Aftermath to the COVID-19 Expansion

Valuation multiples, rising interest rates, and high inflation

The economic response to COVID-19 presented an unexpected outcome. As covered in SaaS Valuations Post COVID-19, the multiples for many growth companies expanded significantly.

The multiple expansion was unsustainable – reversion to the mean was inevitable.

Since the beginning of 2022, those multiples have been under pressure.

Multiple compression

The following chart, showing EV/NTM revenue multiples for select cloud companies, clearly illustrates the brief COVID dip, the climb to extremes, and the reversion starting just before 2022.

Many individual companies experienced similar roller coasters in price performance.

Work-from-home beneficiaries such as Zoom, Shopify, Roku, Peloton, and Netflix have given up nearly all of the gains, or even more in some cases.

The fundamentals of some of these companies, such as Peloton, have been drastically affected.

Others have made significant progress.

In January 2020, Zoom reported $622 million in revenue with EBITDA of $29 million.

In January 2022, Zoom reported $4,100 million in revenue with EBITDA of $1,179 million.

The market, however, is forward looking and concerned about the outlook.

Sustainable growth is highly sought after. It can have a significant impact on the discounted cash flow valuation analysis, which is then often reflected and communicated through the use of multiples.

Some of our portfolio companies have fared better.

The performance over the same period of time for a few of our emerging compounders are shown below.

While the roller coaster is clearly present, the outcomes have been, in general, better in comparison.

These companies are similarly cloud-based, high growth technology companies. The difference is the relevance and durability of their business beyond the post-COVID shock.

The performance over the same period of time for a few of our established compounders are shown below.

Many of these well-known, high quality companies have enjoyed a much smoother ride.

Notwithstanding the positive returns, many, if not all, of these companies have seen their multiples compress.

Interest rates as a driver behind multiples

In response to the pandemic, the Fed acted quickly to drop interest rates to 0%. This had a broad effect since the Fed’s fund rate serves as a basis for pricing all other interest rate instruments.

The 0% rate policy played a significant role in the expansion of multiples across the market. Lower rates lead to higher multiples. High-growth SaaS businesses were particular beneficiaries. The present value of long-dated cash flows increases as rates drop.

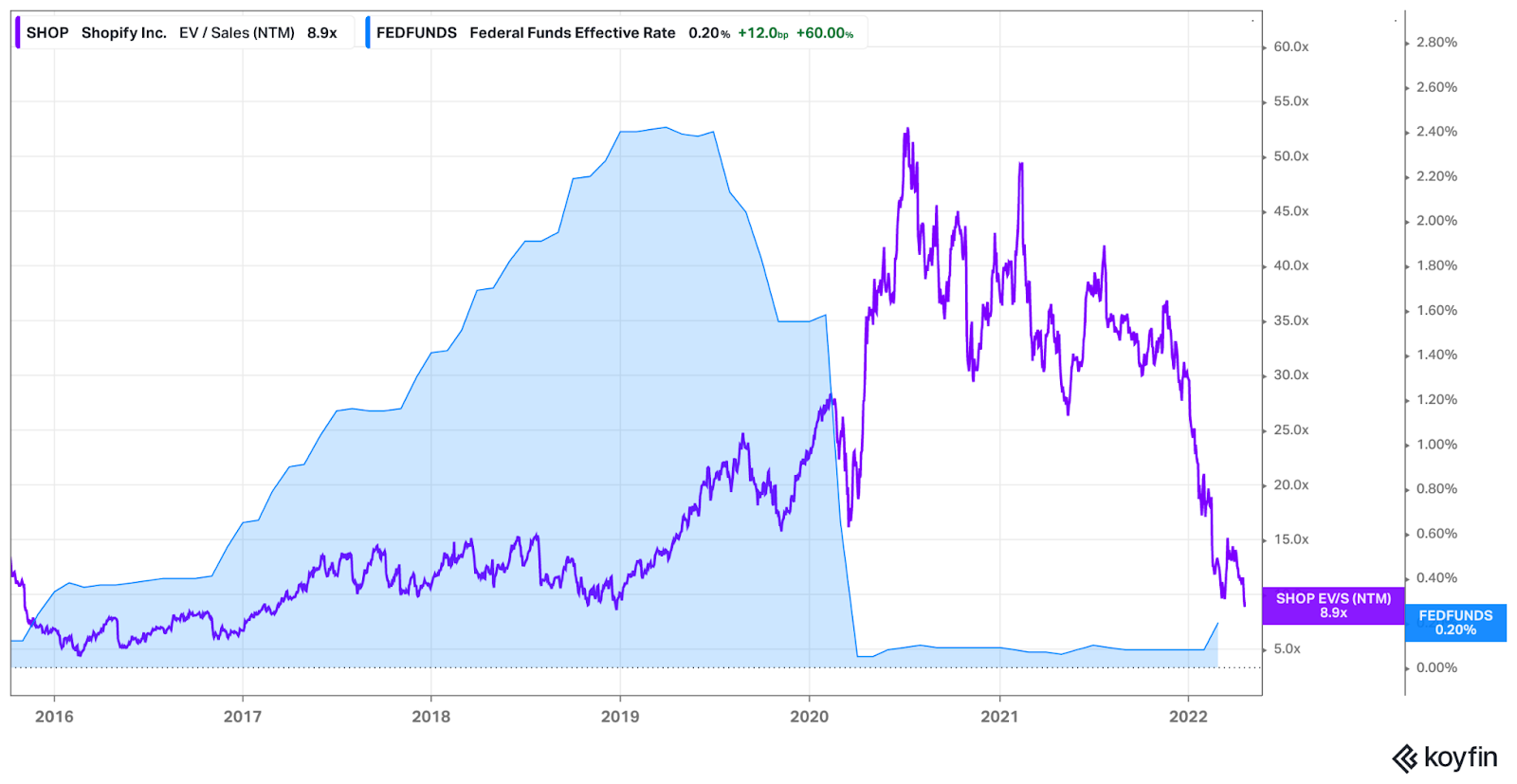

The relationship can be clearly seen in the chart below which shows SHOP’s revenue multiple and the Fed funds rate.

In 2020, when rates dropped to 0%, SHOP’s multiple expanded from around 20x to above 50x.

After peaking in mid 2020, multiples have been on the decline.

The decline gains momentum in late 2021. The market, being forward looking, begins to price in rate hikes, as those signals become more apparent.

The uptick in rates in 2022 shows the first step of the change in policy.

Looking at the previous interest rate hike cycle from 2016 to 2019, however, presents a unique insight. While SHOP’s multiple corrected initially, it began to rise gradually alongside interest rates.

Dot-plot

The dot-plot is a format the Fed uses to communicate their forward looking guidance as to where they see the rate.

As shown below, the majority of the Fed sees rates at around 2% by the end of 2022.

Another important signal is the perception of the market. Futures instruments allow market participants to take positions on these outcomes. The market’s expectations are shown below.

The market is expecting higher rates than the Fed, specifically looking for rates between 2.75%-3.25% by December 14th, 2022.

Inflation as root cause driving rates

While interest rates seem to have a clear effect on multiples, behind the scenes inflation appears to be a root cause.

Fed’s mandate

Controlling inflation is a key element of the Fed’s dual mandate:

“To promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.” - Source

Although three things are mentioned, it is referred to as a dual mandate because moderate long-term rates follow from the other goals of maximum employment and stable prices.

The Fed aims for inflation to be 2% over the long run. Inflation being low and stable leads to a better functioning economy.

“If inflation expectations fall, interest rates would decline too. In turn, there would be less room to cut interest rates to boost employment during an economic downturn. Evidence from around the world suggests that once this problem sets in, it can be very difficult to overcome. To address this challenge, following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation modestly above 2 percent for some time. By seeking inflation that averages 2 percent over time, the FOMC will help to ensure longer-run inflation expectations remain well anchored at 2 percent.” - Source

The following chart shows core inflation rates and interest rates over the last few decades.

Notice how they tend to move in tandem.

The core inflation rate has spiked in 2022, while rates have remained low. It is no surprise that both the market and Fed expect rates to rise.

Concerns regarding high inflation

Rapid changes to monetary policy are undesirable. When things change too quickly, they can result in instability.

High inflation can very well result in rapid, uncontrollable changes and significant instability.

Inflation has a psychological effect on people. It can gain momentum and form a self-fueling cycle, leading to runaway inflation.

For real world case studies, see what has happened in other countries such as Venezuela and Zimbabwe.

Inflation disproportionately affects the lowest income earners, those living paycheck-to-paycheck.

Price increases from inflation are fluid and can occur any day. Because wages are sticky, they tend to be revised once per year. The time offset, or lag, is detrimental. There is also no guarantee that wage increases will cover inflation.

Causes behind inflation

The core economic market dynamics of supply and demand ultimately drive price changes.

Throughout COVID, supply has been challenged by global interruptions. In 2022, the Russian invasion of Ukraine led to additional instability. Financial sanctions closed off Russia from the rest of the world.

These types of supply dislocations can be difficult to adjust. Additional capacity and production often requires capital expenditures and other investments that may take years to come to the market.

When supply is limited, all else being equal, prices rise.

The other side of the equation is demand.

Demand includes the need and willingness to pay.

The combination of limited opportunities for experiences & travel as well as the cash distributions from the government in response to the pandemic led to a surplus of demand. People had cash and had fewer options for where to use it, namely goods.

Demand, unlike supply, can be more easily adjusted on demand. Higher interest rates lead to a higher cost of capital, dissuading additional borrowing and spending. The Fed seeks to adjust interest rates for exactly this reason.

In closing

Valuation multiples for many companies have reverted from their post-COVID expansion. Even if their fundamentals have improved, many individual companies have been significantly adversely affected.

While interest rates have been at an all time low, things are starting to change.

A rapid rise in inflation has caused the Fed and market to expect a need for increased interest rates.

That being said, there are signals of supply chain saturation and peaking inflation. Some macroeconomic experts expect core inflation to subside from the high of 6.5%, possibly ending the year around 3% with minimal intervention.

Inflection points make for actionable signals.

The next CPI report for April 2022 will be released on May 11, 2022.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.