Q2 2022 Earnings Roundup 9.10.2022

Q2 2022 Earnings Roundup 9.10.2022

A brief review of the market, portfolio earnings scorecard, and a look into earnings from CRWD and OKTA

The market faced heavy resistance at the 200-day simple moving average (SMA), and coupled with the Fed’s firm positioning against inflation, has been on the decline. The market has given up roughly 8% since the local peak.

This week the market showed some resilience, bouncing back above the 50-day SMA.

This type of back and forth price action is normal in bear markets. Gaining ground is difficult.

The market had a healthy run higher, making a series of higher highs locally. After dropping to ~$390, it seems to have found a level of support. Will it hold, or will it revisit the June lows? It is impossible to know for sure. Bear markets tend to give glimpses of hope before dragging the market lower.

The consumer seems to be aware of this.

JP Morgan’s Guide to the Markets as of August 31, 2022.

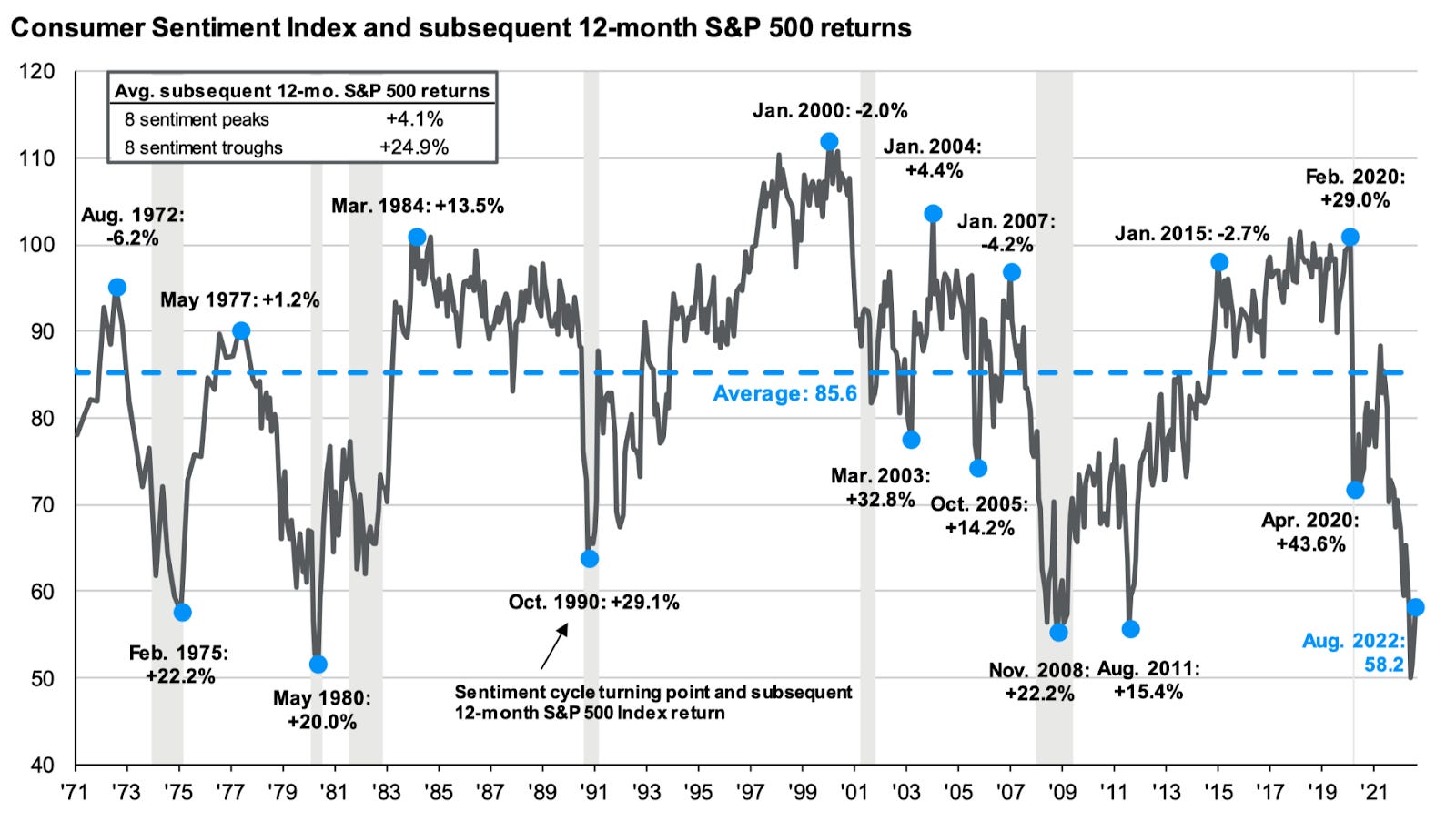

Consumer sentiment has recently hit an all-time low! Lower than in 2008, and rivaled by the low in 1980. As the graph points out, market returns over the subsequent 12-month period following a low point are quite strong, averaging around 25%!

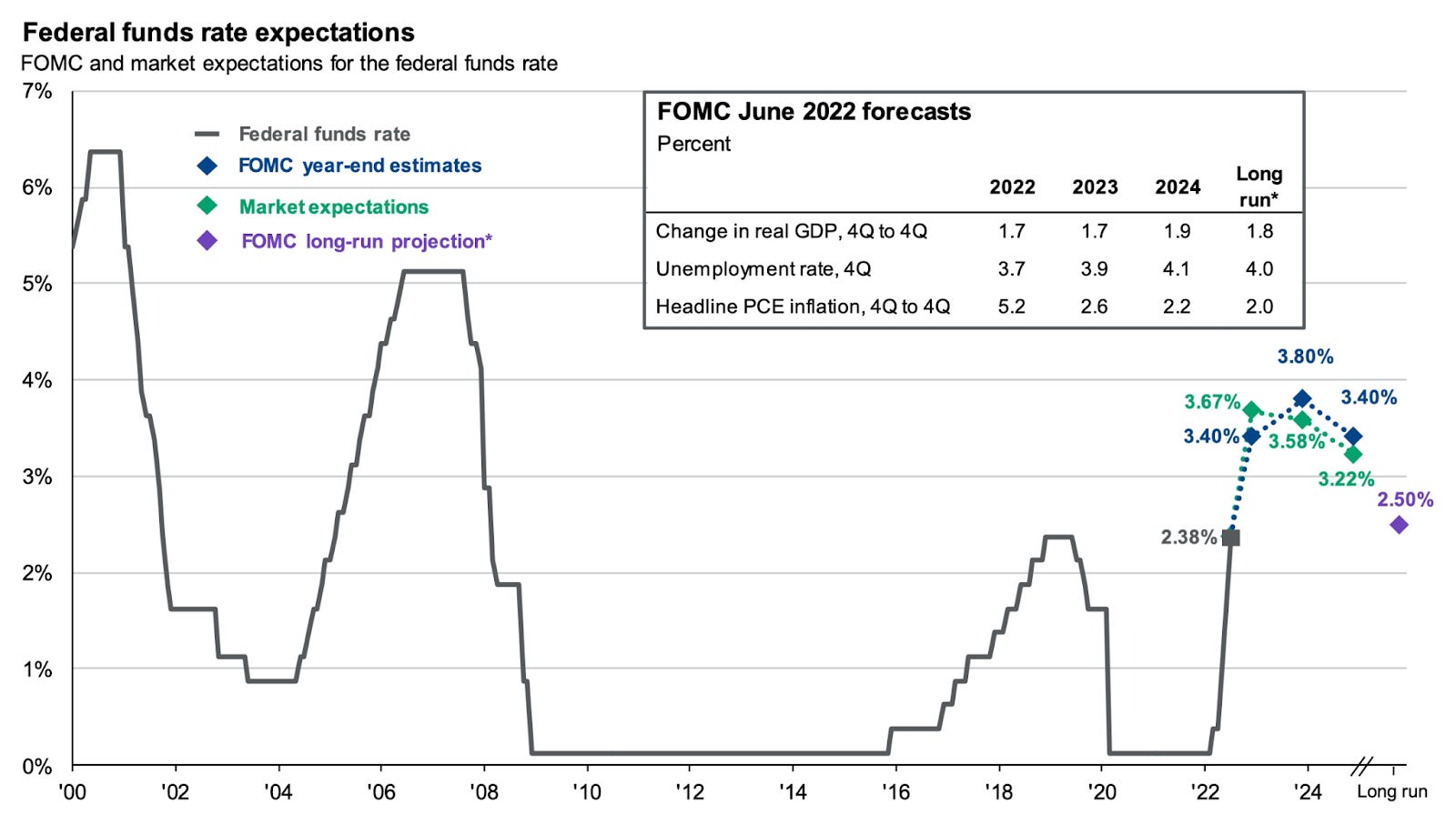

The Fed has a stronghold on the market — recent commentary has had a material impact on the market. The Fed pivot that some may have been expecting has not come, yet.

The market is currently pricing in a peak rate of 3.67%. The rate is then expected to decline throughout 2023.

JP Morgan’s Guide to the Markets as of August 31, 2022.

That being said, the Fed has made it clear that they are resolute in their fight against inflation. Whether inflation persists or comes down more quickly will determine their course of action.

Some components of inflation are transitory. From the graph below, notice how inflation due to vehicles has compressed over time. Energy is expected to be in a similar place.

The sticky components, such as shelter and wages, are the areas of concern.

The next inflation report is scheduled to be released on September 13th, 2022.

Q2 2022 Portfolio Earnings

Over the last two weeks, our last four portfolio companies reported earnings.

We’ll dive into the earnings from two of our cybersecurity companies: CrowdStrike and Okta.

CRWD

“We are on a mission to protect our customers from breaches”

- CrowdStrike

CrowdStrike is a global cybersecurity company that provides cloud-based services for protecting endpoints (i.e. laptops, phones, IoT devices, etc), cloud workloads (i.e. applications on servers), identity, and data.

CrowdStrike’s second quarter results are summarized below:

Total revenue of $535.2 million, an increase of 58% year over year

GAAP operating loss of $48.3 million, for a margin of -9%

Non-GAAP operating income of $87.3 million, for a margin of 16%

Free cash flow of $135.8 million, a margin of 25.4%

CrowdStrike has demonstrated consistent and persistent revenue growth, coupled with high and improving gross margins, and attractive profitability.

While GAAP measurements are negative primarily due to stock-based compensation, the company has demonstrated strong cash profitability as demonstrated by the improving Adjusted EBITDA and FCF margins over time. CrowdStrike has also been ultra-efficient, as demonstrated by the return on capital (ROC) ratios.

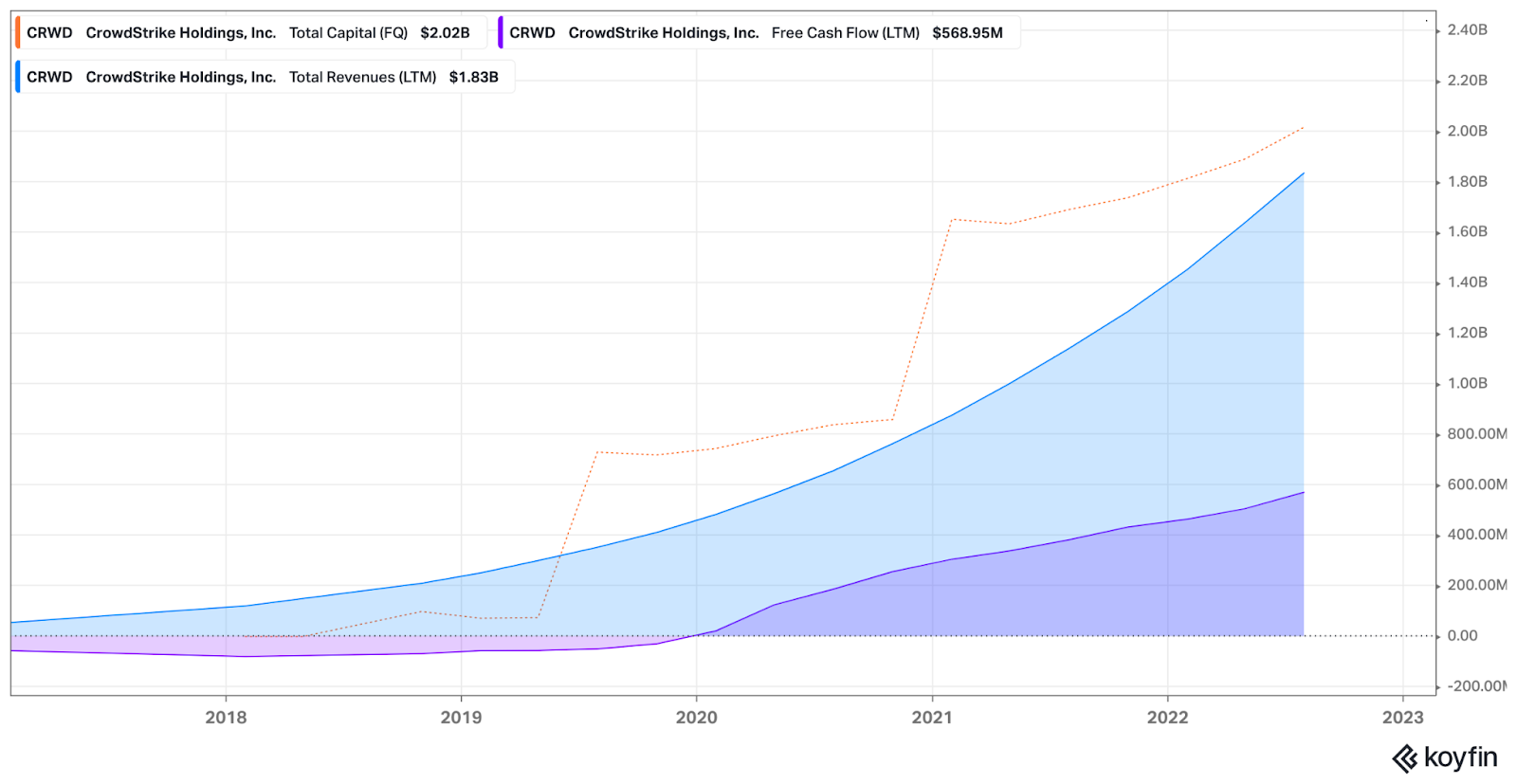

The following graph shows last-twelve month’s (LTM) revenue, last-twelve month’s (LTM) FCF, and the company’s total capital to better visualize the fundamentals and operating leverage.

Revenue and free cash flow are growing at an impressive pace.

Total capital includes all of the resources the company has required – whether those are funds that were raised from investors, debt they borrowed, shares used to pay employees with stock-based compensation, retained earnings, etc. Roughly ~$2 billion has been invested into CrowdStrike since inception, and the company is now producing just under $600 million in FCF every year.

Looking forward, CrowdStrike is guiding for revenue of $569-$576 million for Q3, representing quarter-over-quarter growth of 6-8%. While this may seem like deceleration, companies often guide conservatively particularly during difficult markets. CrowdStrike often exceeds estimates by 3-5%.

Highlights from the earnings call with founder and CEO George Kurtz:

“We achieved several additional milestones in the quarter. Ending ARR grew to $2.14 billion on a 59% year-over-year growth rate. We believe this makes us the second fastest software company reported to reach the $2 billion ARR milestone. Ending ARR for our emerging products grew to $219 million, up 129% year-over-year.”

“As Burt will discuss in a few minutes, we are raising our revenue guidance for the year and remain committed to delivering non-GAAP operating leverage and 30% or greater free cash flow margin for the year while investing in key initiatives that will further widen the gap between CrowdStrike and the competition.”

“Cybersecurity is not a discretionary line item. Cybersecurity is a priority for CIOs, CEOs and CFOs and Boards of Directors, and our value proposition resonates strongly with these stakeholders. Deals committed to close in the quarter did close in the quarter, and we entered Q3 with a record pipeline.”

“Our Identity Protection lineup achieved a record quarter and quickly grew to become the largest contributor to ARR within our emerging category. In Q2, the number of customers subscribing to our Identity Protection modules grew more than 100% quarter-over-quarter driven in part by a new logo attach rate that tripled, with close to 80% of cyber attacks leveraging identity-based tactics to compromise legitimate credentials and use techniques like lateral movement to quickly evade detection. Identity Protection is core to stopping breaches.”

“We see many parallels between this new market [Identity] and the early days of the EDR market, including a massive greenfield opportunity with an estimated $3.7 billion TAM in calendar year 2022 and a sizable uplift to ASP, which can be north of 30%. With our early and growing momentum, we believe CrowdStrike is well on the way to defining and leading the identity protection category.”

OKTA

The last point in CrowdStrike’s commentary makes a great segway to Okta.

Okta is the leading independent identity provider. Okta offers exactly what CrowdStrike is excited about growing into. Okta allows companies to have a central identity, or user account, for all of their employees. With this central access management, they can limit and control access, provisioning and de-provisioning as necessary. Only users that need access to [insert software application here] should have access. Okta also validates that the user logging in is the correct person, helping avoid impersonation or stolen credentials. Okta refers to this offering as workforce identity access management (“IAM”).

Okta recently acquired Auth0 to expand into customer identity access management (“CIAM”). This applies the same principles of identity to the consumers of your application. In simple terms, it allows developers to outsource the login functionality of their applications.

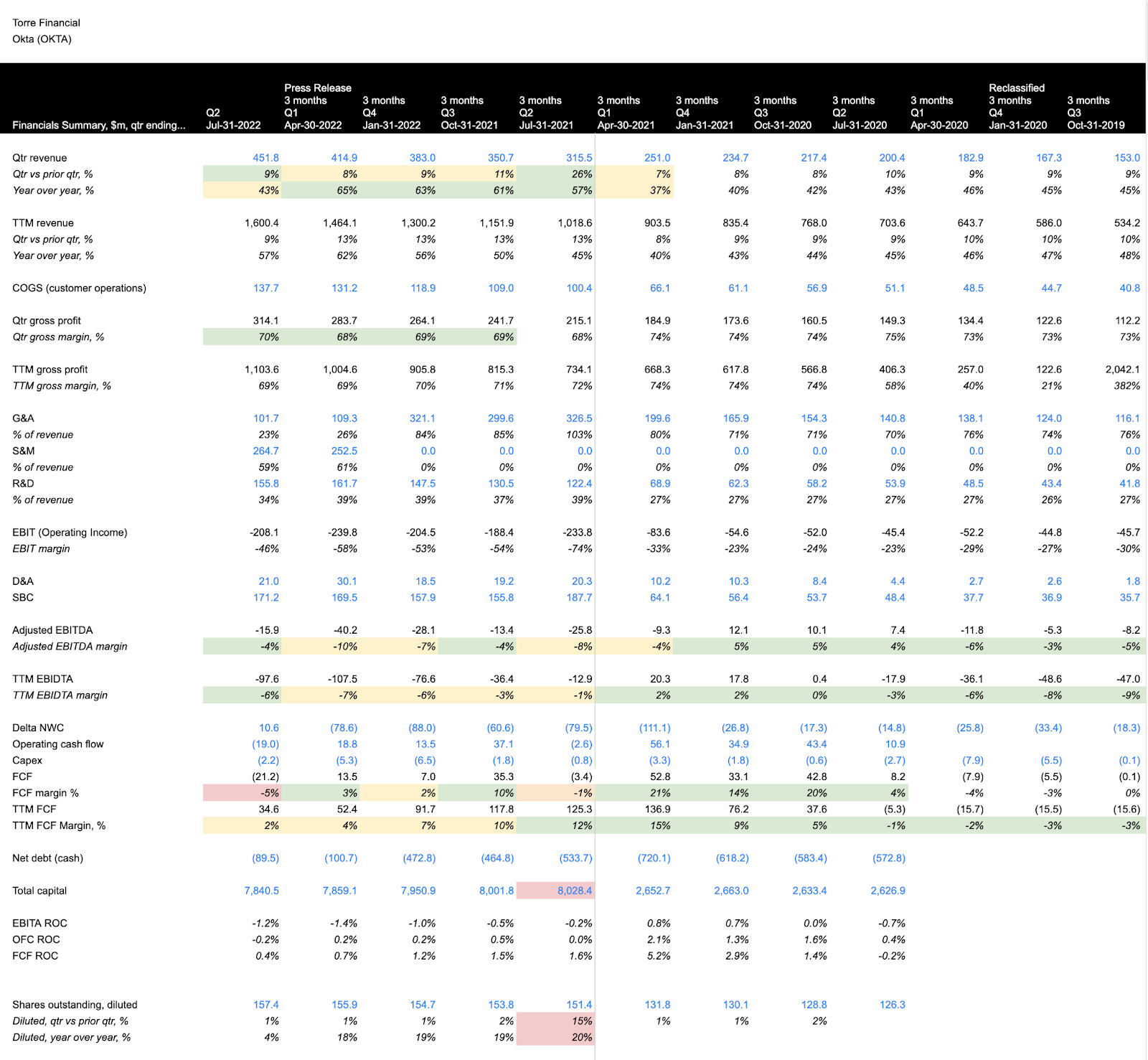

Okta’s second quarter results are summarized below:

Total revenue of $452 million, increase of 43% year-over-year

Growth accelerated quarter-over-quarter to 9% from 8% for the prior quarter

Gross margin increased to 70%, from 68% in the prior quarter

Adjusted EBITDA was -$16 million for a margin of -4%, which is an improvement vs the prior quarter’s -10%

Free cash flow margin was -5%, decreasing from the previous quarter

While operating in a promising market, all is not great at Okta.

There were some positive signals in the report. Revenue accelerated. Gross margins improved. Even guidance was strong. Okta is guiding for revenue of $463-$465 million for Q3, and raised guidance for the full year by $5 million.

Last year, growth may have been sufficient to please the market. This year, things have changed. The focus is now on profitability and efficiency, and Okta is lacking.

Up until the acquisition of Auth0 in Q1 2021, Okta had been demonstrating improvements from operating leverage. Margins were improving each quarter.

Since the acquisition, the story has changed. Operating leverage isn’t as clear.

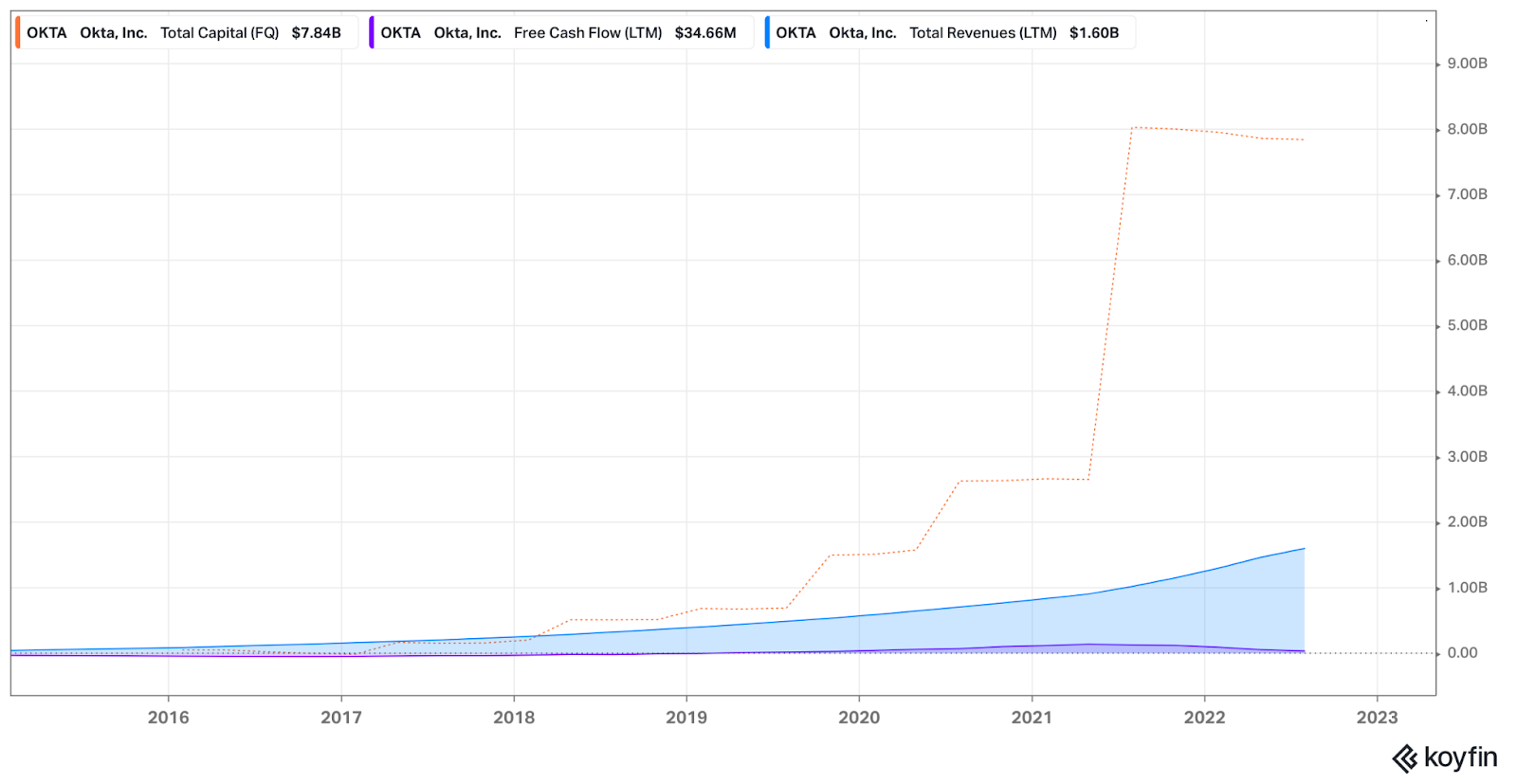

The following chart helps visualize Okta’s revenue, FCF, and total capital.

Total capital jumped significantly with the $6.5 billion acquisition of Auth0, to nearly $8 billion. Total capital is many multiples of revenue. FCF is now declining. (To be fair, Auth0 was paid for using equity in an all stock deal.)

While the idea of expanding into CIAM is appealing, Okta has had significant trouble integrating Auth0 into Okta.

Identity is the common thread across Auth0 and Okta. It may be the only common thread.

Okta’s primary offering is for the workforce. Auth0 primarily offers solutions for customer/user login.

Okta caters to enterprises and sells to CIOs, CISOs, and IT. Auth0 caters to software developers, CTOs, and CPOs.

Synergy in M&A comes from the power of the combined entities. Bringing new products into an existing distribution channel, or cross-selling, is often a significant value proposition. This, in fact, has been a significant point of tension in the integration, as Okta calls out in the earnings call.

Highlights from earnings call with founder and CEO Todd McKinnon:

“While the identity market opportunity remains healthy, our Q2 financial results were mixed. We produced better-than-expected profitability but our top line metrics were not where we wanted them to be due to challenges related to the integration of the Auth0 and Okta sales organizations as well as modest macro headwinds.”

“When talking about Auth0, it's important to revisit the strategic rationale of why we acquired Auth0. Individually, Okta and Auth0 were leading identity providers. Together, we offer the most comprehensive identity platform in the market that is unmatched competitively and creates powerful long-term network effects for us and for our customers. Organizations around the globe are looking for scalable and secure ways to digitally interact with our customers. Together with Auth0, we win the customer identity market faster and accelerate our vision of establishing Okta as a primary cloud.”

“Integrations are always difficult and touch every part of an organization. While we are making progress, we've experienced heightened attrition within the go-to-market organization as well as some confusion in the field, both of which have impacted our business momentum. In order to improve our performance going forward, we've implemented a number of action items. For starters, we're committed to stem nutrition within our go-to-market team. This is a top priority for me and my staff, and we're in lockstep on actions to take.”

“First, after 13-plus and tense years building Okta together, my Co-Founder, our partner, Freddy Kerrest, is going to be taking a much deserved 12-month operating sabbatical beginning November 1 to spend time with his family, recharge his batteries and think about what's next for Okta. Freddy will be staying close to the company as Executive Vice Chairman and Board member during his sabbatical.”

“For FY '23, we are raising our revenue outlook by approximately $5 million at the high end to $1.812 billion to $1.820 billion, representing growth of 39% to 40%. We are raising our profitability outlook by approximately $57 million.”

“Given our near-term outlook, coupled with the uncertainties of the evolving macro environment, we are reevaluating our FY '26 targets at this time. Having said that, we will continue to balance growth and profitability, and we look forward to updating you on our long-term outlook on the Q3 earnings call.”

Note the difference in tone compared with CrowdStrike.

While the integration has been challenging, the opportunity in identity is real. Okta is a leader. While I have trimmed Okta’s position size over the last few months, it is worth holding on to for now. I’ll be keeping a close eye on how things progress.

Closing

The market continues to be fixated on inflation and the Fed’s actions. These issues will remain in the spotlight until there is clarity.

Recession or not, cybersecurity remains a priority for companies. It is not a discretionary purchase. The risk of a breach far outweighs the costs of having protection in place. A breach can be catastrophic to a business.

Many of the businesses I highlight are doing well. That is why they are in the portfolio. This article highlights an exception. Okta demonstrated a solid financial profile with improving operating leverage prior to the acquisition. Post-acquisition, Okta+Auth0 is struggling to find its way.

Analyzing a variety of different businesses is critical and invaluable for building an intuition around investments. What is “good” or not is relative – it depends on the available option set. For deeper insights, compare Okta’s profile to various comparable peers such as Crowdstrike above, Snowflake, or Datadog.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.