Market, Earnings, and American Tower (AMT) - April 13, 2024

Market commentary, portfolio company earnings results, and a deeper look into American Tower Corporation (AMT)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

In our last review on March 16th, we mentioned it would be prudent to expect a pullback. Since then, the market climbed nearly 3% before giving up those gains. The index now at 510.8 is just one point above the 509.8 close on March 15.

The 50-day simple moving average was breached on Friday during intraday trading. This is the first time the index traded below the trendline since November 2023.

This trendline can possibly turn into support, in which case the market could rocket higher. On the flip side, if the price breaches decisively, it could lead to more selling.

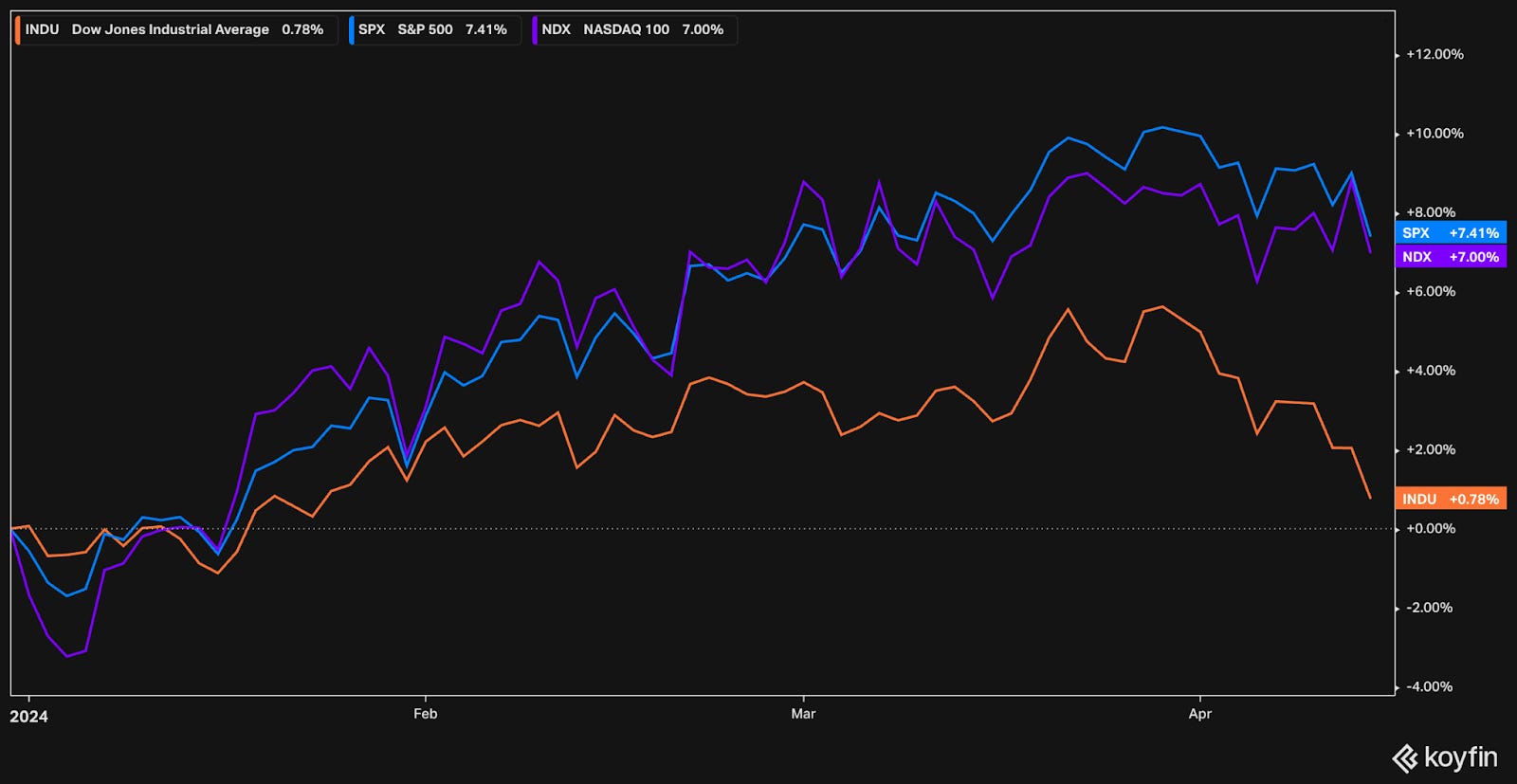

Year-to-date performance across indices:

S&P 500 +7.4%

Nasdaq +7.0%

Dow Jones +0.8%

The S&P index appears stretched based on historical measures. Currently trading for nearly 25x P/FCF, the index has infrequently reached such heights. When it did, the price didn’t hold for long — potentially a harbinger of a further sell off, particularly when coupled with a decline in FCF.

For a different perspective, EV/S and EV/EBITDA multiples are near all-time highs, while the FCF yield is near an all-time low.

Our TF portfolio exhibits stronger revenue growth, FCF margins, less leverage, and trades at a cheaper valuation.

S&P’s top performers year-to-date (YTD) include many chip companies such as SMCI (+216%), Nvidia (+78%), and Applied Materials (+28%) as well as other well-known names like Meta (+45%), Netflix (+28), and Disney (+26%).

There’s also a strong showing from energy names – NRG Energy (+43), Marathon Petroleum (+41), and Valero Energy (+33%).

The bottom performer YTD list includes Boeing (-35%), Lululemon (-34%), Charter Communications (-33%), Walgreens (-32%), Tesla (-31%), and Adobe (-21%).

Growth and value have moved at a nearly-perfect-inverse correlation with each other.

The latest CPI result came out on March 10th. March CPI came in at +3.5% year-over-year vs expectations of +3.4%. The last mile from 3% down to the 2% target seems to be more challenging than expected.

These readings continue to shift rate cut expectations further out.

As of the beginning of the year, the expectation was that rates would come down from 5.3% to 3.6% by the end of the year.

As of today, expectations are for the 5.3% rate to come down to just 4.84%.

The market has been wrong on the expectations in the past. Could inflation come down quicker than expected?

One major component of CPI is shelter, which lags the market by roughly 1.5 years when considering peak-to-peak levels.

Substituting in a real-time shelter index in the CPI calculation would result in CPI coming down to 1.9%, vs. the 3.5% published number.

Truflation, a real-time inflation measurement, also reports inflation below 2%.

Only time will tell.

Earnings

Earning season was unofficially kicked off on Friday with the big banks beginning to report Q1 results.

No portfolio companies reported earnings over the last 4 weeks.

American Tower Corporation (AMT) – Initial Coverage

American Tower Corporation was founded in 1995 as a subsidiary of American Radio. In 1998, American Radio merged with CBS and American Tower was spun-off as a separate company.

A quick snippet of history gives insights into American Tower’s origin.

AT&T Long Lines, which provided long-distance services, had originally started with wire and cable, using coaxial links to connect major cities in the USA. By the 1960s, these connections transitioned to microwave radio relays, which required towers.

By the 1980s, alternatives such as fiber optics and satellites eventually replaced the microwave system. AT&T had no use for the towers. The microwave relay program was decommissioned in 1980.

American Tower began purchasing microwave telephone relay towers from AT&T as early as 2000.

They began repurposing the towers as cell towers and leased antenna space to cell phone providers.

Today, American Tower has a global portfolio of over 224,000 communication sites. It is one of, if not the, largest tower companies in the world.

Their powerful business model allows significant efficiencies through multi-tenancy.

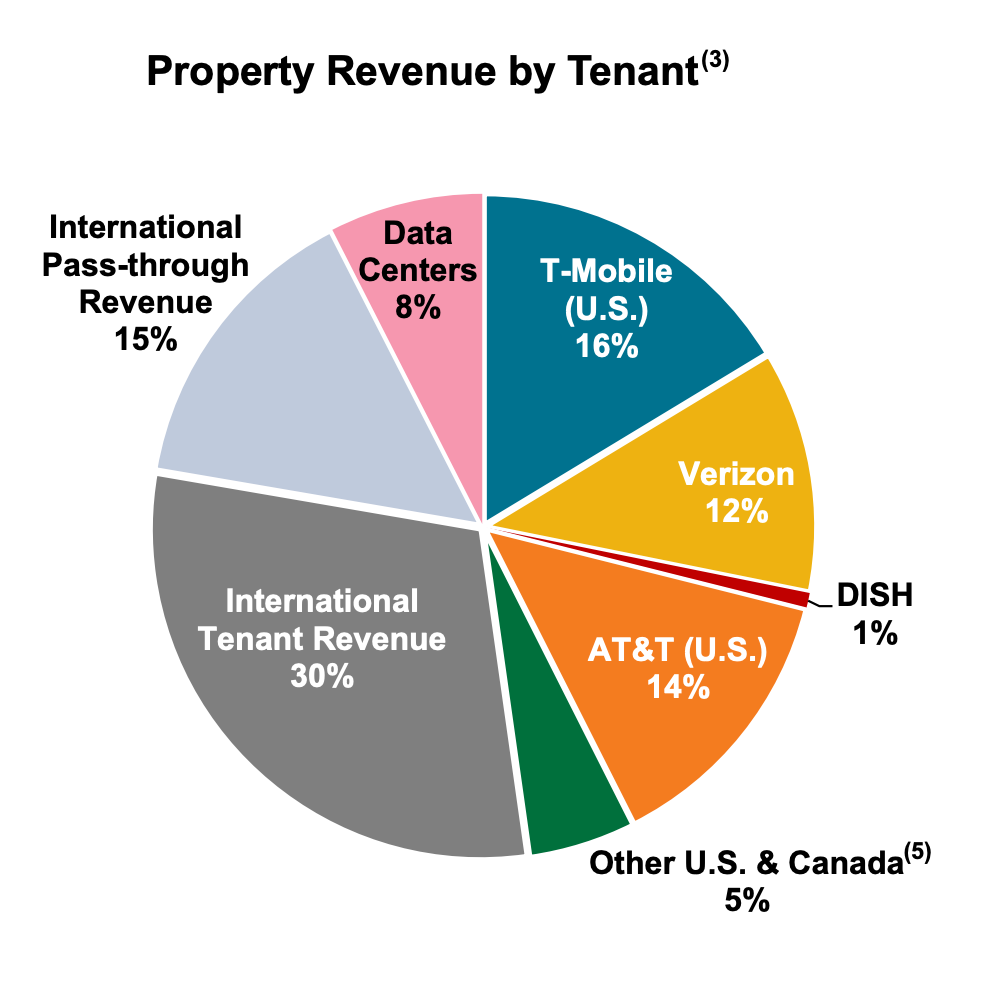

The major telecommunications companies make up 42% of their revenue, with another 30% coming from international tenants.

The infrastructure that American Tower provides is critical to today’s world, considering the dependency on smartphones and the proliferation of internet-of-things.

Demand is strong and growing. Cellular data usage is expected to grow at 20% CAGR through 2028 at least.

The evolution of cellular networks, such as from 4G to 5G, are monetization opportunities for American Tower as cell phone providers add new antennas and other hardware to the towers.

New technologies such as satellite and Wi-Fi connections complement, but will not replace cellular towers. Satellite is widely available, but has inherent limitations with latency. Signals must travel a long distance (to outer space!) and back. This limits many applications that require low latency connections. Wi-Fi provides much smaller coverage and doesn’t use licensed spectrums.

American Tower has very long-term tenant leases, typically non-cancellable with terms of 5-10 years. They embedded annual escalators, typically around 3% in the USA and variable in international markets. Churn is historically very low at 1-2%.

Over the last decade, American Tower has generated a return on invested capital (ROIC) between 9-10%. The portfolio has grown significantly over this time, almost tripling revenue. They have been able to maintain their high hurdle rate with attractive re-investment opportunities, whether through in-house development or acquisition. Over the very long-term, stock returns are likely to resemble a company’s ROIC.

Note that many international contracts have “pass through” expenses, where certain costs are passed on to customers. This increases revenue but with 100% costs, watering down margins and other metrics in financial analysis. About 15% of revenue is passed through.

The company has a long runway for growth. From upgrading existing towers to building out portfolios in emerging markets, they likely have decades to continue expanding their core business.

Additionally, American Tower recently acquired CoreSite, a data center REIT, as another strategic growth play. They are explicit about not going after the hyperscale data center market. Rather, they are using this acquisition as entry into complementing their towers with edge computing solutions. This is a new, very promising area with many high profile players including Cloudflare, Zscaler, Google Cloud, Amazon Web Services, and many more. It is all about reducing latency by having the software execute closer to the end consumer.

Management is very shareholder friendly, runs a conservative balance sheet, applies rigor looking for highest risk-adjusted returns on all investment decisions, and has demonstrated to be forward-thinking.

REITs have been under pressure due to the higher interest rate environment, and American Tower is no exception. REITs are often seen as an income source, and hence sensitive to alternative options such as money market funds. Additionally, they are capital-intensive, often looking to develop or acquire. Higher rates lead to a higher cost of capital, which increases the hurdle rate for new investments, ultimately making growth harder to come by. Rates will always oscillate.

American Tower is a compelling opportunity with durable, long-term, secular growth opportunities; strong competitive advantages due to partnerships, scale, systems, and expertise; and they have demonstrated their ability to generate consistently high returns on capital.

Diving into the financials:

TTM revenue ticked down to 3%, slowing the last few years after peaking at 20%. The peak was in part due to the CoreSite acquisition. While the slowdown can be concerning, we have strong conviction in the long-term opportunity and expect growth to return in the future. As discussed, high rates make growth more difficult to come by.

TTM gross margin ticked up to 71%, having expanded recently. The company has mentioned a focus on improving internal efficiency, leveraging AI for operations amongst other efforts.

TTM EBITDA is strong at 64%

TTM FCF margins came in at 42%, oscillate quite a bit due to cash acquisitions

Net debt / TTM EBITDA ticked down to 5.2x, coming down from a peak of 6.9x. Management has been very clear about their focus to get their debt below 5x to always have a strong balance sheet. Below 5x is a very strong bar for REITs.

Shares outstanding are stable. In the past, there has been up to 2-3% y/y dilution, likely related to acquisitions.

EBITDA and FCF ROC are healthy at 12% and 8% respectively.

→ It is important to recall that all of these financials are impacted by the 15% pass through revenue. This inflates revenue and expenses, effectively watering down margins and efficiencies. As a simple example, consider generating $10 in FCF. With $100 in revenue, that yields a 10% margin. With $115 in revenue, that yields a 8.6% margin.

AMT has been in a pretty clear bear market over the last 3 years, with the stock declining 18.6% as interest rates have pressured the business and the broader industry. October 2023 brought strong interest. The 50-day moving average crossed above the 200-day moving average (“golden cross”) in December 2023. More recently, shares sold off as the price breached below the 200-day moving average. It would be a bullish indicator if shares climb back and maintain the 50-day SMA above the 200-day SMA.

As for valuation:

American Tower has an enterprise value of $120 billion.

EV/NTM EBITDA of 17x is very reasonable for such a high quality company with decades of growth opportunities.

The FCF yield of 3.9% is reasonable, again considering the growth opportunity. The 10 year treasury, typically the risk-free alternative, yields 4.5%. The yield on treasuries would not grow over time.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 0.5%.

Over the next 5 years, assuming an ending multiple of 18x and modest revenue growth of 4%, shares could return 8% per year from today’s price of $179.

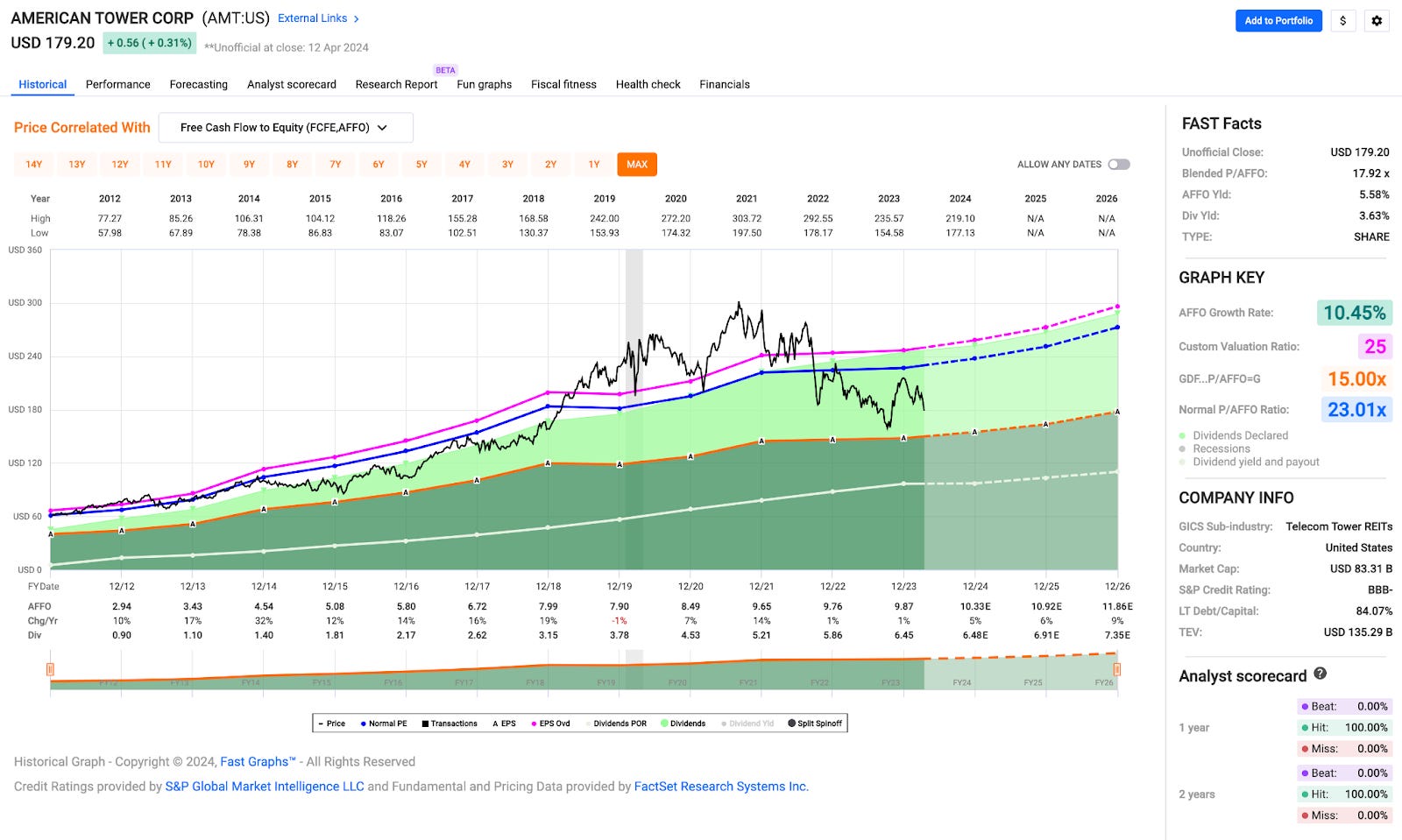

For another perspective, take Fast Graphs.

The valuation has clearly come down, with the stock currently fetching a P/AFFO multiple of 17.9x.

If shares were to re-rate to their historical average P/AFFO of 23x, AMT could return almost 20% annualized.

Closing

The market overall is looking a bit stretched. There’s been a big run up the last 6 months and the market is ever more concentrated in the largest companies.

Notwithstanding, we remain steadfast in our commitment to stay invested for the long term. Over time, the market increases. At the same time, we try to make the best probability-weighted decisions we can at all times.

We’ve mentioned in previous quarterly letters our desire to add stability to our portfolio – a new company that could help diversify and lower volatility. We looked at consumer staples and even energy companies. We were not content with the premium valuations for such low and limited growth opportunities in consumer staples. We were not content with the cyclicality and lack of pricing power in energy. The cost-benefit analysis did not justify a place in the portfolio.

Then we came across American Tower Corporation. After doing a deep dive and monitoring it closely, we found it satisfied a lot of our criteria. It offers stable, recurring cash flows; it has very low or inverse correlation to other positions; secular long-term trends with growing demand; and much more. Additionally, the price has come down to very attractive levels on a historical basis.

A durable, profitable business with a long runway for growth can be a significant source of wealth, as it compounds year after year.

At Torre Financial, we focus on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We assess primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Torre Financial is an independent investment advisory firm focused on companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.