2023 Q2 Letter

Review of quarterly results, look at top performers and detractors, and personal reflection

Results

The second quarter of 2023 ended on Wednesday, July 31st, 2023.

For the quarter, the consolidated return for Torre Financial accounts was 13.18%

For the same period, the S&P 500 (SPY) returned 8.68%.

Returns for individual accounts may vary as each account is managed separately.

Portfolio

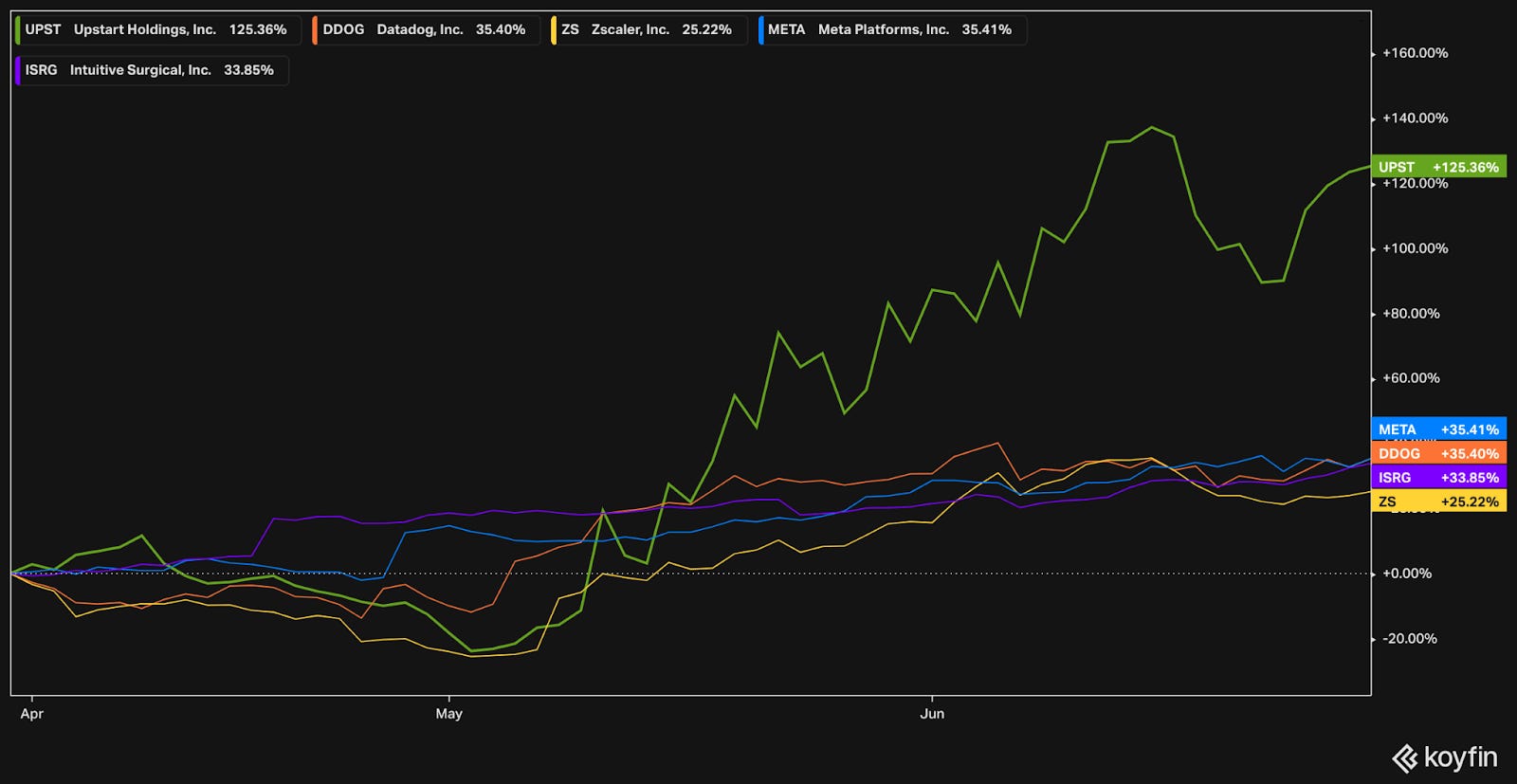

Top Performers in Q2

The momentum with technology companies continued into the second quarter. Big tech seems to be stabilizing as money appears to slowly rotate into more attractive opportunities.

Upstart (UPST) had a significant turnaround this quarter, catalyzed by their Q1 earnings wherein they announced new capital market partners. As a reminder, Upstart’s business has been crushed by the increasing rate environment & recession worries. The majority of their revenue comes from a commission fee from originating loans on behalf of their partners. As rates are rising, fixed rate loans (like bonds) become less valuable – over time, capital can be placed in new loans with higher rates. Now that rates are stabilizing and Upstart has secured a large capital markets partner to provide funding for new loans, Upstart should be able to perform much better. Short sellers are leaving. We are holding a small allocation due to the significant volatility.

Meta (META) is making progress alongside many fronts. They have demonstrated continued financial discipline, such as reducing headcount and capital expenditures. Their Quest VR headsets are well positioned, especially on the tail of Apple’s Vision Pro launch. The Vision Pro sells for $3,499 while Quest headsets start as low as $299. Although different products and markets, the flurry of media will certainly benefit Quest sales. Meta continues to innovate, most recently launching a Twitter-competitor called Threads. Building off the Instagram community, Threads is well positioned to take market share from troubled Twitter. Meta has historically been very successful building better V2’s – examples include Stories, Reels, filters, and more. threads. Additionally, the narrative and sentiment around Meta has changed materially from a few years ago.

Datadog (DDOG) is a leader in application observability, allowing software developers to monitor their applications. Due to their consumption-based business model, Datadog has seen more fluctuation than other seat-based SaaS companies. Customers are able to focus on optimizations to reduce their consumption spend. On the positive side, as consumption bounces back, so does spending. In fact, Datadog was a bottom performer in Q1 as worries pressured the shares. In Q2, consumption seems to be normalizing which is reflected in the price movement. Datadog is well positioned to continue growing with their customers through digital transformation, a strong secular tailwind.

Intuitive Surgical (ISRG) is a leader in robotic surgery. They have an attractive razor blade business model, where they sell ongoing consumables for use with their installed machines. Intuitive is benefiting from the recovery of operations, which are seeing an uptick after being depressed due to COVID. Intuitive was also a bottom performer in Q1, again showing the rotation theme. Intuitive is a fantastic company – and is priced as such! We are holding a small allocation due to the excessive valuation.

Zscaler (ZS) is a leader in zero trust network access. Every enterprise has digital workflows, historically these were hosted on premise and protected by firewalls and VPNs. As technology evolves and workloads shift to the cloud, that model is insufficient. Zscaler’s solution has been well received and gained significant traction amongst large enterprises. Cybersecurity is an attractive space, and Zscaler is operating exceptionally well. Zscaler is founder led, has persistent high growth, and is generating strong free cash flow.

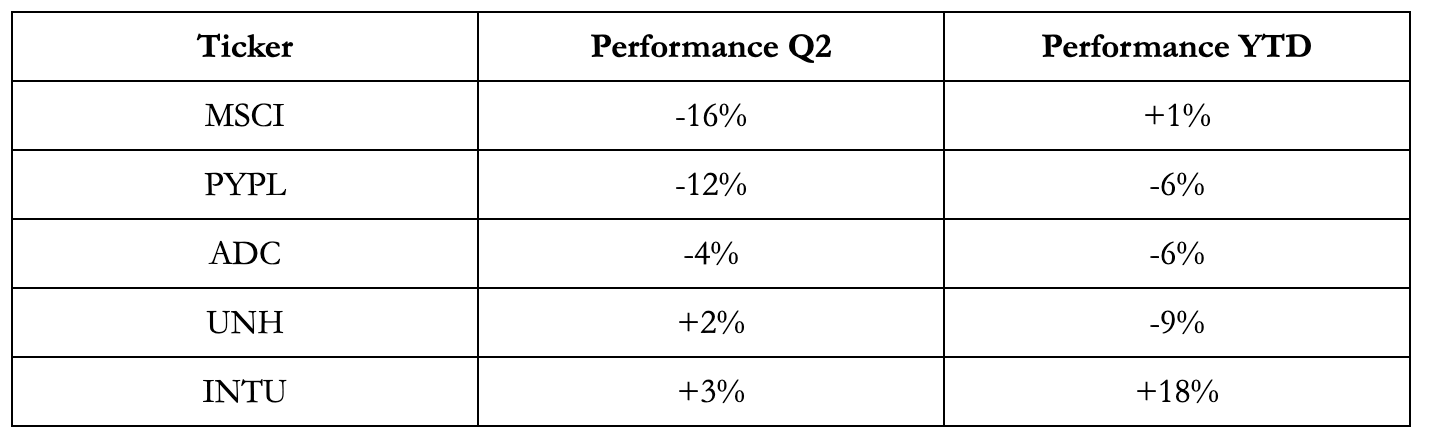

Bottom Performers in Q2

For the most part, the detractors were mostly steady throughout the quarter.

MSCI (MSCI) had a slight revenue miss (~1%) in Q1, resulting in a 13% drop. Investors read into the weakness, as ESG and Real Estate were under pressure. MSCI is well positioned in the index industry and sells high-margin financial information. While we have a smaller allocation, we are not worried and look to build the position over time.

PayPal (PYPL) is another attractive opportunity. The business is facing margin compression due a change in their revenue mix. They made what we see as the right call in extending their business beyond their branded PayPal checkout business to provide all processing services for their customers. While the unbranded processing services are lower margin, they significantly increase PayPal’s relevance and stickiness. PayPal provides significant value to merchants via integrated checkout options and streamlined backend processes. On the consumer side, PayPal continues to invest and innovate at a rapid pace. They recently shared their plans for a PayPal vault, wherein consumer credentials will be stored in one central location and streamline checkout across the entire PayPal network – even without a PayPal account. While we believe PayPal is doing the right things and increasing relevancy, we expect shares to be under pressure until they announce the next CEO.

Agree Realty (ADC) was a bottom performer in Q1 and has shown up again; it is also the only REIT in our portfolio. Real estate generally has been under pressure from the high rates as well as economic troubles in certain real estate sectors. Agree Realty focuses on the highest quality properties and tenants. They have low leverage and are well positioned. We are bullish on ADC; it is a great option for rotation.

UnitedHealth Group (UNH) was a bottom performer in Q1 and has shown up again, although with a +2% performance. The recovery in operations that benefits Intuitive Surgical has the opposite effect on UnitedHealth, as they are the insurance company that ends up paying for those.

Intuit (INTU), +3% this quarter, is the parent company behind Quickbooks, TurboTax, Mint, and Mailchimp. These services cater to small-and-medium businesses. Smaller companies are particularly vulnerable to recessions and do not always survive. The IRS is also planning on launching a free tax service in 2024 which may introduce competition for their TurboTax offering. Notwithstanding the concerns, Intuit increased earnings and revenue guidance for the year in their most recent earnings announcement.

Activity

As introduced in our 2023 Q1 Letter, we are continually evolving our processes and started tracking our activity this year.

We strive to keep portfolio turnover at a minimum. Each company is rigorously evaluated and vetted as a long-term opportunity before being introduced. To enter and exit quickly would indicate a mistake had been made.

With a target 5+ year holding period and 30 holding companies, the implication is we turn over fewer than 6 holding companies a year. We had one addition in April, for a YTD total of two.

While our turnover activity is low, it requires a significant investment in research. We spend a lot of time learning, so that we can have the best possible companies and target allocation. Whether diving into a new company or industry, or learning a new concept, we strive to always be learning. We believe that every mental model, even if not directly associated with investing, can be additive and amplify understanding through different perspectives, inline with Charlie Munger’s mental latticework.

Diving into our portfolio company target allocation weights, …

Subscribe to continue reading about our personal activity — new, exited, increased, reduced positions; reflection; what we’re thinking going forward

Keep reading with a 7-day free trial

Subscribe to Torre Financial Newsletter to keep reading this post and get 7 days of free access to the full post archives.