Understanding Growth and Value

Historical studies, recent trends, and underlying factors

Growth versus value can be a polarizing topic, with many investors identifying strongly with one over the other.

More than simply different investment styles, these strongly-held beliefs are often seen as mutually-exclusive.

Each investor sees the world through their own lens. Investor actions are ultimately driven by their beliefs. By understanding both sides of the coin, investors will be better equipped to understand the market and ensuing trends.

Historically, Value Wins

Value stocks generally have a low price relative to some fundamental measure, for example:

Low price-to-earnings ratios

Low price-to-cash flow ratios

Low price-to-book ratios

Value stocks tend to be more mature businesses, having proven their ability to generate profit on a proven business model. They tend to have higher dividend yields.

Well-known investors associated with value investing include Warren Buffet, Benjamin Graham, David Dodd, Charlie Munger, and Seth Klarman.

Benjamin Graham, author of The Intelligent Investor and Warren Buffet’s mentor, popularized “cigar butt investing,” an extreme version of value investing wherein investors seek out deep value businesses trading at prices below their liquidation value.

Many academic studies show value investing as a strategy that can beat the market in the long term.

One study, conducted over a 27-year period, shows that the three cheapest decile cohorts had annual returns of 17-20% compared to 10-11% returns of the three highest decile groups.

Another study shows the outperformance of value stocks on an annual basis, over a 21-year period. Growth only outperformed in 3 years.

Source: Lakonishok, Shleifer, and Vishny (1994)

One rational explanation for value’s outperformance may be investors’ overreaction to distress factors. Such situations may be difficult for investors to wrangle behaviorally, leading them to sell companies beyond the rational point. As the price falls and creates value opportunities, the future expected returns of an investment rise, leading to a scenario with a positively-skewed risk-reward.

Recently, Growth Wins

Growth is generally considered more expensive and riskier. Stock prices are high relative to their sales or profits, due to expectations from investors of higher sales or profits in the future. They're expensive because of big expectations. If growth plans don't materialize, the price could plummet.

While the two studies above demonstrate value’s outperformance, they both covered a common time period, namely the 60s, 70s, and 80s.

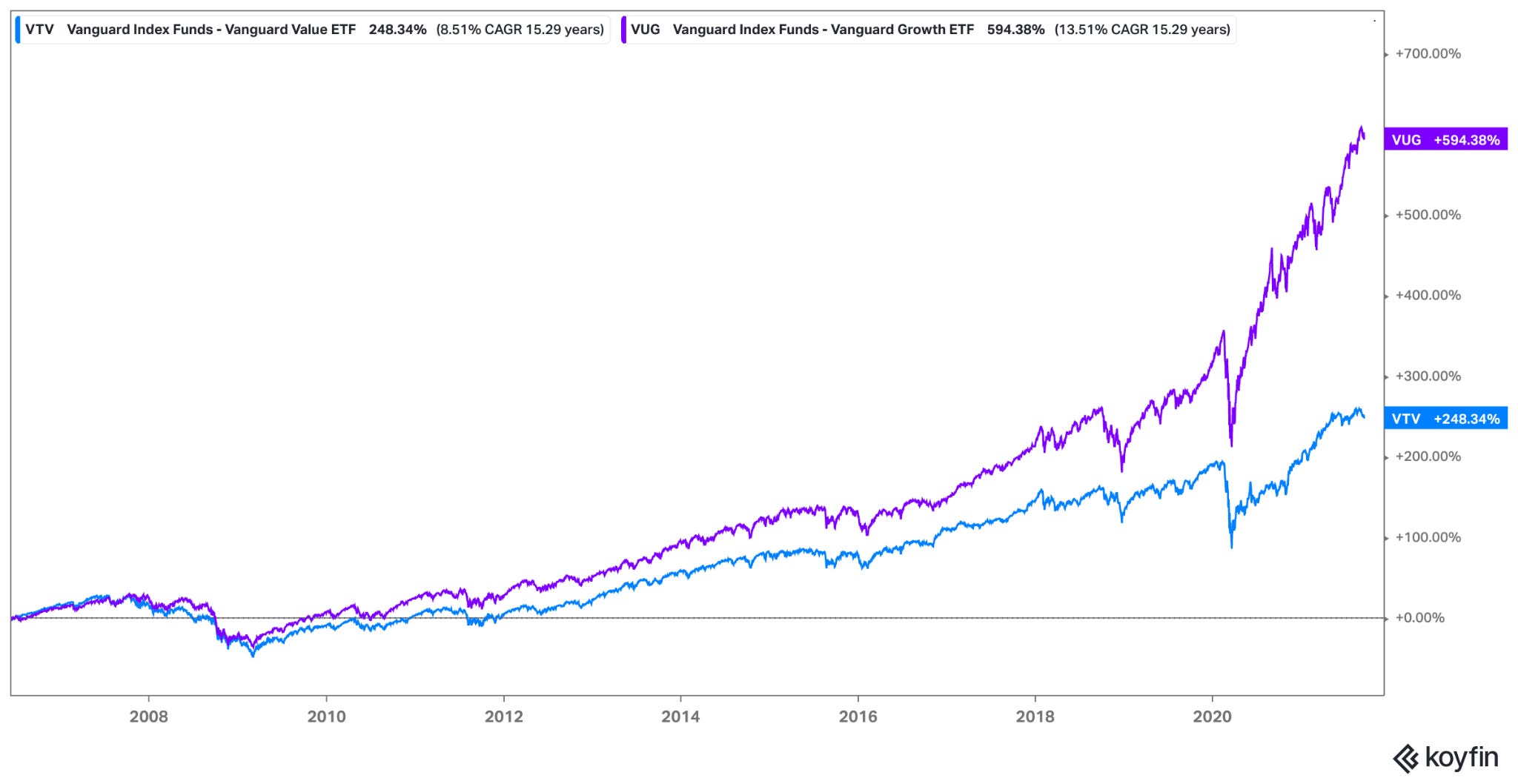

More recently growth has greatly exceeded value in terms of performance. Over the last 15 years, growth has generated returns of nearly 600%, compared to value’s nearly 250%.

Source: Koyfin

Vanguard’s Value ETF, VTV, and Vanguard’s Growth ETF, VUG, ETFs are often used as the benchmark for value and growth.

Vanguard’s funds mimic the large cap indices set by the Center for Research in Security Prices (CRSP).

“CRSP classifies value securities using the following factors: book to price, forward earnings to price, historic earnings to price, dividend-to-price ratio and sales-to-price ratio.”

“CRSP classifies growth securities using the following factors: future long-term growth in earnings per share (EPS), future short-term growth in EPS, 3-year historical growth in EPS, 3-year historical growth in sales per share, current investment-to-assets ratio, and return on assets.”

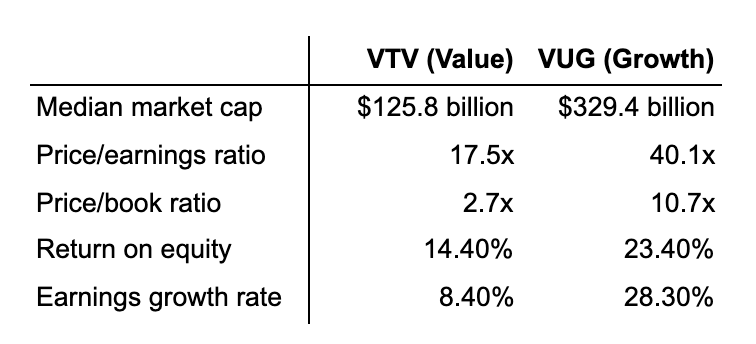

Comparing the fundamentals of the two ETFs shows growth companies having higher multiples on historical fundamentals.

Source: Vanguard VTV and VUG, as of 8/31/2021

While the labels of growth and value seem like a reasonable division, they do not tell the whole story.

Underlying Factors

The bifurcation of growth and value is less about the true intrinsic value of a company and more about the means by which companies are classified.

Naturally, accounting measures look different for different businesses.

Particular industries such as financials and energy tend to have elevated book values due to the capital intensive nature of their business. In general, companies that require and have more assets will have a relatively higher book value, resulting in a lower price-to-book ratio. As an example, Bank of America and Chevron have a price-to-book ratio of roughly 1.3x and 1.4x, respectively.

On the other hand, many technology companies are asset-light businesses. Because book value is relatively low, the price-to-book ratio will come in very high. Amazon, Facebook, and Google have a price-to-book ratio of 15.3x, 7.5x, 7.9x respectively.

This is clearly reflected in the composition of the indices. Looking at the sector diversification for VTV and VUG…

Energy accounts for roughly 5% in value, but less than 0.5% in growth.

Financials account for roughly 22% in value, but roughly 2% in growth.

Technology accounts for roughly 6% in value, but nearly 50% in growth.

Banks have not done very well since the financial crisis, given the lingering negative sentiment coupled with the extremely low interest rate environment.

The price of oil peaked in 2008 and has struggled to recover.

On the other hand, technology has flourished.

The value and growth indexes may simply be reflecting the changes happening in various sectors of the economy.

Closing

There is no right or wrong answer as to whether an investor should be a growth investor or a value investor. In fact, those need not be mutually exclusive.

Labels can be misleading, as they tend to be overly simplistic and often do not tell the whole story.

In a sense, all investors are value investors. Everyone is looking to invest today for a gain. Value is difficult to encompass in a single metric or ratio. It can better be understood by a company’s intrinsic value. There can be opportunities of significant value in a “value” company as well as in a “growth” company.

Rather than taking labels as strongly-held beliefs, investors would be better off seeking to understand the underlying components.

All investors have different objectives, risk profile, and time horizons. By understanding the underlying characteristics and factors, investors will be better positioned to build the portfolio that best suits them.

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.