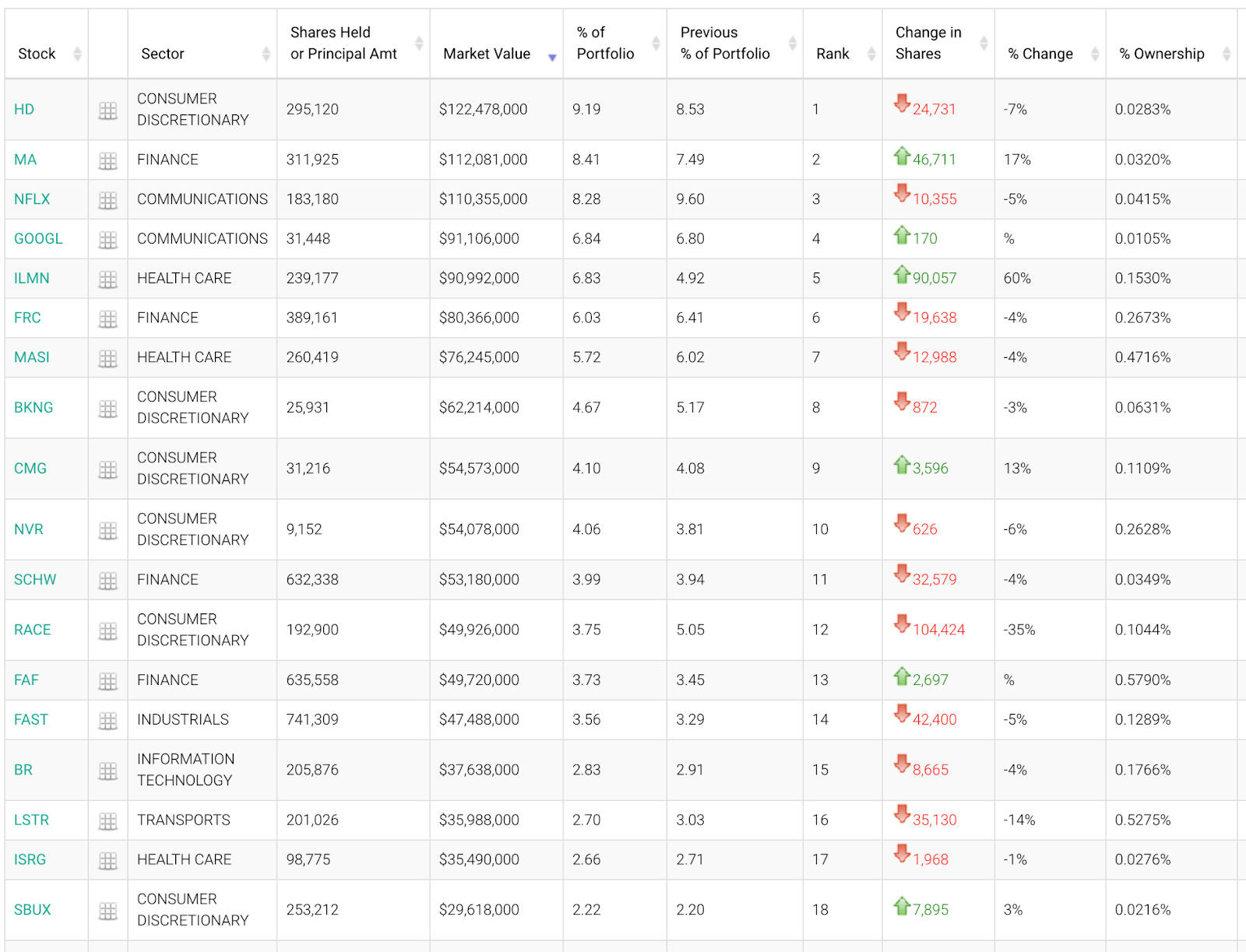

As of December 2021, Ensemble Capital manages $1.33 billion across 31 holdings. The top 10 holdings account for 64.15%. The top three holdings are Home Depot at 9.19%, Mastercard at 8.41%, and Netflix at 8.28%.

As of December 2021, Wedgewood Partners manages $735.3 million across 42 holdings. The top 10 account for 62.66%. The top three holdings are Apple at 8.66%, Meta at 7.60%, and Alphabet at 7.53%.

Closing

"Diversification may preserve wealth, but concentration builds wealth."

- Warren Buffett

Every investor should consider diversification as a key element of their investment strategy.

Generally speaking, diversification can be a good way to preserve wealth. Concentration is often a better way to build wealth.

A concentrated approach benefits from, and likely even requires, significant conviction. Borrowing ideas is easy. As shown above, many managers are required to disclose their holdings on a regular cadence. Taking on a similar level of conviction, however, requires work.

Diversification and concentration are not necessarily mutually exclusive when applied astutely.

There is no right or wrong approach. Each investor should consider their unique needs and objectives to determine the most appropriate path to accomplish their goals.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.