The Payment Network Landscape

Visa, Mastercard, and PayPal; buy now, pay later, crypto and defi, pricing power, moats, tailwinds

Payment networks, with some of the most renowned and respected moats, have historically had a strong foothold in the market.

Visa and Mastercard have operated a near duopoly with their payment cards.

PayPal has gained similar respect as the king of e-commerce, with over a 50% market share of online payments.

Over the last decade, these companies have had strong returns historically, significantly outperforming the broader market. They have demonstrated quality performance with strong returns on invested capital and generally consistent revenue growth.

This year, however, they have lagged the broader market, exhibiting particular weakness since their peaks in late July.

Year-to-date, the S&P 500 is up roughly 27% while Visa, Mastercard, and PayPal are down 2.34%, 2.49%, and 18.59% respectively.

These businesses have enjoyed the fruits of the strong network effects they have been able to build and reinforce over time.

They are great, capital-light businesses with strong moats and continued growth opportunities ahead.

Yet, the market has been selling them off.

New entrants have been trying to breach the incumbent network moats, and there seems to be a shimmer of hope for some.

Buy now, pay later

The buy now, pay later (BNPL) payment model has gained traction over the last few years.

While not necessarily a new concept, a few companies including Affirm, Afterpay, and Klarna have been able to establish two-sided marketplaces.

BNPL is a short-term financing payment option, allowing purchases today to be paid in installments over time, often free of interest. It is a fast, convenient point-of-sale alternative to credit.

As BNPL players continue to grow their two-sided network, they could potentially displace incumbents.

Block, formerly known as Square, provides payment solutions for small businesses. They have built a mobile wallet, Cash, which has flourished throughout the pandemic. In August 2021, they announced the acquisition of Afterpay to further integrate their Seller and Cash ecosystems.

While these new networks have shown traction, the BNPL business model is a point of concern.

BNPL typically focuses on large ticket items, which from the get-go reduces the universe of potential transactions.

The BNPL model charges both the merchant and consumers. Merchants pay a fee for each sale, while consumers pay interest and other fees.

The models that have shown success have leaned heavily in favor of consumers, offering transparency, interest-free installments and even no late fees.

Interest-free installments are often a promotional offering, paid for by the merchant through a higher transaction fee in exchange for driving conversion and sales in the short-term.

Although some prominent companies have been built around BNPL, at its essence, it is a feature, one that PayPal was able to roll out as a payment option to its vast network of merchants.

Additionally, many BNPL services rely on Visa and Mastercard to pay off the installments. Others, such as Affirm, are partnering with Visa and Mastercard to extend their BNPL services to everyday purchases.

Given the higher merchant costs and ample competition, it may be a challenge for BNPL players to achieve both scale and profitability. Profitability is ultimately required for a sustainable model.

Crypto and decentralized finance

Crypto currencies and decentralized finance (DeFi) are similarly garnering a lot of attention as new payment options.

Although very early in the space, they offer a compelling narrative: the promise of a decentralized network, one that is not owned by any single entity.

While speculative, it has the potential to pose a serious risk to payment networks in the future.

Visa, Mastercard, and PayPal seem to acknowledge the potential as they are investing heavily in the space directly, through acquisitions, and through venture investments in crypto start ups.

Pricing power and pressure

Because they offer a critical service, the established payment networks have relatively strong pricing power.

PayPal, Visa, and Mastercard all had plans to increase fees for online transactions in 2021.

PayPal moved forward with the price increases in August 2021.

Visa and Mastercard ultimately postponed their changes to April 2022.

Merchants have often expressed concerns over the dominance of payment networks. As merchants increasingly adopt credit card and debit card payments, the fees they pay on each transaction continue to add up.

These concerns have received increased attention.

In March 2021, the Department of Justice began an antitrust investigation into Visa, probing for anticompetitive practices in the debit-card market.

In November 2021, Amazon said it would stop accepting Visa credit cards issued in the U.K. due to higher interchange fees.

This is not the first time payment networks have dealt with similar negotiation tactics. In April 2020, Kroger stopped accepting Visa credit cards in certain stores. This was reversed 6 months later, presumably as the two parties settled on pricing.

Entrenched moats

While there are ongoing concerns related to potential disruptors and pricing pressure, the payment networks have been able to carve out a very strong moat for themselves and have strong tailwinds as the economy emerges from the pandemic.

The payment network moats are deeply entrenched in part due to the unique balancing act of all stakeholders.

To start, the fees that the payment networks charge are split amongst many parties - payment network, acquiring bank, and issuing bank.

This leads to a supportive environment, where the banks are incentivized to grow the network by issuing cards as well as signing up new merchants.

Stemming from the competition to issue cards and attract consumers, payment networks and bank partners have successfully established robust reward programs.

By effectively giving consumers cash back from their transactions, they have driven consumers to prefer to pay with their credit cards, making them another key player in reinforcing the network.

These types of dynamics are difficult to displace. More than a technological challenge, these networks are driven by a scaled incentive system that has now led to ingrained behavior across all stakeholder groups.

Tailwinds

Macroeconomic factors are lining up to be favorable for payment networks.

Payment networks stand to benefit from inflation due to higher transaction values. Because these networks charge as percentages of the transaction value, any increasing prices will naturally flow through to the payment network.

Relatedly, their asset-light business model is ideal for an inflationary environment. Asset-light businesses benefit from the lack of capital expenses, while asset-heavy businesses will face increased costs to maintain their operations.

As the global economy continues to reopen, travel will pick back up. Travel spending, a large category, has been depressed since the pandemic. Additionally, cross-border transactions are an important high-margin business for payment networks.

New behaviors are likely to stick. Throughout the pandemic, consumers have increasingly adopted online shopping, credit cards, and other digital solutions such as QR codes. These trends are likely to continue to drive growth.

Conclusion

While Visa, Mastercard, and PayPal have benefited from strong network effects, formidable disruptors seem to be emerging from the BNPL space and potentially from DeFi in the future.

Payment networks have been able to create a uniquely balanced ecosystem where all parties are incentivized. They offer value-added services beyond transactions, including financing options, rewards programs, currency conversions, fraud prevention, and insurance.

It remains to be seen if BNPL is sufficient to be a viable competitor to existing payment networks or a niche offering. The dynamic for DeFi is even less clear.

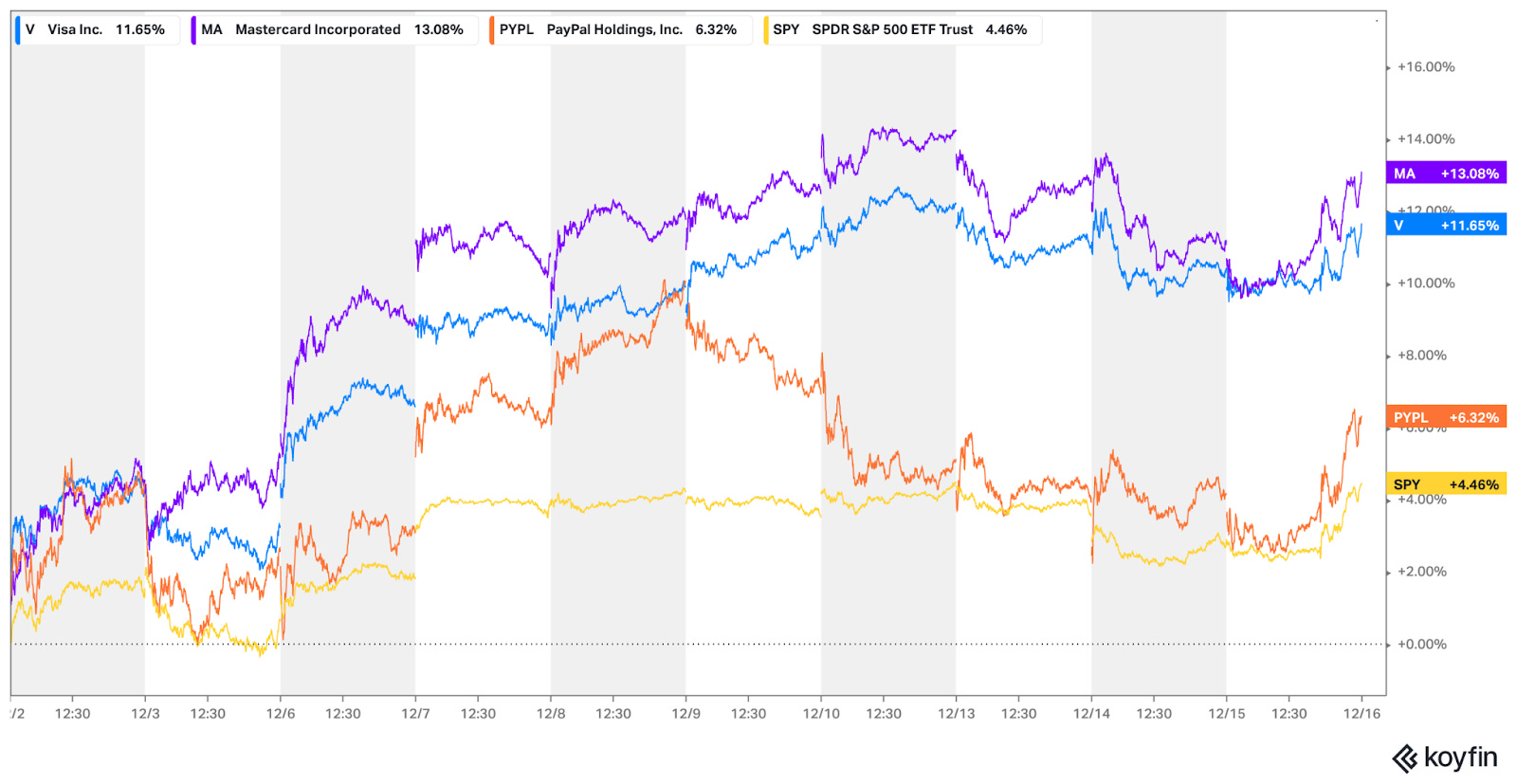

In the last few weeks, the Visa, Mastercard, and PayPal have started showing some momentum relative to the broader market. They may be turning around.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.