Market, Earnings, and CrowdStrike (CRWD) - March 16, 2024

Market commentary, portfolio company earnings results, and a deeper look into CrowdStrike (CRWD)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

The S&P has posted gains in 17 of the last 20 weeks. The bull-market backdrop is strong, as AI-stocks and momentum push the market higher. This march higher has been undeterred since its start in late October.

Volatility has increased over the last few weeks. Down days have been stronger and more frequent. Buyers have continued to step up, so far.

The chart shows some consolidation in the 505-515 range. The market closed out on a weak note.

Markets don’t go up and to the right forever. It would be prudent to expect a pullback.

Year-to-date performance across indices:

Nasdaq +5.8%

S&P 500 +7.3%

Dow Jones +2.7%

The VIX Volatility Index is still at a historically low and relatively calm level, 14.4. It appears to be increasing slowly and steadily over time, forming an upwards channel. Higher volatility corresponds to a higher probability of a declining market, while lower volatility corresponds to a higher probability of a rising market.

The Magnificent 7 continue to push higher, mostly.

Apple, Tesla, and Alphabet have slowed down this year, with -34%, -10%, and +1% returns YTD. Could these be early signs of rotation out?

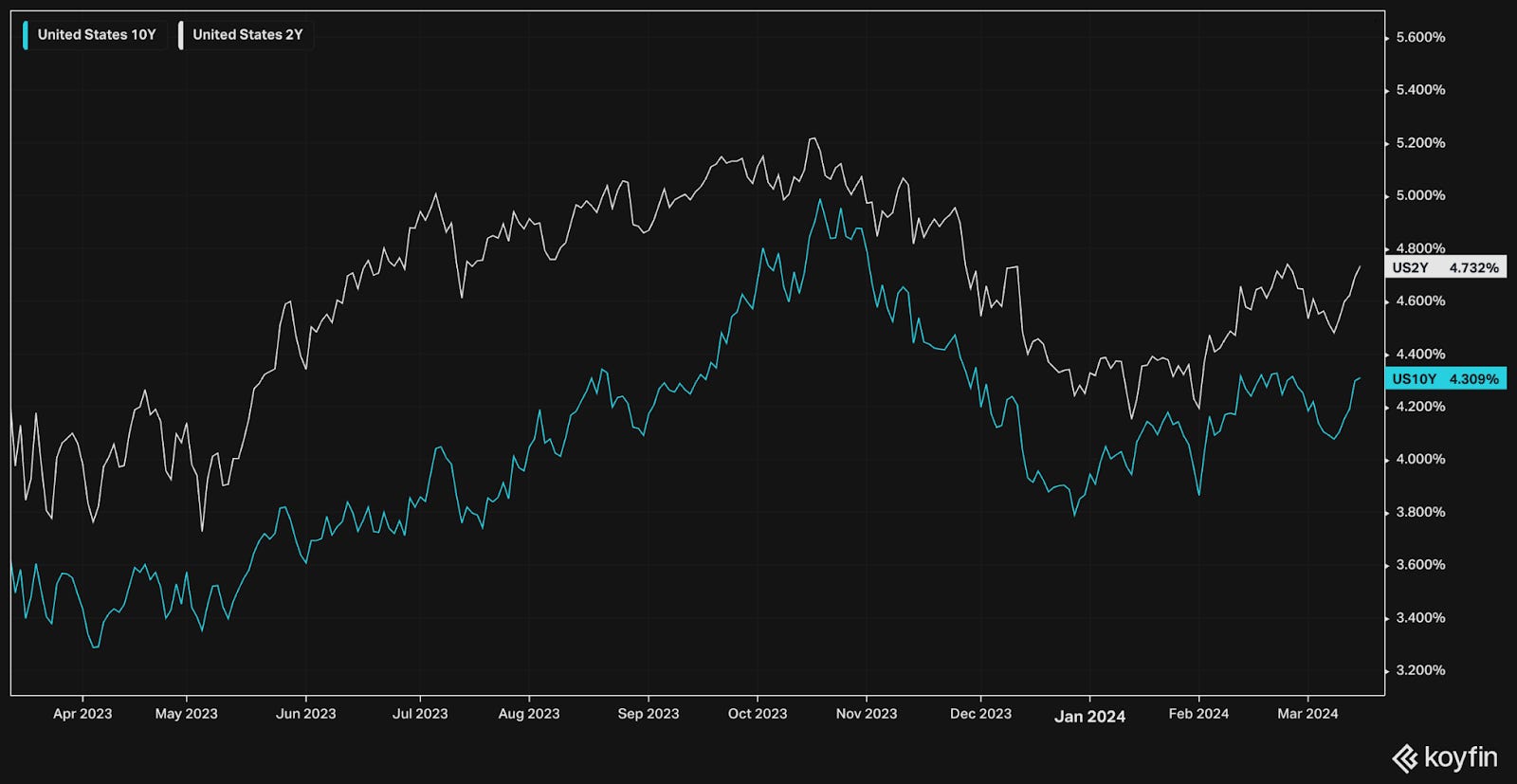

The 2y-10y curve has now been inverted for over 421 consecutive trading days, surpassing the 1978-1980 inversion for the longest period ever.

The 2-year yield trades at 4.7% while the 10-year yield goes for 4.3%

Market’s expectations for a rate cut continue to be pushed out into the future. There are loose expectations for the first rate cut to come in the summer.

In our article on December 23rd, just 3 months ago, the market had strong conviction that a rate cut would be coming on March 20th with probabilities of 75.6%.

Market expectations can be helpful directionally – more likely rates will come down next, and not up. Timing, however, is difficult for anyone to know in advance. Higher for longer has proven true thus far.

Earnings

Over the last two weeks, 2 portfolio companies reported earnings.

CrowdStrike (CRWD)

Prior coverage:

CrowdStrike (CRWD) - initial coverage, July 2020, share price ~$100

Market & Earnings Review - March 18, 2023 - share price ~$133

Market, Earnings, and CRWD - September 2, 2023 - share price ~$161

CrowdStrike has been an emerging leader in the cybersecurity space. The company has been very successful in scaling and expanding their portfolio of offerings.

While they have been typically seen as an upstart challenger, they are now directly challenging Palo Alto Networks for the leading spot.

CrowdStrike’s story illuminates a valuable investing lesson about the fruits of high-quality companies.

CrowdStrike first sold shares to the public in June 2019, pricing their IPO at $34.

Shares surged to close the day out above $63.

We had been interested and tracking the company for a while, but weary of the typical IPO hype.

We finally initiated a position in May 2020, picking up shares between $72-76.

Our first article on CrowdStrike was published in July 2020. Shares were trading at ~$100. Even though shares had nearly tripled since the IPO, we projected CrowdStrike still offered a compelling investment opportunity:

“[Projecting] 5 years out, we [could expect] roughly $1.5 billion in operating earnings with a 30x multiple. The estimated valuation for CRWD would be $45 billion. This is in comparison to today’s market cap of $21.8 billion, or roughly a CAGR of over 16%.”

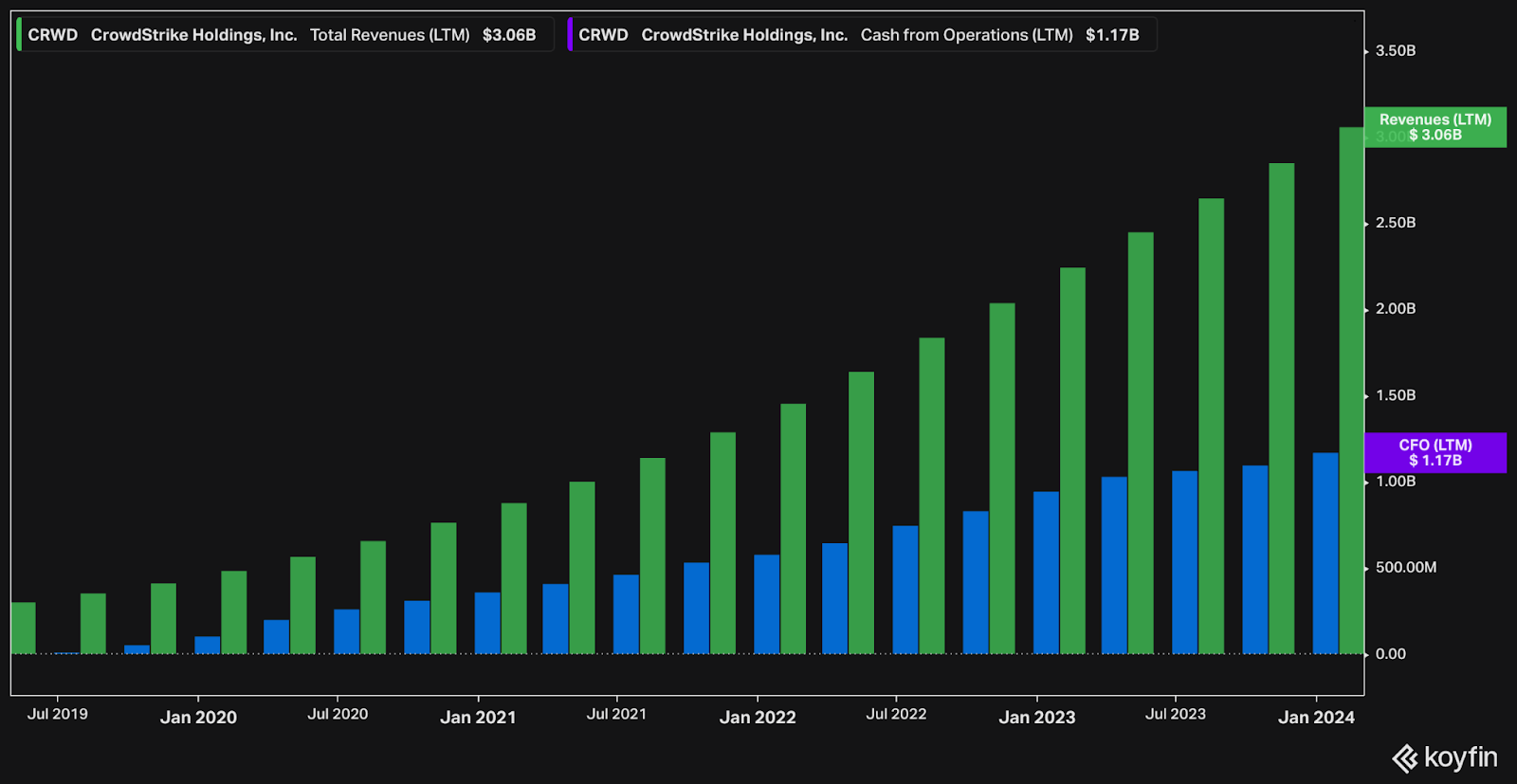

Today:

Revenue is up to $3 billion, from $0.65 billion

Operating cash flow is up to $1.2 billion, from $0.26 billion

CrowdStrike’s market cap is closer to $77.5 billion, up from $21.8 billion

Shares are up over 300% since our initial purchase, for a CAGR of 45.85%. Although, it has been a volatile ride with COVID, post-COVID boom, post-COVID bust…

CrowdStrike certainly seemed expensive when we first invested. Shares were going for a market cap of more than $20 billion – with only $650 million in LTM revenue! 30x LTM revenue, or 20x NTM revenue – these are high multiples on revenue!

Yet, markets are savvy. They price in the future – not the past.

Over these last 4 years, CrowdStrike …

Grew revenue by almost 5x

Grew operating cash by nearly 6x

And the share price roughly 4x’d

The fundamentals (revenue, operating cash) outgrew the share price indicating compression in the multiple. Even so, CrowdStrike has been a very strong performer.

Investing in high quality companies can pay off. The risk is in the unknown future. If things falter while trading for a significant premium, it could get ugly. If things move along smoothly, a fast growing company can create significant value.

Diving into the financials:

Revenue growth came in at 36% y/y. While that looks to be declining, they are holding strong in the 30s. Very few companies have been able to maintain this kind of growth on the back of very strong comps in the prior year.

Gross margins of 75% are holding impressively steady, and have increased over the years from 74%. This is a strong positive. In the past there were worries that competitors such as SentinelOne were undercutting on price, which could lead to discounting or other pricing pressure. CrowdStrike appears to be holding strong there.

EBITDA margins are up to 24%. They have been significantly improving every quarter.

FCF margins are steady at 32%. These have slowly come down over time, from a recent peak of 35%. This divergence between EBITDA and FCF is quite odd. Possible explanations would be a shift in employee compensation to be more cash and less stock-based compensation. Another would be a decline in percent of customers paying upfront – i.e. sales are exceeding cash collection. It cannot be too significant since FCF margins have not come down too much.

Balance sheet is strong, with nearly 3.5 billion in cash and very little debt.

Share dilution has ticked up to 2.5% y/y. This is certainly on the higher end, and we wouldn’t like to see it go much higher than this. That being said, so are the fundamentals. The combination of high growth in the 30s and these profitability margins also in the high 20-30s does make it worthwhile.

Efficiency ratios are strong with EBITDA return on capital of nearly 24% and FCF return on capital of nearly 32%.

The last few years have been volatile for CrowdStrike, yet the fundamentals have been strong and eventually gained the respect of the market.

Over the last 3 years, CRWD is up nearly 60%, exceeding both the Nasdaq’s +21% and the S&P 500’s +35%.

As for valuation:

CrowdStrike has an enterprise value of $73.6 billion.

With NTM revenue estimates of $3.97 billion, it is currently trading for a hefty 18.5x revenue multiple. This is quite a premium. The EV/NTM EBITDA of 72x doesn’t look much better.

As discussed above, multiples in-and-of-themselves do not determine what makes a good investment. Multiples are simply a proxy valuation, and used to compare against other companies in the market. Not many other companies have the growth, profitability, and efficiency of CrowdStrike.

The FCF yield of 1.3% is quite low, even with the 30%+ growth. Assuming 50% growth to FCF, it would take 3 years to get to a FCF yield comparable to the current risk-free rate.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 2.5%, in an effort to be conservative.

Analysts expect revenue growth of 30%, 26%, and 26% over the next three years. Shares currently trade at 18.5x NTM Revenue.

Over the next 5 years, assuming multiple compression down to 14x and more conservative revenue growth of 20%, shares could return 10% per year from today’s price of $315.

Closing

Markets don’t go up forever. We’ve been cautiously optimistic this year and have stayed invested throughout. Recently we’ve been lightening up a bit as we see the market stretching to the upside. Investing decisions are all based on probabilities. A pullback seems more likely than not at this point.

As for high-quality companies – the best will likely always seem expensive. Amazon, Google, and many others seemed extremely expensive during their most formative years.

By taking a business owner perspective – focusing on business itself, the industry, secular tailwinds, competition, demand, fundamentals, management’s decisions, etc – investors can get insight into the quality. A durable, profitable business with a long runway for growth can be a significant source of wealth, as it compounds year after year.

On the flip side, premium-priced companies do face real risks. If things don’t go as planned, the downside can be significant. It is important to keep this in mind!

At Torre Financial, we focus on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Federico Torre

Torre Financial

federico@torrefinancial.com

Torre Financial is an independent investment advisory firm focused on companies with high return on capital, competitive advantages, and durable growth.

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

It has nothing to do with quality companies and 90% to do with a new industry being born..it isn't clear there won't be setbacks. One should take profits when margin of safety goes negative!