2023 Q1 Letter

Review of quarterly results, look at top performers and detractors, and personal reflection

Results

The first quarter of 2023 ended on Friday, March 31st, 2023.

The consolidated return for Torre Financial accounts was 16.72%

For the same period, the S&P 500 (SPY) returned 5.97%.

Returns for individual accounts may vary as each account is managed separately.

Portfolio

Top Performers

Technology companies came roaring back in the first quarter, presumably due to a combination of portfolio underweighting and realization that we are now late in the rate hiking cycle.

META’s performance turnaround mirrors their own pivot – from investing heavily to the future to focusing more on the needs of today. Although Zuckerberg owns roughly 10% of the company, he holds nearly 60% of the voting power. Zuckerberg’s steadfast mindset on the metaverse and other long term investments had escalated the concerns about capital allocation, causing investors to flee. In 2023, META pivoted their messaging towards more disciplined allocation to future efforts, a renewed focus on their core offerings, and a focus on efficiency. Expenses have been reduced dramatically, including operating expenses such as salary as well as capital expenditures.

Additionally, META has focused on their offerings including monetizing the business use of Whatsapp, improving their AI models for recommendations and attribution, and optimizing ads on Reels and other products. Sales growth is estimated at 5% for 2023 and 11% for 2024. This is a positive signal, and inline with expectations. From a July 2022 article, I had commented: “Meta is essentially a value stock at this point. Our focus on compounders does call for growth. We’ll want to see growth return, and expect to see double digit growth return over the next two years.”

Salesforce (CRM) has had a similar shift in priorities. The pressure had been building up after a few activist investors, one of which was Elliott Management, built up a sizable position. Marc Benioff, who had recently become the sole CEO, began focusing on efficiency and performance. On the March 1st, 2023 earnings call, Marc Benioff opened up re-emphasizing their new focus: “Improving profitability is our highest priority, and that really showed up this quarter. Our goal is to make Salesforce the largest and most profitable software company in the world, and that is what we are doing.” Salesforce is the undisputed leader in the CRM category. Durable revenue coupled with ongoing growth and high profitability are the characteristics I look for in compounders.

Airbnb (ABNB), Cloudflare (NET), and The Trade Desk (TTD) are younger and faster growing companies.

The COVID pandemic was truly transformational for Airbnb. Their business was hit very directly as travel came to a halt with bookings dropping over 70%. Instead of standing flat footed, ABNB transformed their cost structure – they reduced the workforce by 25%, cut the marketing budget by $1b, reduced executive salaries, and much more. They focused the energy they had on the core business, addressing customer and employee needs. They revamped their internal process to have a single roadmap, driving clearer focus internally. Gross margin has expanded from ~70% pre-COVID to ~85% post-COVID. ABNB has +16% return on invested capital, and +43% FCF return on invested capital. All while continuing to grow. Airbnb was quick and early to get on the efficiency focus, and that is now paying off. There are concerns about the upcoming recession impacting travel. Although there may be some softness ahead, the long term thesis is intact. ABNB seems reasonably priced at a 21x on FCF, or FCF yield of 4.8%.

Cloudflare continues to innovate at a rapid rate. It has been very impressive to see Matthew Prince and team build new offerings and enter new markets. Starting with a cloud-delivery network (CDN), Cloudflare now offers scalable storage, edge computing, and cloud network security. All of their offerings are built on top of their core infrastructure. Cloudflare is aggressive in going after the cloud titans (“AWS’s Egregious Egress”) and other leaders such as Zscaler (“Descaler Program”). Cloudflare has recently turned the corner to be FCF positive and expects expansion going forward. Their revenue growth has been very steady, and maintained in the high 30% 's even throughout the shifting macroeconomic landscape. Given their strong performance and nearly endless opportunities, NET is very pricey at 16x NTM revenue (P/S).

The Trade Desk (TTD) offers an ad-buying platform. They are creating an open marketplace, where buyers can purchase media placement across a multitude of platforms. This allows them to optimize spend across different options, as opposed to the closed ecosystems offered by the large advertisers such as Google and Meta. This long-term thesis seems inevitable, and TTD has been performing well. They continue to expand market share, growing in the midst of a broader slowdown in marketing spend.

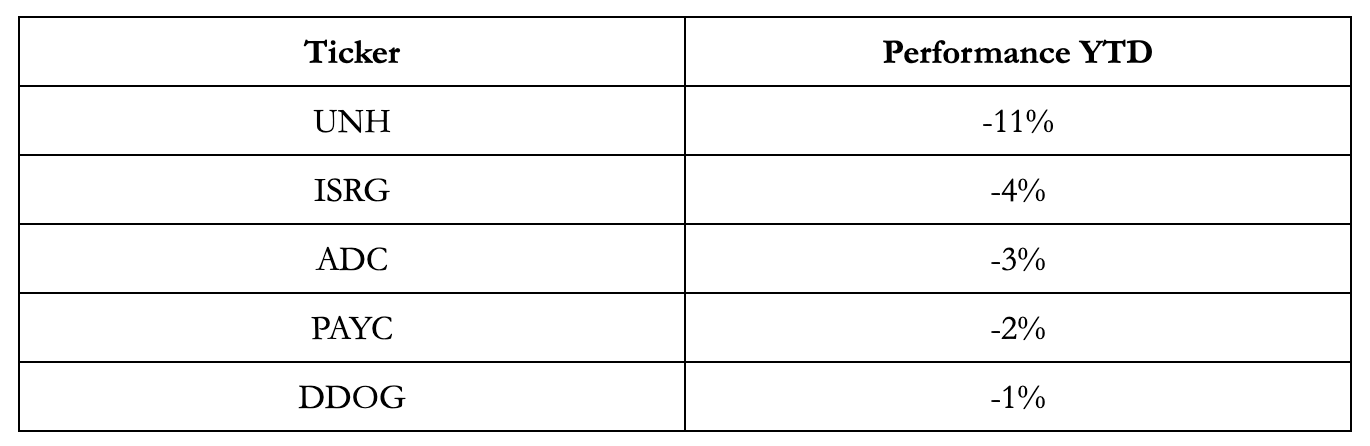

Detractors

The risk-on mindset of the quarter had opposite effects to more defensive sectors.

UnitedHealth Group (UNH) is as steady as it goes. Deeply entrenched in the medical insurance ecosystem, UNH has been steadily compounding capital for years. Valuation has been steady at roughly 22x earnings, or a yield of 4.5%.

Similar in the healthcare industry, Intuitive Surgical (ISRG) is a leader in robotic surgery. They have a solid razor-razorblade business model wherein they monetize the consumable elements for every installed machine. Valuation is, and has always been, quite pricey, currently at nearly 55x earnings. Position sizing reflects the inherent risks to valuation.

Agree Realty (ADC) is the one REIT in the portfolio. Because REITs are required to distribute 90% of earnings, it is more challenging for them to retain earnings to compound. Through depreciation and related mechanisms, they can retain and compound a bit more of the cash flow. REITs are typically considered more defensive as they offer a good balance between appreciation and current cash flow. Agree Realty has been very proactive in both developing and financing projects, always focused on the highest quality tenants.

There was no clear catalyst for the drop beyond perhaps rotating money from defensive positions towards a more risk-on approach.

Paycom (PAYC) and Datadog (DDOG) are both software companies that seemed to move counter-trend. Concerns about the upcoming slow down seem to be weighing on both.

Paycom offers payroll and HR software to small and medium businesses – the Fed’s fight against the strong employment market is not necessarily a positive catalyst here.

Datadog is a leader in software observability, allowing developers to monitor and understand how their systems are operating. Their business model is consumption-based – customers pay for what they use. Over time, this need is bound to grow exponentially especially as AI takes off. For the time being, the focus on efficiency and cost reduction is hitting their top line. Growth is expected to slow from 62% last year to 25% this year. It is likely to reaccelerate after that.

Reflection

Last year was difficult for the markets. The first rate hike in March 2022 placed the Fed Funds Rate at 0.25-0.50%. By the end of the year, following the December 2022 hike, rates were up over 10x to 4.25%-4.50%. Volatility rocked every corner of the market, with long duration bonds down 30% and long duration equities 50%, 60%, even 70%+.

Such a drastic change of the risk-free rate results in a very real shift in the value of future cash flows. Multiples, driven by sentiment and perception of the future, will fluctuate over time and are likely to overreact.

That being said, business owners focus on building their business from the ground up. Business owners pay attention to their fundamentals – growing sales, driving efficiency, optimizing cash flow and more.

In the same way, I look to invest in companies for the long term. While it is important to be open and aware of possible changes to the thesis, it is also important to look beyond the price volatility.

When investing in equities, volatility should be expected. The range of results in any 1 year period can be very broad, ranging from -39% to +47%. The best antidote to this volatility is time. As the holding period increases, the volatility declines.

Over a 5 year holding period, annualized returns range from -3% to +28%

Over a 10 year holding period, annualized returns range from -1% to +19%

Over a 20 year holding period, annualized returns range +6% to +17%

In order to be successful and withstand the temporary volatility, investors have to have conviction. Investors cannot just go with the flow or borrow conviction – their commitment is likely to break down at the worst time. It is important to have a resolute, independent view. Conviction is ultimately a behavioral challenge, one that can be supported by analytical research.

I am constantly iterating and improving my process to 1) make sure I have the best companies for my approach and 2) challenge and/or reinforce my conviction in our holdings.

To do so, I need to always be learning. I am starting to track my activity to hold myself accountable.

I also want to better track my decisions with the end goal of optimizing them in pursuit of the goal of attaining 15%+ annualized returns. I want to be as objective and rational as possible in evaluating investment decisions.

I track my target portfolio allocation over time to always have an understanding of the appropriate size of any particular position. I review it monthly, ensuring the target weights reflect the combination of risk and reward informed by new developments, valuation, and more.

For each company, I track detailed financials to understand the fundamental direction. I also follow them closely, to have a strong qualitative understanding of the management team and the company’s opportunities.

For each company, I have a long term thesis. As an iteration to my process, I am working on having that better organized for each company. I also plan on justifying every change in allocation in the same thesis document, so I have clarity in what is driving my actions.

In the same company-level notes, I plan on looking out into the future to the extent possible. In order to be successful investing today, I want to look out 18 months.

Having all of this documented will allow me to more effectively review & reflect back on my decision-making process. I want to better track my activity, decisions, and progress to more effectively learn from my own experiences.

Personal fun fact

The last two market bottoms have coincided nearly perfectly with my last two daughter’s birthdays.

The COVID low came in on 3/23/20. Alia Torre was born 3/24/2020.

The most recent low from inflation and rate hikes came in on 10/13/2022. Tessa Torre was born 10/15/2022.

Good news - we’re not expecting anytime soon!

Closing

Last year was challenging. This year is off to a strong start. Although the economy is expecting turbulence ahead, markets are forward-looking and tend to bottom out well in advance. That is not to say that there won’t be more volatility ahead. In fact, the recent market strength is likely due for a pull back.

While I monitor macro indicators and incorporate those insights into my decisions, I focus primarily on finding and investing in the highest quality companies at attractive valuations.

I have strong conviction in our portfolio companies. I will continue to work hard to re-evaluate and reinforce my processes to best ensure that every decision and investment I make clears our hurdle rate – a path to 15%+ annualized returns over the next 5 years, or a doubling of capital every 5 years.

To those that have trusted me with their capital – thanks for your patience. It is critical for a successful partnership.

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.