2022 Q3 Review

Quarterly review of results, the market, portfolio companies, and insights

Results

The third quarter of 2022 ended on September 30th, 2022.

For the third quarter, the consolidated return for Torre Financial accounts was -5.74%.

For the same period, the S&P 500 (SPY) returned –4.93%.

Returns for individual accounts may vary as each account is managed separately.

Market

The third quarter got off to a strong start, as the market bounced nearly 20% in the summer with expectations of a Fed pivot. A Fed pivot, unofficially, is any signal from the Fed loosening up on rate hikes, such as by either hiking by less than expected or pausing hikes all together.

On August 26th, Fed Chair Jerome Powell concluded the Jackson Hole conference with a surprisingly straightforward speech.

“Without price stability, the economy does not work for anyone. In particular, without price stability, we will not achieve a sustained period of strong labor market conditions that benefit all.”

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

“Longer-term inflation expectations appear to remain well anchored … But that is not grounds for complacency, with inflation having run well above our goal for some time.”

Powell has been very clear in his resolution to abate inflation. The market took notice and gave back all of the summer gains in September.

Equities and bonds alike are feeling the pain. “The 10-year treasury bond is on pace for its worst year ever (-16.7%) and a 60/40 portfolio of the S&P 500 and 10-year bond (-21%) is on pace for the 2nd worst year ever, trailing only 1931,” states Chris Bilello.

This year has been referred to as Powell’s “Volcker Moment.” Fed Chair Paul Volcker is credited with curbing inflation in the early 1980s, as inflation peaked at 14.8%, by raising rates from 11% to 20% in a short period of time. It led to the 1980-1982 recession, where unemployment rose to over 10%. US monetary policy eased in 1982, helping lead to a resumption of economic growth.

Inflation is particularly sticky in wages and housing. The Fed is looking for the unemployment rate to rise and wages to fall, in order to slow inflation. On the housing front, mortgage rates climbed to 6.7%, the highest since 2007. While the effects may take a while to permeate due the dynamics of the residential market, this should eventually bring down home prices and rent.

The Fed has been called to pause hikes. Jeremy Siegel, Professor at Wharton and author of Stocks for the Long Run, passionately made his case on national TV: “calling it poor monetary policy is an understatement”. The United Nations pressed the Fed and other central banks to stop raising rates.

Somewhat inadvertently, the UK has already pivoted.

In an effort to address double digit inflation, the Bank of England has been trying to increase rates, most recently increasing to 2.25%. At the same time, the government announced a major spending program and major tax cuts in an effort to offset fast-rising energy bills. While it may alleviate short-term pressures, markets worry it will further fuel inflation. Yields spiked.

As the pound sank to record lows and bond prices fell, pension funds were being forced to sell assets, leading to a downward spiral. The Bank of England had to step in to buy bonds – essentially reversing course and implementing quantitative easing (QE).

In the US, market participants continue watching closely for any sign of a pivot.

Portfolio

Top performers in Q3 2022

Profitable, high-growth portfolio companies performed well during the third quarter, holding on to gains throughout the quarter’s volatility. Many are still down significantly from the beginning of the year.

PayPal (PYPL) stands to benefit from a few dynamics including volume increases from inflation, getting through the eBay comps, and the tempering of the non-profitable competitors as the cheap cash era comes to an end. Online payments is still a competitive area, with heavy players including Google Pay, Apple Pay, Shop Pay, and Amazon Pay.

The Trade Desk (TTD), Snowflake (SNOW), and Paycom (PAYC) continue to grow and demonstrate strong margins. Paycom, in particular, benefits from rising rates since they take a float on the payroll they process.

Cloudflare (NET) continues to innovate at a rapid pace, while beginning to show operating leverage. They just wrapped up their 12th Birthday Week with over 36 product announcements including first zero-trust SIM, Workers Launchpad which is a $1.25 billion fund with VCs, Turnstile, and much more.

For the latest analysis, see

Q2 2022 Earnings Roundup 8.13.2022 for PAYC, DDOG, NET, TTD

Q2 2022 Earnings Roundup 8.27.2022 for SNOW

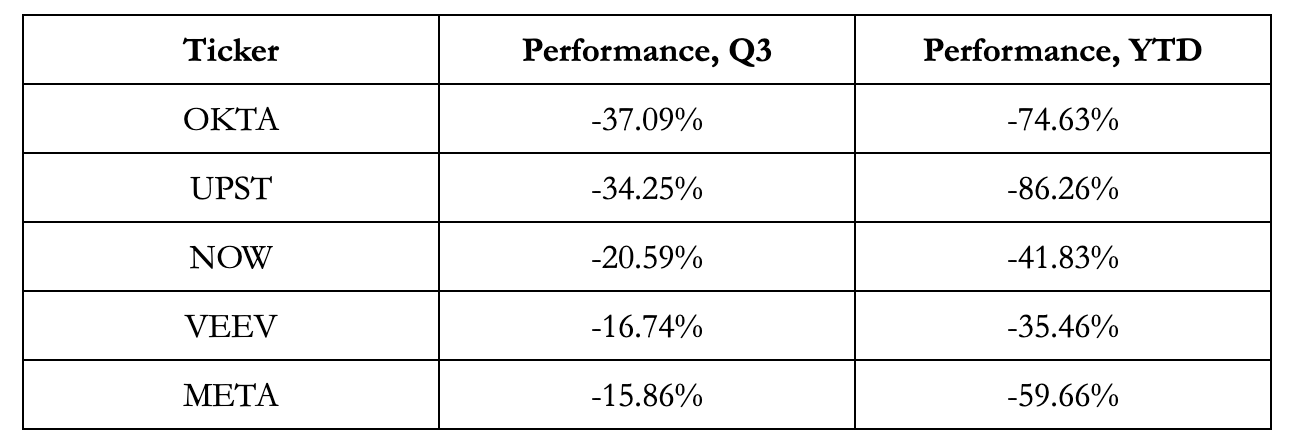

Bottom performers in Q3 2022

In the bottom performers cohort, there’s a mixed bag.

ServiceNow (NOW) and Veeva (VEEV) seem to represent meaningful opportunities. Both demonstrate strong revenue growth and profitability. The macroeconomic picture has brought headwinds such as the strong dollar and longer deal cycles. The businesses are fundamentally sound. Positions have been accumulated throughout the quarter.

Okta (OKTA), Upstart (UPST), and Meta (META) are more in show-me mode. Positions have been reduced throughout the quarter.

Okta is working through issues after acquiring Auth0. The leadership team also seems to be going through some change, with the Chief Product Officer departing and Fredric Kerrest – COO, co-founder, and Okta-evangelist – taking a one-year sabbatical. Okta has an enormous opportunity ahead, but they do have some work to do to get things together internally. I’d like to see growth maintained and profitability trending in the right direction before considering accumulating.

Upstart has been battered by rising rates. Because Upstart is a marketplace, they depend on institutional investors to provide financing for the loans they offer. Investors have been cautious to place capital in a rising interest rate environment. Additionally, the increasing likelihood of a recession doesn’t typically fare well for personal loans. Upstart’s management team has flip-flopped on using their strong balance sheet for funding loans. As of the last announcement, they decided they would fund loans opportunistically. The core thesis remains intact – vast amounts of data should enable a more accurate underwriting process. The market is very large from personal loans, to auto loans, to mortgages. In order to truly scale, they will need to make the marketplace work. Using their balance sheet won’t be sufficient. They will need to gain the trust and confidence of institutional investors.

Meta has had a challenging year: Apple’s iOS changes have affected mobile ads targeting; they have committed to deeply investing in the metaverse which has a long-payoff as rates have risen; and there has been increased competition from TikTok, Youtube Shorts, and more. Meta was one of the first to slow hiring and is looking closely at individual performance internally. While growth has slowed dramatically, Meta is very profitable. Meta will need to show a return to growth, ideally double digits, to regain investor confidence.

For the latest analysis, see

Q2 2022 Earnings Roundup 9.10.2022 for OKTA

Q2 2022 Earnings Roundup 7.30.2022 for META

Insights

Intuition behind rates and valuations

Posted here in September 2022, A Capital Market's Perspective on Valuations can help build an intuition of how interest rates impact valuation.

Options as derivatives or as drivers behind the market?

While options are often considered a derivative instrument, Cestrian Research alludes to the relationship being inverted. Given the volume and scale, option activity could actually be a driving force behind movements in markets. When market participants buy options (puts or calls), the option dealers (typically market makers) have to take a position to hedge out their exposure. Because options expire on a common schedule, the unwinding activity is batched. When there is a significant imbalance between puts and calls, this can lead to significant market volatility. Read more here and here.

High growth showing strength

In an October issue of Clouded Judgement , Jamin Ball points out the correlation between revenue growth and revenue multiples amongst high growth cloud software companies with high free cash flow margins.

He also calls out the recent divergence in valuation multiples of high growth cloud software companies. While the low-growth and mid-growth cohorts have lingered, high-growth valuations have demonstrated strength.

On creating wealth

The 2004 essay from Paul Graham, How To Make Wealth, promotes the idea that wealth is not constrained or fixed, but rather can be created. It covers many topics spanning from differentiating money and wealth, growing the pie, breaking down a job and its role within an organization, the value of measuring and applying leverage, the trade off between sacrifice and intensity of a start up versus a larger company, getting acquired, and much more.

Although published nearly 2 decades ago, it is just as relevant today.

As an example, consider the following excerpt:.

“Potential buyers will always delay if they can. The hard part about getting bought is getting them to act. For most people, the most powerful motivator is not the hope of gain, but the fear of loss. For potential acquirers, the most powerful motivator is the prospect that one of their competitors will buy you. This, as we found, causes CEOs to take red-eyes. The second biggest is the worry that, if they don't buy you now, you'll continue to grow rapidly and will cost more to acquire later, or even become a competitor.”

It is an apt description for recent news of Adobe acquiring Figma for $20 billion, a roughly 50x EV/NTM revenue multiple in the midst of a highly volatile macroeconomic climate.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.