Market & Earnings Review - March 4, 2023

Market commentary, portfolio company earnings results, and closer look into Salesforce (CRM)

Market

After climbing throughout January, the market met resistance with the SPY down about 3.5% in February. After this week’s rebound, the market is still up 5.7% for the year.

The technical picture seems constructive, with the 50d SMA steadily above the 200d and the week closing out above the 50d. There is a chance the February dip can become a higher low, and for the market to go on to hit a higher high.

Strong economic data in February added to the “higher for longer” story. Activity came in hot across not only the CPI (0.5% vs 0.4% expected) and PCE (0.6% vs 0.5% expected), but also from external factors like China (PMI 52.6 Feb vs 50.1 Jan). No recession yet.

These indicators challenged the story that propelled markets in January – that the Fed was close to ending the rate hikes. Good news was bad news, and markets sold off.

Whereas the market had been pricing in two more 0.25% hikes, the futures market now expects three such increases. After that, the Fed is expected to pause.

This week, good news was good news. The US services sector showed expansion with the Services PMI for February coming in at 50.6 vs 46.8 in January. Markets cheered the result.

While equity markets are attempting to push higher, so are bond yields. The inverse relationship is apparent from the chart below.

The yield on the 10-year Treasury closed above 4% for the first time since November. It will be difficult for equities to go much higher if bond yields continue to climb.

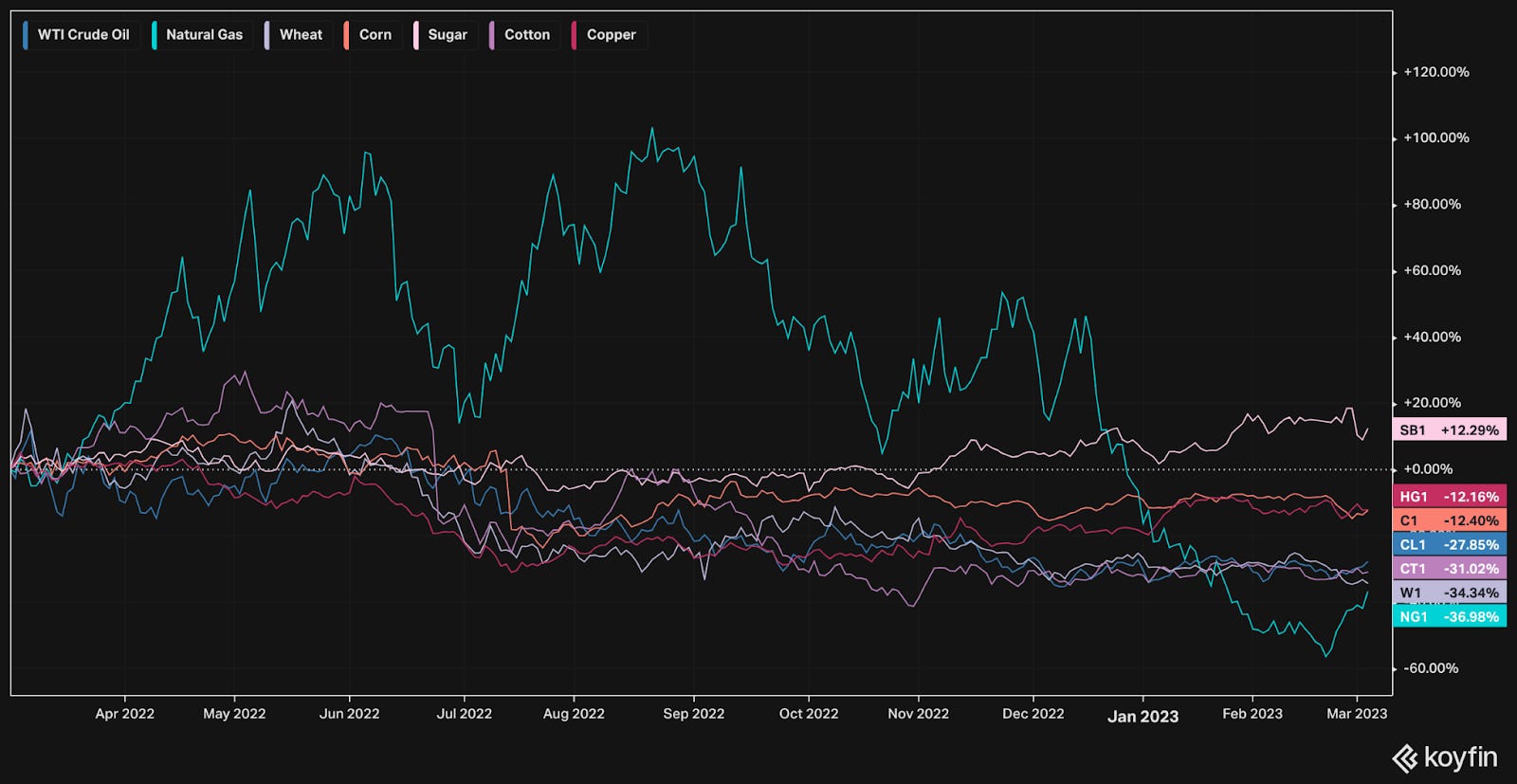

Commodity prices are useful leading indicators into inflation, and therefore yields.

Over the last year, prices have been generally coming down, easing inflationary pressures.

The effects of higher yields take time to work through the economy.

From 2022 Market Review - December 31, 2022, I mentioned housing was due to come down.

“The true effects of the rate increases on the economy take time.

The real estate market is a prime example. As rates climbed, mortgage rates increased from ~2% to ~7%. Interestingly, housing prices have yet to come down. Sales, however, ground to a halt – fewer deals are being made, presumably as expectations between buyers and sellers have widened. “Stable” prices, based on low volume, may not be as stable as they seem. The inability to sell has sellers switching to renting. If demand in the rental market holds steady, and the supply increases, rental prices will come down. This in turn will lower the attractiveness of switching to renting, and incentivize deals at lower prices.”

Mortgage rates are high.

According to Redfin, a buyer with a $2,500 monthly budget at 3% rates could afford to pay $518,000 for a home. Today that same buyer can only afford $384,000.

Fewer transactions are happening and prices are coming down. While homeowners have the option to hold on to their homes and defer a sale, new homes don’t have that luxury. They must be sold, and at the going market price.

The average price of a new home sold in the US is now down 16% from the peak last July.

And as Charlie Bilello pointed out, a 16% drop is simply not enough. To have the same level of affordability as a few years ago, prices would have to come down much more.

Q4 2022 Earnings

Over the last two weeks, six portfolio companies reported earnings: Intuit, Workday, Salesforce, Snowflake, Veeva, and Zscaler.

Summary of sales:

Revenue this quarter exceeded expectations across the board. Guidance was mostly inline with the exception of Snowflake and Veeva Systems.

Detailed results:

Commentary:

Intuit demonstrated significant profitability improvements this quarter, exceeding expectations on EBITDA (28% margin!) and EPS. Sales growth remains inline with expectations. Intuit’s revenue jump for next quarter is due to seasonality from the upcoming tax season, as Intuit is the parent company behind TurboTax.

Workday’s results were broadly in line. Being a large enterprise SaaS offering, it isn’t surprising they have visibility into their business and have been able to manage expectations. While the layoffs across large companies are likely affecting them, they seem to be managing well. Workday’s EBITDA margin for the quarter was 24%.

Salesforce had a huge surprise to the upside on profitability, which was cheered by the market. More to come in the section below.

Snowflake is seeing growth slow down faster than anticipated. In the prior quarter they gave preliminary guidance for FY23 of 47% growth. This quarter, they revised that down to 40%. This is in part due to Snowflake’s consumption-based business model – customers can ramp activity up and down at their discretion. That being said, Snowflake has a long and promising runway.

Veeva is going through a change in how they recognize revenue from contracts, regarding “termination for convenience rights” or TFC. Essentially they will be more conservative in recognizing revenue going forward, since a customer could cancel their contract. Without making this change, their guidance for the year would have been ~15%. Due to this issue, they are guiding for 10% growth. Anticipating market concerns, they provided guidance for next year as well, and called for nearly 20% growth!

Zscaler had a solid report. Revenue is growing at 50%+, FCF margins are healthy at 10%. Guidance was slightly raised. Yet, the market reaction was negative, perhaps due to the premium valuation.

Salesforce (CRM)

Salesforce is likely a familiar name. Led by Marc Benioff, Salesforce was the pioneer into selling software as a service. They popularized the famous land-and-expand strategy, where the initial offering is accessible to new customers and they expand their usage over time.

Salesforce’s core offering is a customer relationship management (CRM) suite that enables the entire customer lifecycle from lead to sale through ongoing support. Founded in 1999, their offering is as popular as ever. They are the dominant player, in part due to their open platform approach, which has allowed other solutions to be built on top of their platform.

Revenue growth has been strong over the years. From Marc Benioff himself:

To grow a business from $4 billion to nearly $35 billion in 10 years is a remarkable achievement. One key strategy they have applied over the years is M&A.

Net income, though? Not so much.

One of the appealing things about a software company though is that management does have discretion. A significant amount of the expenses are towards new functionality and/or offerings. Sustaining existing offerings can be done typically much cheaper. This allows management to toggle a will. Activist investors have been pressuring Salesforce to make this shift.

Benioff opened the most recent earnings call with their commitment to driving profitable, sustainable growth going forward:

“Improving profitability is our highest priority, and that really showed up this quarter. Our goal is to make Salesforce the largest and most profitable software company in the world, and that is what we are doing.”

Do the numbers show it?

Revenue growth for the quarter came in higher than expected with q/q acceleration into Q4. Looking at the TTM revenue, we can expect the 18% to come down closer to 14-15% over time.

Gross margins jumped up to 75%, from 73% and 72% in the prior quarters, showing efficiency gains in how they deliver their offerings.

EBITDA margins jumped up to 28% from 23%, benefiting from the disciplined spend from G&A and R&D.

FCF margins also jumped up 20% from 18% prior, showing cash management discipline in working capital and capex investments.

Net cash increased from 1.3b to 1.9b.

Shares are down 1% y/y, showing the benefit from the $10b buyback program announced in August. They have deployed $4b so far, which seem to have been timely purchases with a low stock price. In the most recent quarter, another $10 billion was added to the buyback program for a total of $20 billion.

Salesforce has a large total capital base, resulting from a combination of their large M&A activities and share dilution over time. M&A purchases show up as goodwill on the balance sheet and that goodwill tends to linger. Given that context, their return on capital metrics ranging from 7-10% seem adequate.

The market applauded the results and guidance. The numbers show their commitment towards profitability. Marc Benioff even mentioned they will be disbanding their M&A committee, further reinforcing their re-focusing on their core offerings.

Although still down over the past year, shares are up nearly 50% from the December low. The focus on profitability combined with ongoing double digit growth and a durable product portfolio makes for a compelling opportunity.

An interesting aside – Salesforce used to have a Co-CEO at Marc Benioff’s side. In November, Bret Taylor stepped down from the role. The timing couldn’t have been better for Benioff to claim fame for the turnaround that was to come. Could he have known something in advance? Did Taylor step down, or was he asked to step down?

Turning to the valuation:

Salesforce seems to be fairly priced. The continued profitability expansion should help increase the FCF yield over time, at a rate faster than revenue growth.

Closing

Everything is connected. Easy financial conditions led to high demand, which drove up prices and resulted in inflation. In an effort to get control, the Fed has been raising interest rates. As rates rise, the cost of capital increases.

Companies and investors alike have a higher bar to clear for any given investment – the ROI needs to exceed their cost of capital.

As long as companies have cheap capital available (i.e. low-cost financing through debt or a high share price) they will keep investing.

As banks tighten up and share prices fall, companies start paying more attention. They have to operate within constraints.

As investors call for higher profits, companies that can do it are incentivized to do so in order to have access to cheaper capital (i.e. higher share price).

This has played out very clearly with a few companies recently, including Salesforce and Meta.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.