Market, Earnings, and CRWD - September 2, 2023

Market commentary, portfolio company earnings results, and closer look into CrowdStrike

Every two weeks we share market and earnings reviews, as well as a deep dive into one portfolio company. Subscribe now to follow along.

Market

The market bounced back after approaching the 430 level discussed in the previous post. These last two weeks have instilled renewed hopes of the bull market’s continuance.

The market is trading above both its 200-day and 50-day simple moving averages, a positive momentum indicator. The next critical move will be retesting the 460 level – if able to break above it, the market could continue to new highs.

The recent price movement comes as a surprise to many investors, as high yields continue to present an attractive alternative.

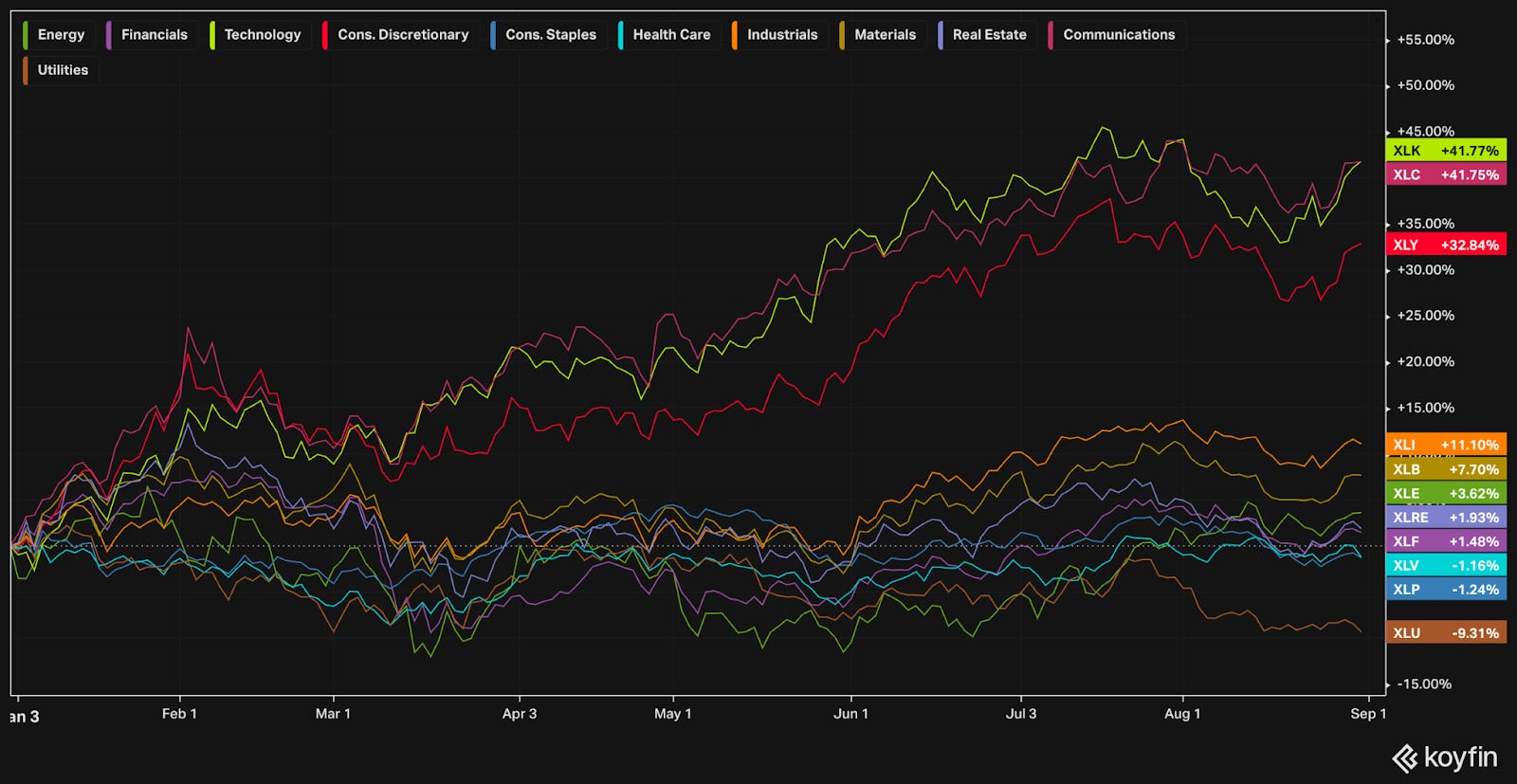

Year-to-date performance across indices:

Nasdaq +41.6%

S&P 500 +17.6%

Dow Jones +5.1%

Sector leaders and laggards

Utilities is the lone outlier, with -9% YTD. Utilities, being highly regulated, are typically seen as a fixed income alternative. They provide steady dividend payouts. They are particularly affected by the high yields.

Gains are driven primarily by

Technology +42%

Communications +42%

Consumer Discretionary 33%

These three sectors include many of the mega caps and AI players.

The intrinsic value of a company is the discounted future cash flows it produces. With high yields, future cash flows are worth less. Technology and high growth companies bake in a lot of growth out into the future – they are “long duration” equities.

Notwithstanding the headwinds faced by high yields, they have pushed forward in part due to the resilient economy and optimism about the future.

IPO market warming up

IPOs have been outperforming the S&P 500 this year, by a significant margin (11%).

This seems to be helping warm up the IPO markets.

Instacart, Klaviyo, and Arm are all planning to go public in September.

Jobs – bad news is good news

Markets can be fickle and erratic. Sometimes good news is good, and markets go up. Sometimes good news is bad, and markets go down. It can depend on the second- and third-order effects of the news.

The Jobs Report released on Friday September 1st, 2023, showed the unemployment rate ticked up to 3.8% vs the 3.5.% prior.

The market cheered the result. These data points give the Fed more reasons to not pursue further hikes. The market is currently more concerned about additional tightening than it is about the state of the economy.

CRE debt maturity

In our post Market & Macro - April 1st, 2023, we highlighted a potential concern in the real estate space:

“There is ongoing concern about real estate & real estate loans. It is a large industry, with significant lending requirements in which many large and regional banks participate. Rising rates affect the value of those loans and also the operator’s ability to pay them. If the loans are fixed rate, the valuation of the loan is significantly impacted. If the loans are at a floating rate, tenants will have a very difficult time paying the hiked rates as the Fed rate went from 0% to 5%.”

The next 12 months will be critical, with about $1 trillion in loans maturing.

While banks and lenders can be accommodative, renewing or extending loans, there are significant challenges ahead. Refinancing at a significantly higher rate can be prohibitive and/or unsustainable for ongoing operations.

Further, if valuations come down and violate the covenants set in the loans, they may become distressed assets. This would further perpetuate the cycle.

So far, real estate equity holders have mostly benefited from “unchanged” valuations due to the market being in a standstill. If there are no transactions, there are no comparables by which to reprice an asset.

That is starting to change. Buildings are going for fire sale prices. Some recent transactions in San Francisco:

In August, 60 Spear St sold for $40.9m, 66% less than the most recently assessed property value of $121 million

In June, 550 California St sold for ~$44m, less than half of the purchase price in 2005

In May, 350 California St sold for ~$65m, less than 75% of the estimated value of $300m

Q2 2023 Earnings

Over the last two weeks, 6 portfolio companies reported earnings.

Results were positive across the board. All six companies beat against revenue and adj. EBITDA expectations.

Recently, the market has demanded more profitability, preferring lower duration equities. Many technology companies are flexing their ability to balance growth and profitability, demonstrated by significant improvements in margins.

CrowdStrike (CRWD)

Originally covered in July 2020 – CrowdStrike (CRWD); Most recently covered in March 2023 – Market & Earnings Review - March 18, 2023

Founded in 2011, CrowdStrike has emerged as a distinguished leader for next-generation cybersecurity solutions.

Led by co-founder and CEO George Kurtz, CrowdStrike has become the clear leader in the cybersecurity space.

The company was ahead of the time. Even before Covid, they were operating effectively with 50% of the workforce remote. Since their founding, they have been keenly focused on applying AI to security.

CrowdStrike’s lead offering is endpoint security. For simplistic purposes, consider this as the next-generation of anti-virus software (i.e. McAfee or AVG).

Legacy solutions required observing an attack, storing the attack in a master database, and then downloading that database to each endpoint (i.e. computer).

CrowdStrike’s cloud-native solution uses a lightweight agent to monitor traffic and unusual behavior. They have a centralized place they call the “threat graph” that processes all of these signals. Leveraging AI, they are able to stop attacks more effectively – both known attacks as well as those not previously known.

They provide endpoint security not only to computers, but to workloads (applications) in the cloud or any device connected to the internet (internet of things).

The company has since evolved into a platform, offering more than 20 modules including device management, data protection, malware detection, identity protection, logging, response services, and much more. Many of these have come from internal innovation as well as through bolt on acquisitions.

Their market is expected to grow at 13% per year.

They compete with Microsoft’s security offerings, Palo Alto Network, Fortinet, Blackberry and SentinelOne to name a few.

SentinelOne is the younger, fast growing upstart. Once seen as a very viable threat, SentinelOne has suffered significant leadership attrition. They have continued burning through cash, even as the market shifted. Most recently, there have been rumors that Blackberry and SentinelOne are both looking for buyers. If they were to be bought out by private equity firms, that would certainly be beneficial to CrowdStrike.

With growth in the high 30s, CrowdStrike continues to gain market share in an attractive market with secular growth.

Turning to the financials:

Revenue growth has been decelerating, yet more resilient than other companies. With Q2 revenue growth of 6% and guidance of 6% for Q3, there’s the possibility of an inflection point. If Q3 comes in above, it may mark an end to the deceleration.

TTM revenue growth of 44% is very impressive, especially for this environment.

Gross profit margins are holding steady at 74%. This is very good to see. SentinelOne was known to compete on price. This type of competition can lead to certain behaviors such as discounting that can erode profitability. Maintaining a steady margin shows CrowdStrike’s pricing power & ability to service their customers efficiently.

Adjusted EBITDA margins ticked up to 20% in Q2.

FCF margins of 32% are significantly higher than their EBITDA margins, demonstrating effectiveness in cash conversion. One of the key differences between EBITDA and FCF is working capital. Many SaaS companies charge customers upfront for access. They receive the cash in advance of delivering the service – cash flow is up before the earnings appear.

The balance sheet is very strong. They have over $3b in cash and debt has been maintained at $740m.

Shares outstanding are growing 2.3% per year, due to dilution primarily for stock based compensation. It is good to see this come down from the 4-5% annual rate a few years ago. It would be nice to see the dilution rate continue to go down, ideally under 2%. That being said, 2% dilution for 40% growth and high profitability is not the worst tradeoff.

Return on capital ratios are very strong at 20% EBITDA ROC and 32% FCF ROC. These have been trending higher the last few years. They are able to leverage their platform as they continue to grow. This is a well run, efficient business.

CrowdStrike share price appears to have stabilized after the rollercoaster of 2021 and 2022. Since January 2023, shares have been building momentum. In June, the 50-day moving average crossed above the 200-day moving average, an indication known as the “golden cross.” Shares are currently trading above the 50-day moving average, which is also positive.

Turning to the valuation:

CRWD trades at 9.8x EV/NTM revenue. While not cheap, this is moderate given the high level of performance. The highest valued growth companies go for 15-17x.

EV/NTM EBITDA of 41.3x is similarly at a premium, yet deserving.

The TTM FCF yield of 2.5% is better than peers. For context, the SPY has a TTM FCF yield of 3.3%.

The following table shows potential annualized returns over the next 5 years given a spectrum of revenue multiples and growth rates. This model includes annual share dilution of 2.5%.

Assuming they are able to maintain a multiple of 10x EV/NTM revenue and growth decelerates to between 15-25% per year, investors could reasonably expect between 11-21% annualized returns over the next five years.

Any additional improvement – be it multiple expansion or higher growth, would enhance the return. The company is currently growing at ~40% and is showing signs of growth stabilizing.

Closing thoughts

The market continues to climb the wall of worry. While momentum may carry the market higher, investors are best served by scrutinizing their holdings. High yields are an attractive alternative – and markets are really good about plugging any dislocations.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We look at the first fundamentals, yet continually re-evaluate and rebalance positions according to what the market is offering.

We’ve invested in CrowdStrike since the summer of 2019 when they IPO’d. It has been a great investment thus far. We’re excited about their continued execution, growth, and optionality. While there were worries of competition eroding profitability, CrowdStrike has been able to defend itself due to their differentiated offering. CrowdStrike is an excellent example of an emerging company with many traits of a long-term compounder. They are executing on all cylinders and have a long runway ahead.

Over the next two weeks we will hear earnings from Zscaler and Adobe.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.