Earnings Review - December 3, 2022

Brief market commentary, portfolio company earnings results, and a deeper dive into Workday and CrowdStrike

The market continues to climb from the October lows. The S&P 500 closed above its 200-day moving average for the first time since April 7, 2022.

Jerome Powell’s speech on Wednesday, November 30, acted as a catalyst for the market.

“Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting.”

He seems to have eased his stance in comparison to prior communications, where he commented “pain for households and businesses” would be an unfortunate cost of reducing inflation.

The federal funds rate is currently at 3.75% - 4%. The market is now expecting a 50 bps increase in December, versus the 75 bps hikes which, although extreme when compared to prior tightening periods, seemed to have become the standard. Higher rates tend to act as gravity on equities.

A look at macroeconomic indicators can provide context as to why now.

The rapid clip of tightening has driven the yield-curve to invert. Typically longer-dated bonds will have higher duration (i.e. 5% yield if committing to 10 years, 2% yield if committing to 2 years). Today, shorter-dated bonds are paying more than long-dated bonds. Being a fundamental principle behind lending, this causes issues for the financial system. An inverted yield curve has often been a reliable signal of an impending recession.

Inflation seems to have peaked. There is a need for more data points to confirm, and there is a worry it can bounce back. But for now, things seem to be trending in the expected direction.

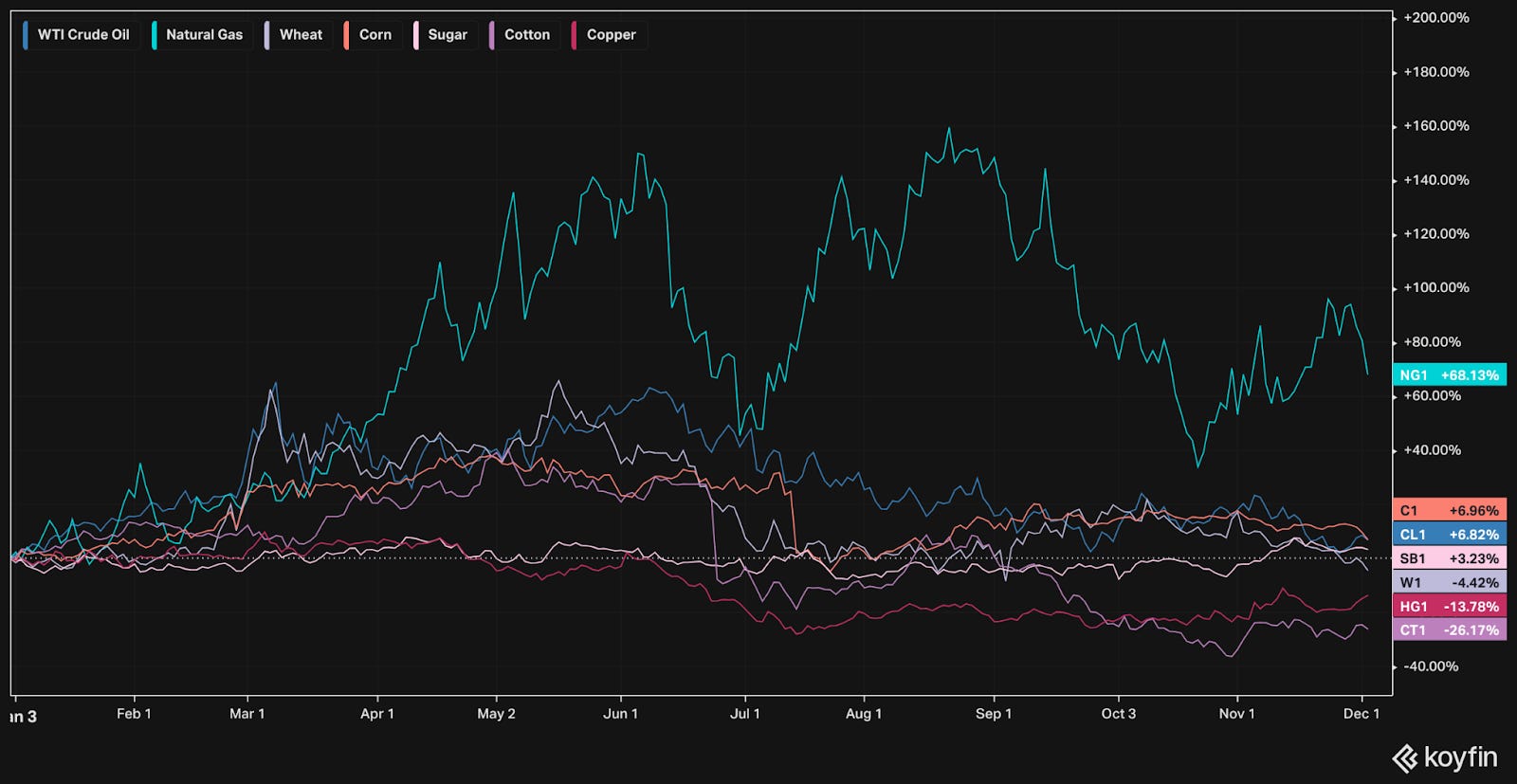

Commodity prices can give foresight into an element of inflation. Many commodities are trading near, even below, prices from the beginning of the year.

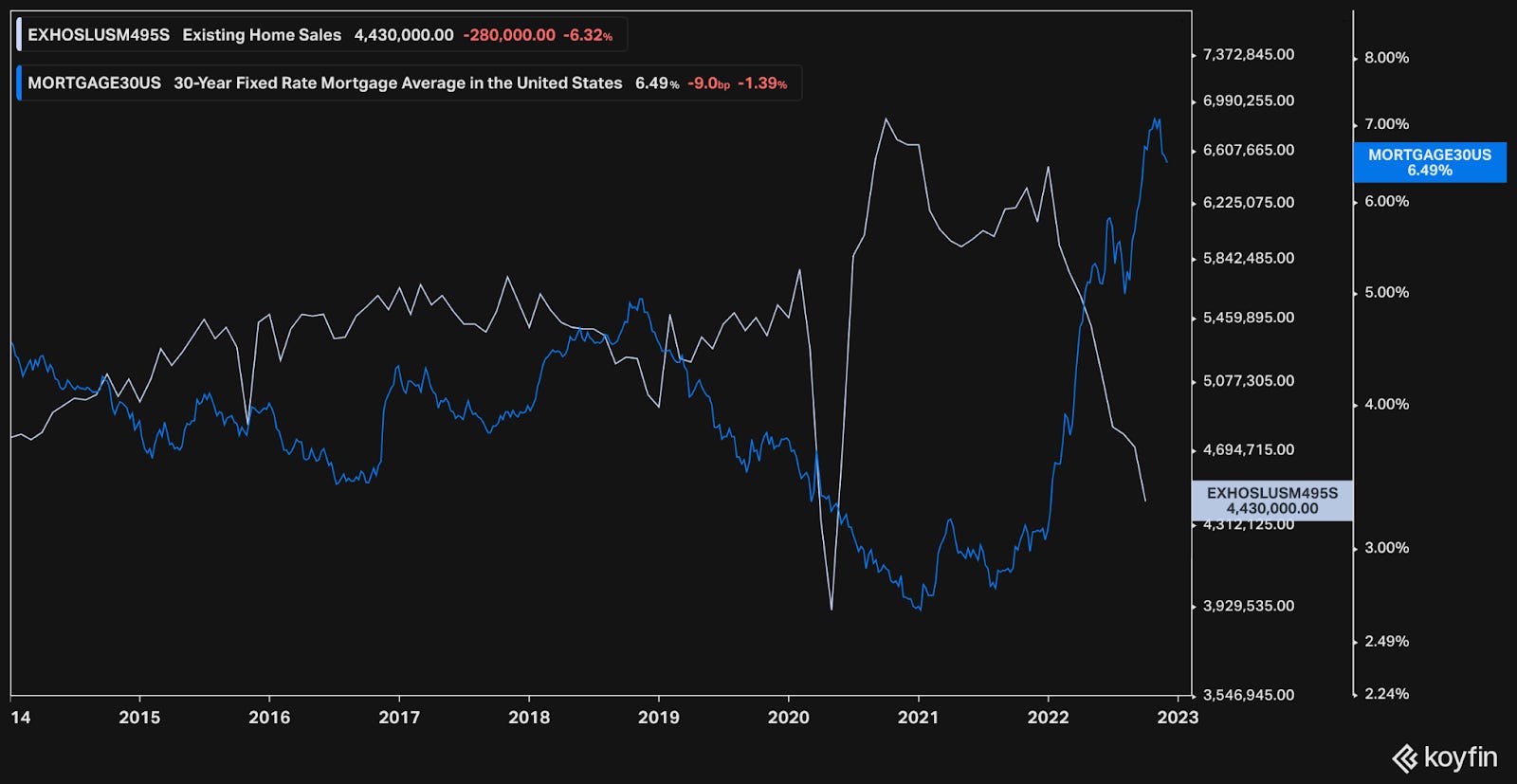

Mortgage rates have climbed with rates. Home sales have plummeted. As costs increase and there are fewer transactions, prices come down. While lagging, rent prices will follow.

While the job market remains active, jobless claims seem to be trending upwards.

CY Q3 2022 Results

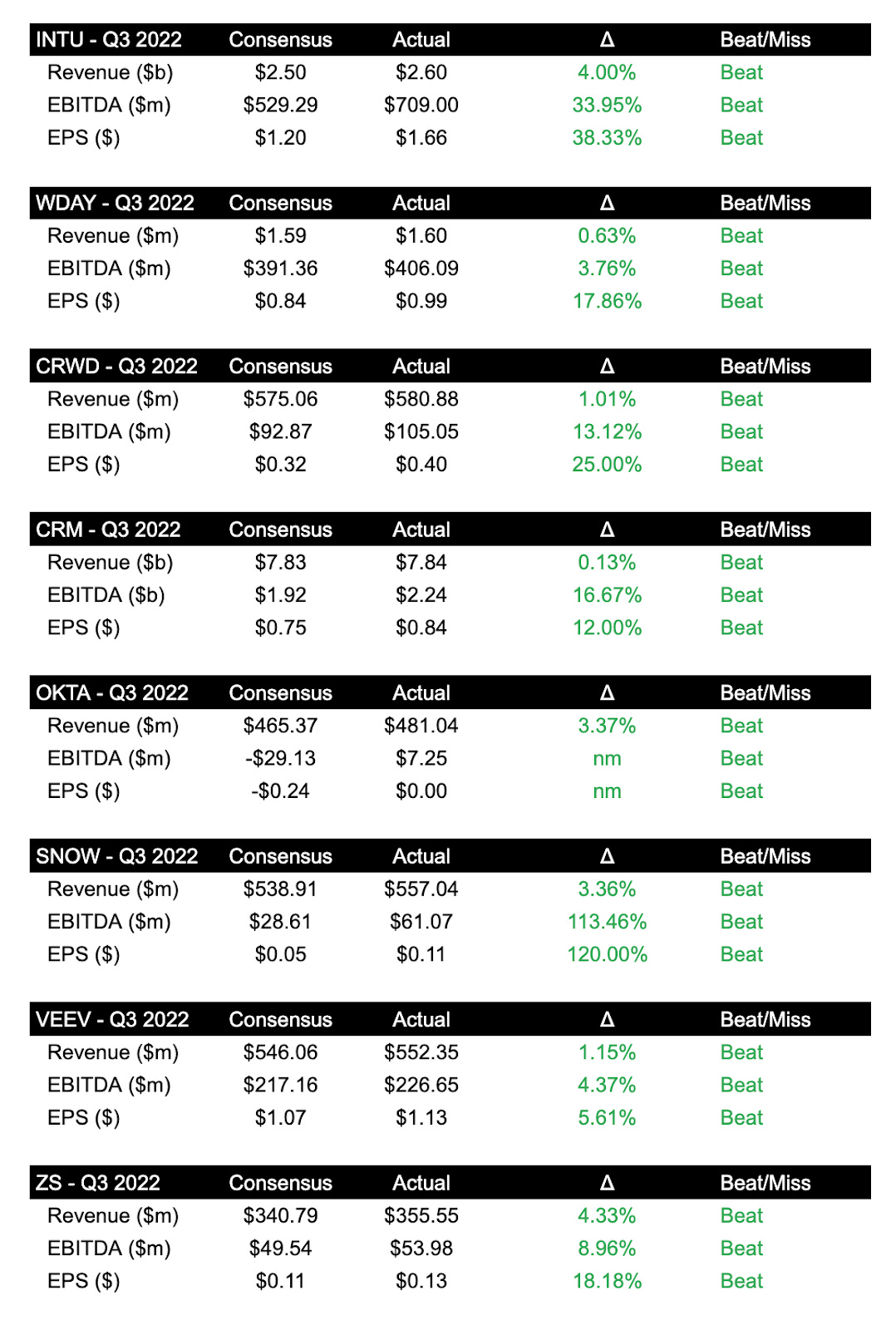

Over the last two weeks, eight portfolio companies reported earnings: Intuit, Workday, CrowdStrike, Salesforce, Okta, Snowflake, Veeva, and Zscaler.

Although results were positive across the board, market reactions were mixed. Markets are forward looking and therefore anchor strongly on guidance. I plan on incorporating guidance going forward. For now, a closer look into two companies.

Workday

From their 10-K:

“Workday is a leading provider of enterprise cloud applications for finance and human resources, helping customers adapt and thrive in a changing world. Workday provides more than 9,500 organizations with software-as-a-service solutions to help solve some of today’s most complex business challenges, including supporting and empowering their workforce, managing their finances and spend in an ever-changing environment, and planning for the unexpected.”

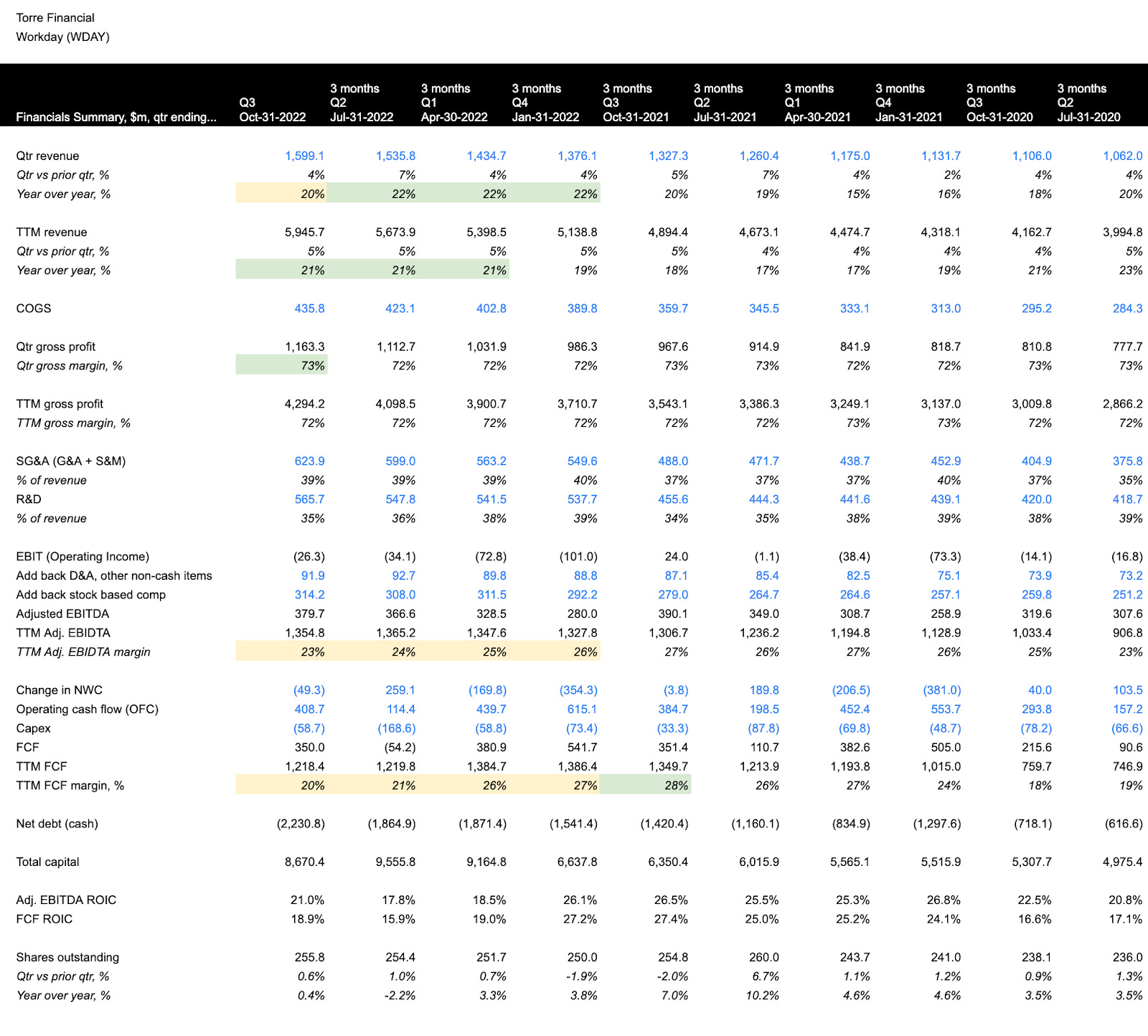

A summary of Workday’s financials is shown below.

A couple of call outs:

Revenue decelerated slightly to 20% year over year. Given the macro environment, however, this is strong performance.

Gross margins improved this quarter, up to 73% from 72% prior. This can be attributed to either pricing power and/or operational efficiencies.

Operating net working capital seems to fluctuate, although generally decreasing over time. This quarter they were able to improve working capital by $49.3 million, which flows through to FCF.

TTM FCF margins of 20% are healthy.

Dilution seems to be trending downwards. Year-over-year dilution (primarily due to stock based compensation) is only 0.4%. For the combination of 20% revenue growth, 20% FCF margins, and ~20% return on invested capital, the stock based compensation seems reasonable.

Workday has a strong balance sheet. They have accumulated cash over time, now holding $2.23 billion in net cash.

From the Q3 release:

Workday recently approved a $500 million buyback over the next 18 months. This represents 1.1% of the current market capitalization of $43.77 billion.

They narrowed guidance of subscription revenue for the year to $5.556 billion, representing 22% year over year growth. This is the top of the range presented at the beginning of the year.

Workday has been a steady performer, consistently exceeding expectations since the IPO. This level of predictability, coupled with the durability of their solutions, is a very strong trait.

CrowdStrike

From their 10-K:

“Founded in 2011, CrowdStrike reinvented cybersecurity for the cloud era and transformed the way cybersecurity is delivered and experienced by customers. When we started CrowdStrike, cyber attackers had an asymmetric advantage over legacy cybersecurity products that could not keep pace with the rapid changes in adversary tactics. We took a fundamentally different approach to solve this problem with the CrowdStrike Falcon platform – the first, true cloud-native platform capable of harnessing vast amounts of security and enterprise data to deliver highly modular solutions through a single lightweight agent. Our pioneering platform approach keeps customers ahead of attackers by automatically detecting and preventing threats to stop breaches.”

A summary of CrowdStrike’s financials is shown below.

Callouts:

Maintaining revenue growth at a very high clip, with sales growing 53% year-over-year. This is a deceleration from the prior growth rates, but that is expected as they continue to scale. Note they are growing fast off a large base, already with over $2 billion of annual revenue.

Gross margin came down slightly to 73%. This is a strong level, but it is important to watch as there are increasingly more and more competitors. CrowdStrike is the category leader and has been able to maintain strong pricing. SentinelOne is a fast-growing competitor that has been coming in with lower pricing.

EBITDA margins have improved consistently over time, from 7% in October 2020 to 19% in October 2022.

FCF margins have been even stronger, as CrowdStrike has been able to leverage their strong positioning to bring in cash upfront. Notice how the operating net working capital has decreased every quarter. They are managing their books superbly, essentially getting free financing.

Their balance sheet is strong, having accumulated cash to the tune of $2.46 billion.

Efficiency metrics, cash as a proportion to invested capital, are looking very healthy and continue to improve over time.

Dilution has been trending downwards as the company scales, also a good sign.

From their Q3 earnings release

CrowdStrike is guiding for Q4 revenue of $623.5 at the midpoint, implying a quarter-over-quarter growth rate of 7% and year-over-year growth of 45%.

In the earnings call, CEO George Kurtz mentioned the slowdown is due to a longer sales cycle given the uncertainty, not lost deals.

CrowdStrike has similarly demonstrated strong predictability and visibility into their business over time, exceeding expectations since IPO.

Closing

All asset classes have been under pressure from the rising rates. It seems the tide may be turning. The economy lags the market. While things may get worse in reality, the market may have already priced it in and moved beyond it. It is still too early to know if the market has passed the worst. I always find it helpful to stay focused on the business. While it may oscillate, the value created is eventually realized.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.