2021 Q4 and Year-End Review

Review of the quarter including results, market commentary, portfolio commentary, and insights.

Results

The fourth quarter of 2021 ended on December 31st, 2021.

The consolidated return for Torre Financial accounts was -3.03% for the fourth quarter and 30.69% full year.

The S&P 500 (SPY) returned 11.07% and 28.75%.

The Dow Jones Industrial Average (DIA) returned 7.85% and 20.84%.

Returns for individual accounts may vary as each account is managed separately and tailored towards each client’s investment objectives and risk profiles.

Market

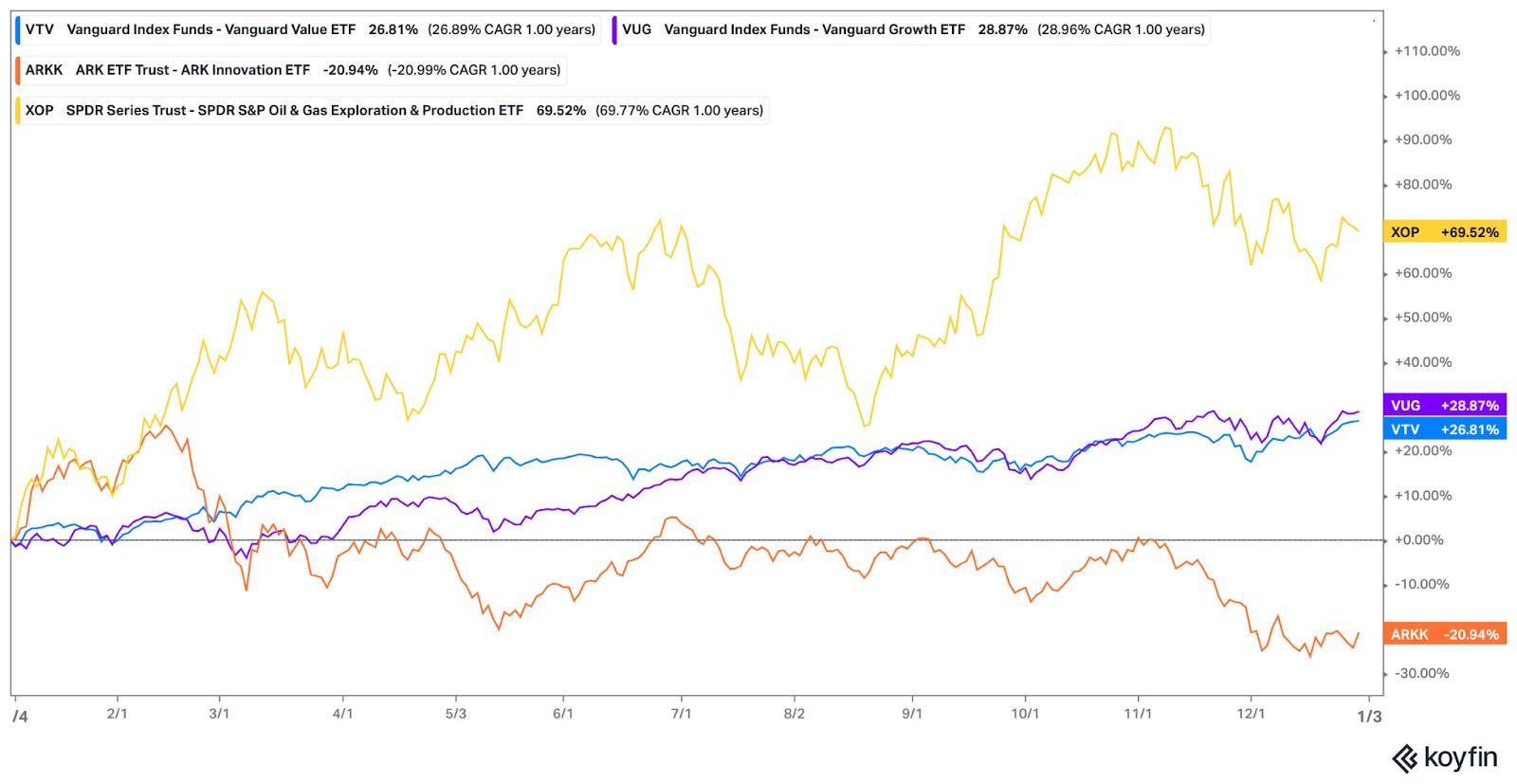

The market continued the march to new highs.

After underperforming early in the year, growth was able to catch up to value, with both ending the year with similar performance.

While these high level views give the semblance of a smooth year, under the surface there was plenty of rotation across sectors.

Energy, oil, and commodities outperformed.

High-growth companies, whose valuation hinges on long-dated future cash flows, underperformed.

Today, many names are in correction territory, trading more than 20% below their highs.

These changes came as investors digested and reacted to new information.

COVID continues to evolve, with the latest Omicron variant replacing Delta. Steep increases in infection rates are concerning. The milder symptoms and lower-risk of hospitalization are a silver-lining.

Global supply chains, shocked when the pandemic began, continue to struggle. Shortages have yet to be resolved.

For the year ending in November 2021, the consumer price index showed prices had increased 6.8%.

Inflation is now outpacing wage growth, which came in at 4.3% for the same period.

While some still believe that inflation should settle as supply chains normalize, Jerome Powell commented that inflation should no longer be considered transitory. The Fed is planning on three rate hikes in 2022.

The White House continues to push for a $2 trillion bill, Build Back Better. Faced with resistance, it is unclear if the bill will pass. The additional spending would put upwards pressure on inflation.

Notwithstanding the myriad of concerns, the primary trend remains in place. The market continues to push forward, climbing the wall of worry and notching new highs.

Portfolio

Top performers in Q4

Bottom performers in Q4

Commentary

ANET. Arista Networks builds and sells servers for data centers, i.e. the servers that run “the cloud.” Their primary customers include the tech titans Facebook and Microsoft. In the last earnings announcements, some of Arista’s customers guided towards increased capital expenditures for next year. Arista confirmed the positive trend in their own call. Arista has fared well so far and will likely continue to. However, Arista’s business model is naturally cyclical as it depends on capital expenditures.

UNH. UnitedHealth Group’s largest risk is significant change to healthcare insurance. UNH is likely benefitting from the resistance the White House is facing. Additionally, UNH benefits from delayed operations due to Omicron – they continue to charge their premiums monthly regardless of activity.

DDOG. Datadog provides software for companies to monitor and observe their own software systems. It is a critical function for smooth operations, as it helps developer and ops teams prevent and mitigate issues. They are benefitting significantly from the push towards digital transformation. Datadog is not a transitory play - once it is implemented it is difficult for teams to migrate off of their platform. Datadog has performed admirably, especially considering the significant sell off in many high growth peers.

UPST. With a fantastic first three quarters, Upstart shares peaked at a high of $400 and have since corrected. Regardless, Upstart continues to be a high conviction pick due to their large addressable market, superior offering, strong management team, and strong financial fundamentals. For additional details, see Upstart (UPST) - December 2021.

PYPL. PayPal, a leading digital payment processor, has experienced a significant tailwind from COVID and trends towards digitalization. Given their strong network of merchants and consumers, coupled with many promising opportunities ahead, I find PayPal to be a particularly attractive established compounder. Additionally, PayPal’s business model benefits from any increases in inflation, counteracting the impact interest rates may have on our other high growth companies. PayPal has likely suffered from tax-loss harvesting as the year winds down. I expect this to turn around next year.

PLTR. Palantir provides critical software for mapping and optimizing large operations. Their clients include many government agencies including the FBI and CIA. They have recently expanded into the commercial sector and have demonstrated market fit with large enterprises and small start ups alike. Palantir’s software serves as a competitive advantage for their customers, allowing them to leverage big data and analytics to make better decisions. Their business model is inherently long-term focused. New customers come at high costs with very involved implementations. However, once onboarded, customers tend to stay and grow their usage of Palantir’s software. These long-term relationships become very high margin contributors. The unique economics of their business model do require long-term commitments. The solutions they deploy are clearly providing significant value. The jury is still out on how profitable a business they can build.

Insights & Analysis

“We worry top-down, but we invest bottom-up.”

— Seth Klarman

The stock market has more than doubled from the March 2020 lows. It is up more than 40% from the pre-COVID high.

The unexpected outcome is likely underpinned by the government’s response to the pandemic: loose monetary policy and copious stimulus.

The following graph shows the market yield on the 10 year treasury, a good proxy for nominal interest rates.

The following graph shows the M2 money supply over the last 30 years. Notice the steep increase from $15.4 trillion to $18.4 trillion in 2020.

These factors combined have helped boost equities. But equities are not the only impacted market. Asset classes across the board have seen strong, broad growth.

Median home prices are up nearly 20% year-over-year, from $337,5000 to $404,700.

Alternative asset managers including VCs, real estate private equity, and buyout private equity have more cash available than opportunities.

Startups are raising larger rounds of financing at higher valuations. Two anecdotes from this last quarter:

One startup with $1M in ARR raised $20M at a $100M pre-money valuation; a 100x multiple!

Another startup with $100K in ARR raised funds at a $20M valuation; a 200x multiple!

While the increased money supply and loose monetary policy may be driving up asset prices, the stock market’s performance seems to be supported by fundamentals.

The following graph shows the S&P 500 share price on the red line, and earnings per share scaled by a multiple of 20x on the black line.

Earnings growth is driving the current bull market.

There are a lot of concerns and worries about the durability of the bull market. Skeptics find it overvalued, claiming it won’t continue for long. As long as companies are able to demonstrate earnings growth, there seems to be room to run.

Google’s parent company Alphabet provides a concrete example of how earnings can drive price appreciation.

In the third quarter, Google’s earnings per share increased over 70% year over year.

Even as Google’s EV/EBITA multiple compressed from a peak of 18.3x to 15.8x, Google shares were able to post a gain of 18.5% for the 6-month period. Google shares are up 67% for the year.

Large cap companies like Google have helped the market hold up in the midst of underlying turmoil.

Given the strength of the market and the ongoing rotations, it would not be unreasonable to expect some weakness in the future. Indices would surely reflect any weakness in large caps.

Stock selection may turn out to be an important strategy for next year.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.