Market, Earnings, & Booking Holdings (BKNG) - March 2, 2024

Market commentary, portfolio company earnings results, and a deeper look into Booking Holdings (BKNG)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

The technical picture has not changed much as the market continues its uninterrupted climb.

The S&P 500 made another new all time high and closed above 5,100.

The Nasdaq made a new all-time high on Friday, surpassing its 2021 record, on the back of the AI boom. Nvidia’s strong earnings released on February 21st seemed to have propelled the whole market forward.

Things are good. The market is calm and steady. On the other hand, valuations are getting stretched. The market is overbought.

Momentum can be a powerful force in the market. It is important to respect the price movement. At the same time, markets do not go up forever. It would seem reasonable to be prepared for a pullback.

Year-to-date performance across indices:

Nasdaq +8.8%

S&P 500 +7.7%

Dow Jones +3.7%

Analyzing performance by sector can help better understand trends and identify opportunities.

Over the last 3 years:

Over the last year:

YTD (January & February):

Some insights:

Over the last 3 years, Energy is the clear winner with a huge move up starting in late 2021.

Looking over the last 3 years, as of January 2023, the worst performing sectors were Communications, Consumer Discretionary, and Technology. Over the last year, starting soon after January 2023, the best performing sectors are Technology, Communications, and Consumer Discretionary. There was a clear change in leadership.

Over the last year, the 3 worst performers are Utilities, Consumer Staples, and Real Estate. Looking at YTD sector performance, those are still the 3 worst performers. It doesn’t seem like there has been an inflection quite yet, but something to keep an eye on. It can be worth looking into these for investment opportunities.

Healthcare is in the middle of the pack in both 3-year and 1-year lookbacks. YTD, however, Healthcare has been a leader. The sector could be well poised for continued growth.

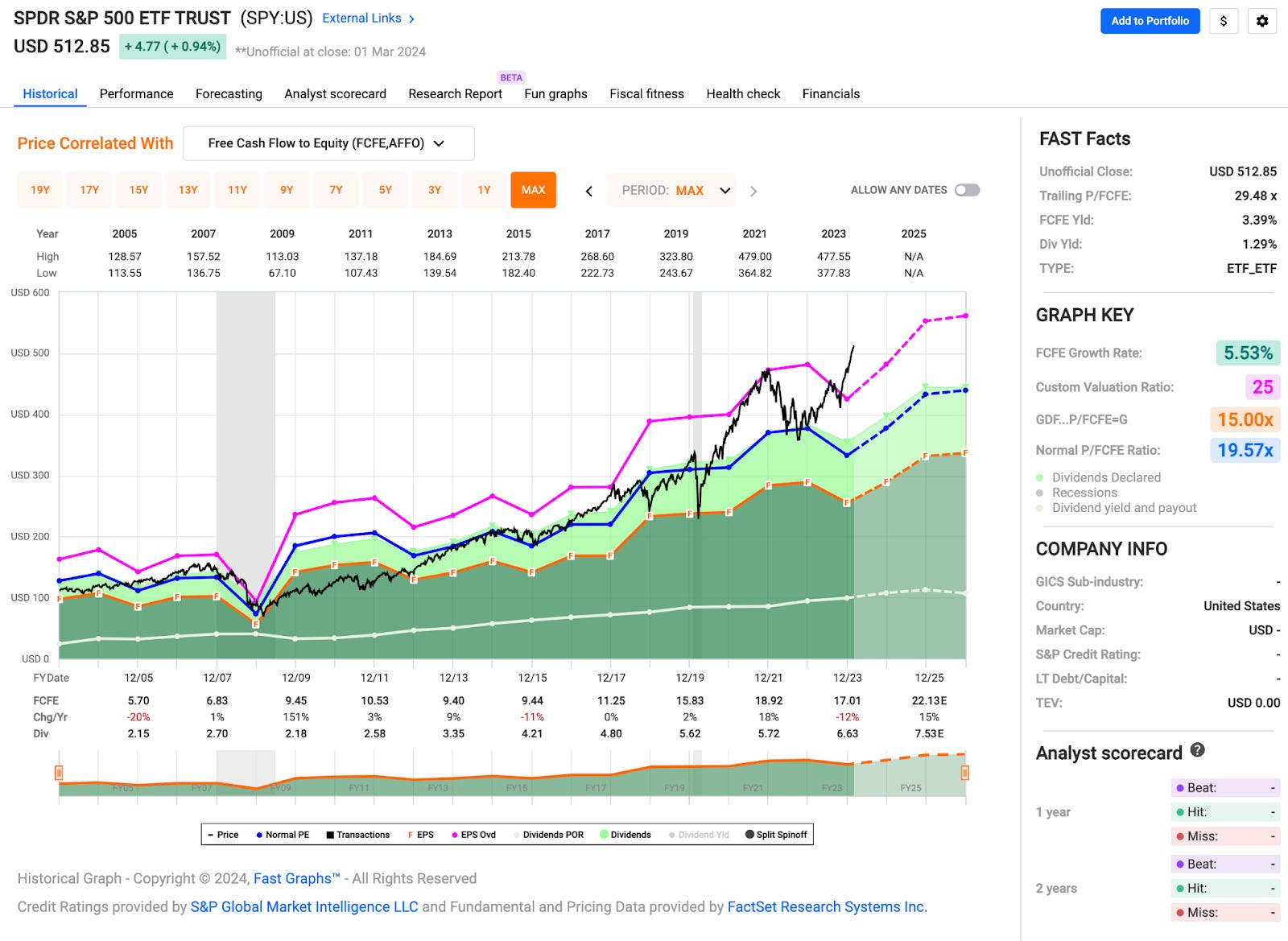

Overall, the stock market appears to be expensive.

The SPY currently trades for 29.5x P/FCF compared to a historical average of 19.6x. Markets often attempt to price in future events & typically move ahead of the fundamentals.

For a briefer on Fast Graphs, see Getting Started with Fast Graphs.

The Magnificent 7 are driving a disproportionate amount of the market fundamentals, sentiment, and ultimately price movement. How are valuations looking from a fundamental perspective?

Microsoft looks pricey, at 48x P/FCF, or a 2.1% FCF yield. Shares have historically traded for 19.5x P/FCF. The price seems to be getting way ahead of the fundamentals.

Alphabet shares look reasonable at 24x P/FCF, or a 4% FCF yield. Coupled with the double digit growth going forward, they can provide a compelling opportunity.

Amazon shares look pricey today (48.9x P/FCF, or 2% FCF yield), but if it delivers against expectations, it might even be cheaply priced.

Tesla shares seem objectively expensive at these levels – 159x P/FCF, or 0.6% FCF yield.

Nvidia shares have been flying higher, but that has been supported by fundamentals. The current price looks expensive (70x P/FCF, 1.4% FCF yield), but may be reasonable if Nvidia is able to deliver against expectations.

Apple shares seem pricey, coming in at 27x P/FCF compared to a historical multiple of 16.7x. The single digit growth makes it hard to justify the high multiple.

Meta shares seem reasonably priced. Even after the impressive recovery, shares trade for 30x P/FCF compared to a historical multiple of 34x.

Certain areas of the market seem extremely expensive. Examples include FICO, COST, CTAS.

Other areas seem to present some attractive opportunities, such as names in Real Estate and Consumer Staples. Examples include ADC, O, PEP.

As always, it is a market of stocks. Not the other way around!

Earnings

Over the last two weeks, 8 portfolio companies reported earnings.

Booking Holdings (BKNG)

Prior coverage:

Market, Earnings, and BKNG - August 5, 2023 - share price $3063

“We truly believe travel to be a great force for good. It is this deeply held belief that drives our mission day in and day out to make it easier for everyone to experience the world. … Travel will always remain fundamental to people’s lives.”

- Glenn Fogel, President & CEO, Booking Holdings

Booking Holdings is the parent company behind Booking.com, Priceline, Kayak, and OpenTable. The company is considered the leader in the travel space, with Airbnb as the closest contender.

Booking’s management team has always been well-rounded and fiscally responsible. They were disciplined throughout COVID – when travel came to an abrupt halt. They were disciplined in the aftermath when travel ramped back up quickly and money was extremely cheap.

The company continues to invest in innovation, bringing more and more of their audience firmly into their ecosystem with solutions for payments, full Connected Trip management experience, and AI chatbots.

Growth areas include flights, alternative accommodations (i.e. Airbnb-style rentals), and add ons like insurance, attractions, and transportation.

In 2023, Booking returned over $10 billion to shareholders via share repurchases. This reduced the outstanding share count by roughly 10%.

In the most recent earnings call, Booking established a quarterly dividend of $8.75, or roughly a yield of 1%. The dividend is in addition to the share buyback program. This is consistent with actions taken by many other technology companies including Salesforce, Meta, Paycom, and many more.

Diving into the financials:

TTM revenue growth came in at 25% and guidance shows further slow down to 20%. It is great to see continued growth after the post-COVID revenge travel phase. Throughout 2005-2019 growth rates were in the 10-20% range.

Gross margin of 85% is very healthy. It seems to be stabilizing there after continued expansion.

TTM EBITDA margins ticked down to 33%. This is not unexpected due to seasonality – Q4 is historically lower revenue & therefore lower margin.

TTM FCF margins also came in at 33%. It is nice to see FCF track EBITDA very closely. Oftentimes FCF exceeds EBITDA. The business is able to collect cash upfront. TTM FCF was $7 billion.

Balance sheet is very strong. Even after $10 billion in share repurchases, Booking has a net debt of $1.5 billion.

Shares outstanding came down significantly over the last year, most recently declining 9% y/y. The share count is down nearly 17% over the last 2 years!

EBITDA return on capital and FCF return on capital are very strong at 58% and 57% respectively. Booking is able to continue to grow the business without additional investment. In fact, they are returning a lot of money to shareholders which is bringing down the total capital invested.

Since the low of $1,625 set in October 2022, shares have been moving up nicely. They recently approached $4,000 before selling off post-earnings release. The sell off was likely due to the rapid ascent, coupled with lower guidance due to conflicts in the Middle East.

Over the last 3 years, Booking shares are up 50%, exceeding both the Nasdaq (+42%) and the S&P 500 (+35%).

As for valuation:

Booking Holdings has an enterprise value of $121 billion.

It trades at 5.2x NTM revenue and 15.3x NTM EBITDA. These are very reasonable multiples, especially for such a high quality company. The lower multiples may be due to the travel sector – travel being a discretionary purchase – which can be more cyclical than other sectors.

FCF yield of 5.8%, with 8% revenue growth, is very strong and compelling against the risk-free rate of ~4%.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share dilution of 4%, in an effort to be conservative.

Analysts expect EBITDA growth of 11.4%, 12.2%, and 11.7% for 2024, 2025, and 2026 respectively.

Shares currently trade at 15.3x EV/NTM EBITDA.

Even considering the share price movement upwards to $3,500, shares still represent a solid opportunity for further expansion.

On the lower range, if the multiple compresses to 14x and EBITDA grows at 10% CAGR, BKNG shares could generate returns of 13% per year.

On the higher end, if the multiple expands to 16x and EBITDA grows 12% CAGR, BKNG shares could possibly generate returns of 18%+ per year.

Looking at the Fast Graph for another perspective – if Booking delivers on the expectations and shares were to trade at the historical P/FCF multiple of 20.3x by December 2026, BKNG shares could generate returns of 21% per year.

Closing thoughts

Trends can be a powerful thing in the market. Overvalued stocks can stay that way for a long time. The risk of permanent loss of capital, however, can be a steep price to pay.

Regardless of what the market is doing, there are many opportunities and corners of the market. It is a market of stocks, not just a blanket stock market.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Federico Torre

Torre Financial

federico@torrefinancial.com

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.