Market, Earnings, and Adobe (ADBE) - December 23, 2023

Market commentary, portfolio company earnings results, and a deeper look into Adobe (ADBE)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

The market has continued its upwards march. The SPY index is just a few points away from the all time high set in early January 2022.

Although new highs tend to make way for new heights, markets don’t go straight up forever. Since December 14th, the market appears to be in consolidation.

The Wyckoff Method of technical analysis identifies four phases: accumulation, markup, distribution, and markdown. The markup rapid ascent appears to be flattening out. It is possible we are at the distribution phase. Per the method, the next phase would be a markdown, or sell off.

Portfolio managers have been dressing up their portfolios, pushing up the winners to end the year.

Investors with unrealized gains are likely to hold off booking any gains until January.

From a probabilities-weighted perspective, a pullback in January seems more likely than not.

Year-to-date performance across indices:

Nasdaq +53%

S&P 500 +24%

Dow Jones +13%

Dow has hit an all time high. The S&P 500 and Nasdaq are within a few points. The indices have climbed out of a deep hole.

Momentum tends to build on itself in the market. As the saying goes, “strength begets strength.”

Strong markets tend to have relatively better forward returns in the short term (< 5 years) than the long term (10+ years). The inverse is true for bear markets.

The Magnificent 7 have driven the market higher.

NVDA +234% YTD

META+194% YTD

TSLA +105% YTD

AMZN +83% YTD

GOOGL +60% YTD

MSFT +58% YTD

AAPL +50% YTD

These 7 companies make up about 30% of the S&P 500’s market value. For more, see WSJ’s It’s the Magnificent Seven’s Market. The Other Stocks Are Just Living in It

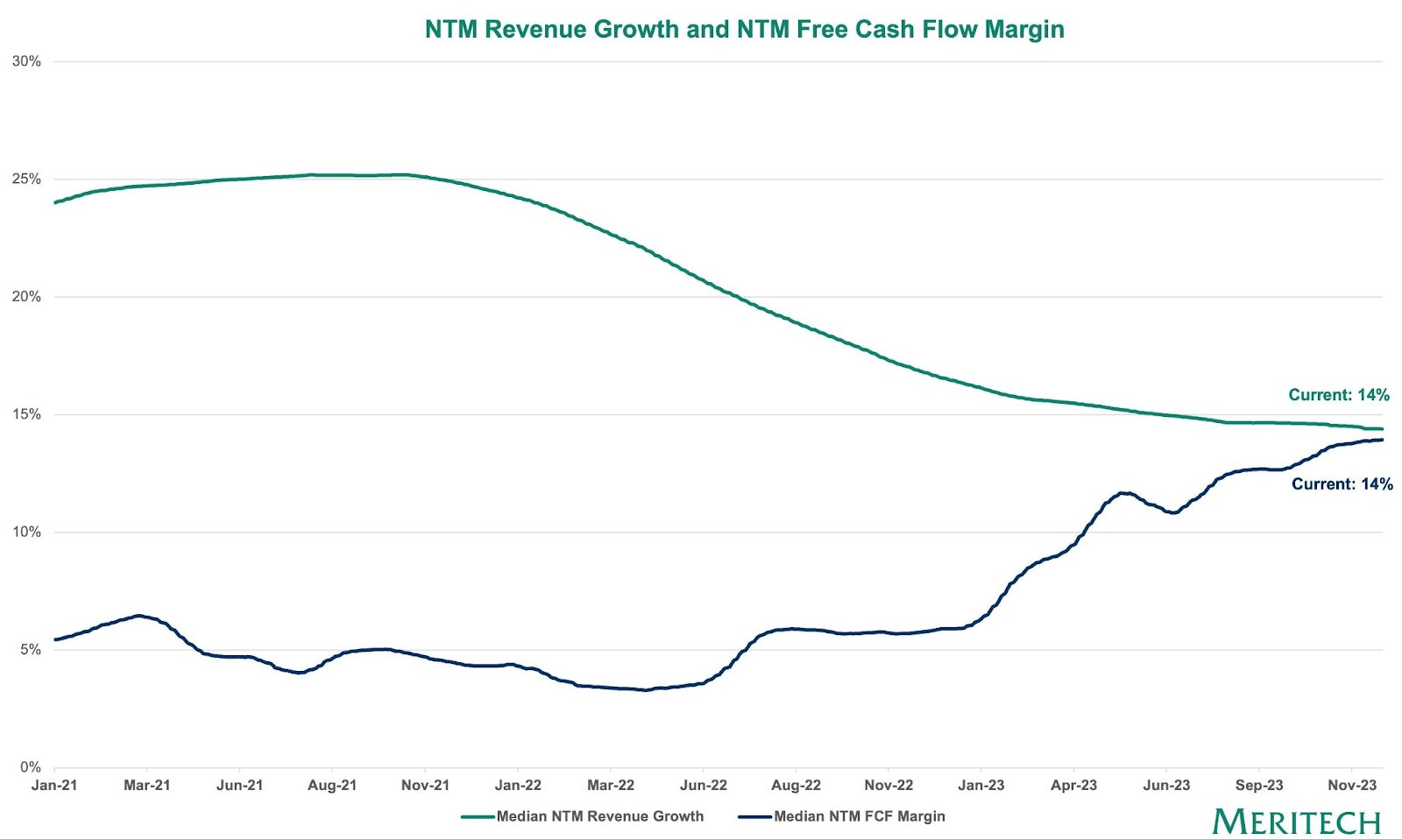

Software companies have benefitted from their rapid shift towards efficiency, trading growth for profitability. R&D spend primarily fuels enhancements and new products, i.e. future growth. Those expenses can be reduced at will. Forward growth rates have been nearly cut in half (from 25% to 14%), while forward free cash flow margins have nearly tripled (from ~5% to almost 15%).

These last two weeks brought large merger & acquisition (M&A) activity, including:

Japan’s Nippon Steel acquiring US Steel for $14.9 billion

Bristol Meyer Squibbs acquiring Karuna Therapeutics for $14 billion

Adobe and Figma mutually agreed to abandon the $20 billion acquisition after regulatory scrutiny (more on this below)

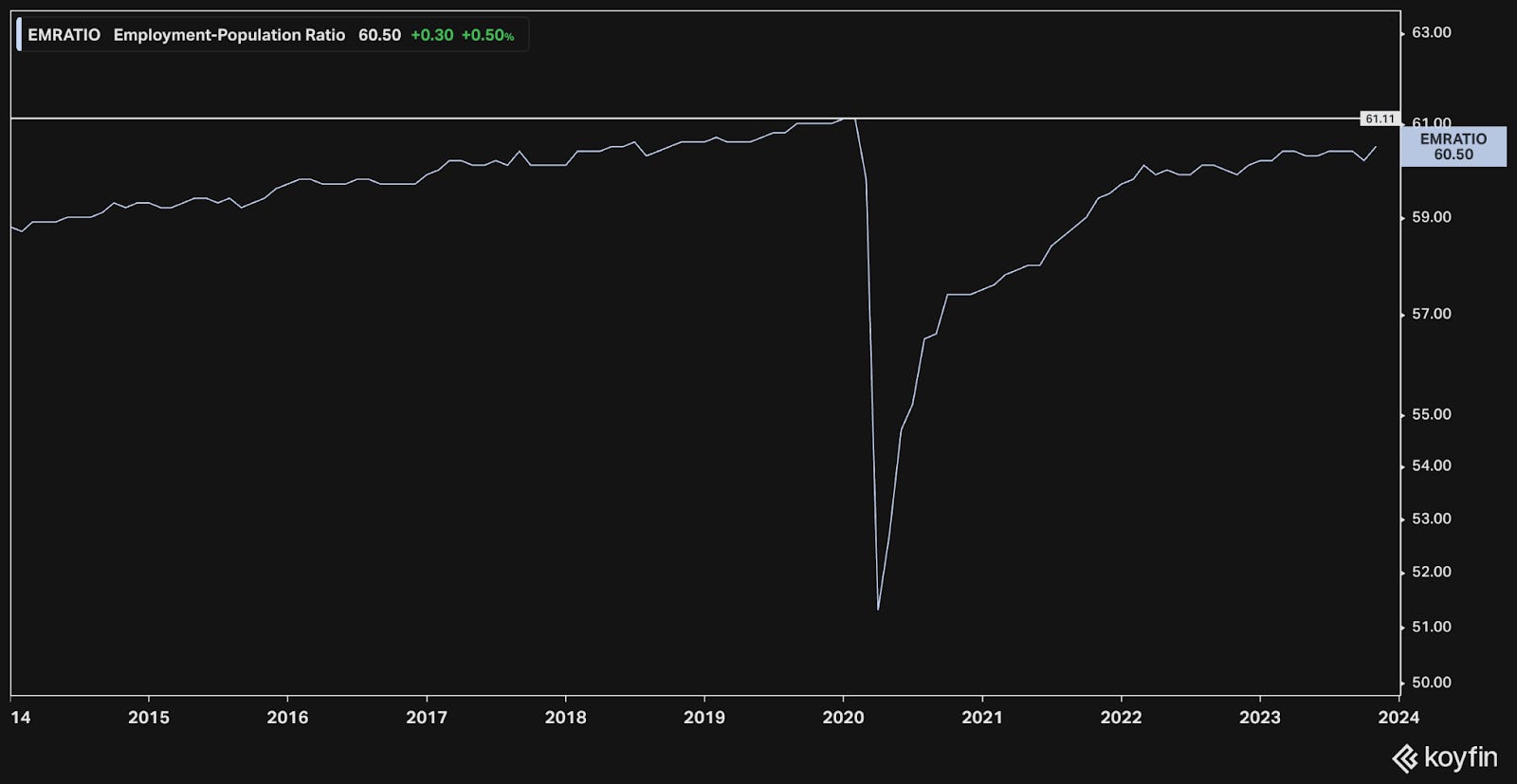

The economy has been holding up with steady employment and normalizing inflation.

The employment ratio of 60.50 continues to tick up, slowly recovering to the pre-covid high of 61.

Interestingly, healthcare accounts for roughly a third of the jobs created this year. Job growth in healthcare is accelerating, while other sectors are seeing declining growth rates.

Inflation is on its way down. The personal-consumption expenditures price index (PCE), the Fed’s preferred inflation measure, fell 0.1% in November versus September. Year over year, prices were up 2.6%.

The Fed has acknowledged the progress – and they have no desire to unnecessarily sacrifice jobs in the fight against inflation. The FOMC now expects to cut rates next year:

"If the economy evolves as projected, the median participant projects that the appropriate level of the federal funds rate will be 4.6 percent at the end of 2024, 3.6 percent at the end of 2025, and 2.9 percent at the end of 2026, still above the median longer-term rate."

- Jerome Powell, Federal Reserve Chair

The market expects the first rate cut in March.

Markets responded. Equities continued their climb. Yields have come down. The 10-year treasury peaked at 5% and has now been below 3.9%. Moves of this magnitude are rare in the bond market.

The USD, as measured by the DXY index, is declining. A weaker dollar benefits companies with international revenue exposure.

The volatility index (VIX), known as the fear gauge, is down and declining. A low VIX indicates market confidence. This VIX is at roughly 1.5 standard deviations from the mean, indicating an extreme level that only happens about 6.5% of the time.

Is this the calm before the storm?

Earnings

One portfolio company reported earnings over the last two weeks.

Adobe (ADBE)

Prior coverage: Market & Earnings Review - June 24, 2023

Adobe has emerged as one of the key leaders in the AI-race. They have built and released many generative solutions for creatives across image, video, modeling, and more to make creation more accessible and personalizable.

The current narrative is a dramatic turn from just a year ago, when the market was questioning Adobe’s moat.

At that time, Adobe announced the acquisition of Figma, a fast-growing collaborative design platform used primarily for software development.

During the rate increases and the dramatic decline of tech stocks, Adobe offered to acquire Figma for $20 billion, or 50x sales. Such a steep price, it was thought, could only be justified against an imminent threat to the model. Adobe shares declined 17% after the announcement.

Fast-forward to today – the two companies announced to mutually drop the acquisition after regulatory scrutiny. Adobe will be on the hook for the $1 billion termination fee.

It has been a journey, and likely still a positive outcome for Adobe.

For one, it must be a tough time for Figma employees. A few weeks ago many were banking on cashing in their equity compensation for a large sum. Many would-be millionaires missed out on the life changing moment, now likely many more years away (and at a lower multiple). It can be hard to work through this type of morale drain.

It also bought Adobe time to re-establish themselves as the leader in the creative space with the rapid release of many AI solutions.

The Adobe team is motivated and confident in their opportunities.

They continue to innovate, with notable areas of investment including:

Firefly, their generative AI engine

Integrating Firefly solutions across their Creative Cloud (ex. Photoshop Generative Fill and Expand; Illustrator Text to Vector, Adobe Express Text to Image, and much more)

Document Cloud – workflows to edit, share, review, and sign documents (i.e. competing with Docusign, which is rumored to be acquired be a PE firm)

Experience Cloud – analytics and marketing solutions to track and leverage the customer journey

From the last earnings call, CEO Shantanu Narayen commented:

“Adobe Creative Cloud, Document Cloud and Experience Cloud have become the foundation of digital experiences, starting with the moment of inspiration to the creation and development of content and media to the personalized delivery and activation across every channel. Adobe's mission of changing the world through personalized digital experiences and our delivery of foundational technology platforms set us up for the next decade of growth. We take pride in being one of the most inventive, diversified and profitable software companies in the world.

We believe that every massive technology shift offers generational opportunities to deliver new products and solutions to an ever-expanding set of customers. AI and generative AI is one such opportunity, and we have articulated how we intend to invest and differentiate across data, models and interfaces. We have delivered against this strategy and are pleased that a number of our groundbreaking innovations, including our Firefly models and integrations across Creative Cloud, Liquid Mode and integrations across Document Cloud and AI services in our real-time customer data platform and integrations in Experience Cloud are now seeing tremendous usage by customers.”

Diving into the financials:

Revenue growth stabilized in the 10-12% range, down from ~25% levels seen at the peak in 2021. The outlook for Q1 calls for continued 10% y/y growth. Steady is good – the key behind consistency.

Gross margins have been remarkably steady at 88%, having increased from 85% in pre-covid times. This is best-in-class.

EBITDA margins have held steady at 47-48% – again best-in-class levels.

Free cash flow margins are down to 36% vs a prior peak of 42%.

Cash conversion (EBITDA to OCF or FCF) has been weakening. This is something to keep an eye on. One primary reason for poor cash conversion is working capital – sales are not the same as collection.

The balance sheet is strong. Net cash is up to $4.2 billion, more than double from a year ago. Adobe had committed to a $1 billion termination in their offer for Figma – a likely outflow in the near future.

Shares outstanding are down 0.6% y/y. This is a much slower pace than a year ago, where share counts were decreasing almost 3% y/y. It is good to see shares still declining, and it is actually good that the pace has slowed. Presumably management is acting prudently, taking advantage of cheaper shares (a year ago) and buying back less when they are more expensive (now).

Return on capital metrics (EBITDA ROC and FCF ROC) are both very strong. The FCF ROC shows the same divergence due to the weaker cash conversion.

Adobe has been a consistent growth machine. Over the last 10 years, they have beat consensus estimates roughly 90% of the time. Only 5 quarters were misses, and those misses were very narrow (could even be called inline).

Adobe shares have been on a rollercoaster ride the last few years, similar to many other software companies. Shares declined 60% from the peak of $700 to the trough of $272 after the Figma acquisition was announced.

Since then, things have turned around significantly. Shares stabilized at the beginning of the year. After overcoming the trendlines at the golden cross, shares rocketed upwards. ADBE shares are up 78% YTD.

As for valuation:

Adobe trades for 25x EBITDA and has a trailing free cash flow yield of 2.6%. The valuation does not seem extreme – neither cheap, nor expensive for the quality of the business.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share reduction of 1%.

Analysts expect EBITDA to grow 10-12% through FY 2026. If that occurs, even with some multiple compression, ADBE shares could produce returns between 8-14% per year at current levels.

Fastgraphs provides another perspective on valuation. The FCF chart shows how the market has pulled forward some of the future growth. Annualized returns between 3-11% are possible over the next few years if shares trade between 25x (magenta) and 31x (blue) P/FCF.

Closing thoughts

This year’s rally caught many investors and financial advisors off guard. The late-year rally is certainly fueled by many professional investors playing catch up, trying to position their portfolios for the end of the year. Those that have been invested are likely holding off any gains until 2024. It would not be surprising to see the market pullback in January after such a long run up.

At Torre Financial, we look to bring in any and all the signals we can into our decision making. Macro and or other high level data about the economy can certainly inform our portfolio positioning. While we do not know what the market will do for certain, we can leverage these insights to understand underlying drivers, motivation behind market participants, supply and demand, as well as second- and third-order impacts.

That being said, we have a strong preference to always stay primarily invested. We invest bottoms up, identifying opportunities through solid businesses at attractive valuations. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

Investing is all about making probability-weighted decisions.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.