Market, Earnings, and CRM - December 9, 2023

Market commentary, portfolio company earnings results, and a deeper look into Salesforce (CRM)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

After one of the strongest months on record, the market continues to grind higher. Over the last 10 trading days, there have been 5 down days and 5 up days.

The stability above the 450 level is promising. Investors interested in booking quick gains are selling, yet the market has been resilient. Buyers continue to support the market at this higher price point.

Going forward, selling interest may be limited. As the market breaks out to new highs, there is less resistance to work through (i.e. investors that sell as they “break even” or “finally recover”). Any selling from tax-loss harvesting is likely to be muted with the market up double digits this year.

There’s a high likelihood that the momentum can carry on through the rest of the year.

Year-to-date performance across indices:

Nasdaq +47%

S&P 500 +20%

Dow Jones +9%

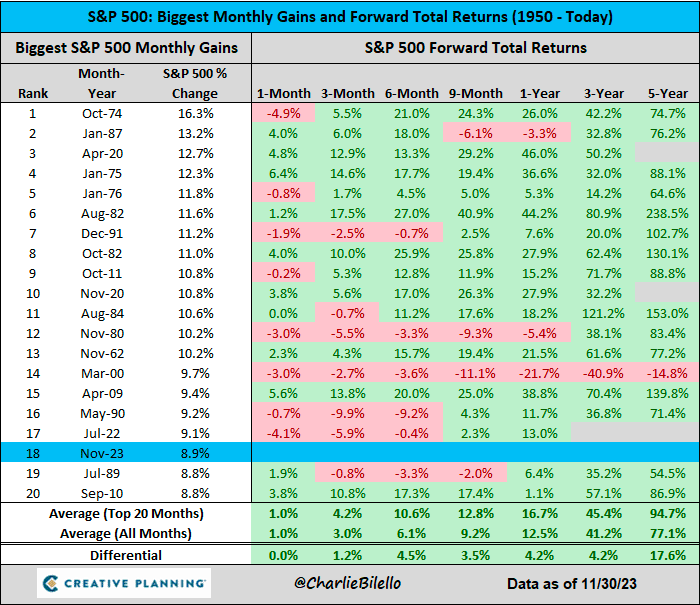

The market was up 8.9% in November, ranking as the 18th best monthly returns since 1950.

Forward returns after such a strong month have outperformed normal times. After the 20 best months, one year forward returns were +16.7% vs. the average +12.5% forward return.

As the Wall Street adage says: “strength begets strength”.

The volatility index (VIX) is down 43% this year. It dropped steadily throughout the year, before climbing back up to opening price in late October. Since then, the VIX is similarly down 43%.

Known as the “fear gauge”, the VIX measures the stock market’s expectation of volatility based on index options. It is a forward-looking index.

A high VIX means market participants expect a high level of volatility, or price movement. Uncertainty is undesirable. Markets tend to sell off.

A low VIX implies an low volatility ahead. Stable prices in a calm market can build investor confidence. The market tends to go up.

The market has generally performed very well after such dramatic declines in the VIX, often up 20%+ a year later.

Yields have similarly declined, lining up almost perfectly with the strong performance and lower VIX. After touching 5%, the 10-year treasury yield retreated back to 4.3%. Lower risk-free rates make equities and other investments more attractive.

The US Dollar (DXY) has been relatively stable throughout 2023, following significant strength in 2021 and 2022.

Crude oil prices have declined nearly 30% since the end of September. Crude oil serves as an input cost to many products and services and can have significant impact on inflation. Lower oil prices result in less pricing pressure.

Inflation seems range bound between 2.7% and 3.2%. While stable, the rate of inflation is stubbornly above the Fed’s 2% target.

The Fed’s rate hiking cycle is complete, according to market expectations. In fact, the market expects the Fed to cut rates by May.

Earnings

Seven portfolio company reported earnings over the last two weeks.

Many of these are technology companies and have their fiscal year offset by one month, ending on January 31st instead of December 31st.

One callout – the outsized beats across the board on EBITDA. Technology companies often invest heavily in R&D upfront to develop and enhance offerings. Software companies typically have flexibility to throttle future investment in order to boost profitability.

Salesforce (CRM)

Prior coverage: Market & Earnings Review - March 4, 2023.

Founder and CEO Marc Benioff wrote Behind the Cloud sharing the Salesforce story from inception to date. In the book, he shares his frustrations with the agility of large enterprises (i.e. his time at Oracle), how he envisioned a new way to deliver and sell software, Salesforce’s atypical marketing campaigns, how they created strong relationships with their customers making them strong advocates, and much more. It is a great read for anyone interested in Salesforce or software-as-a-service more broadly.

Studying a company’s past can help understand the company’s culture and DNA. These core character traits behind a company are what can propel a company forward. They faced many challenges and perservered, in large part due Benioff.

Over the last few years, the macroeconomic climate has changed significantly. Technology companies switched from leveraging cheap capital to grow at any cost to focusing on profitability as the cost of capital increased dramatically.

Salesforce is no exception. Earlier this year, Marc Benioff stated profitability as the company’s #1 priority.

“Our goal is to make Salesforce the largest and most profitable software company in the world, and that is what we are doing.”

Salesforce has a broad array of offerings, and continues to innovate.

“Our Customer 360 platform unites sales, service, marketing, commerce and IT teams by connecting customer data across systems, apps and devices to create a complete view of customers. With this single source of customer truth, teams can be more responsive, productive and efficient, deliver intelligent, personalized experiences across every channel and increase productivity. With Slack, we provide a digital headquarters where companies, employees, governments and stakeholders can collaborate to create success from anywhere.”

Salesforce has various offerings under their Customer platform:

Sales – allows sales teams to manage entire process from leads to opportunities to billing

Service – allows customer success teams to deliver personalized customer service and support across multiple channels (phone, chat, email,etc) as well as fieldwork; also includes an AI-powered chatbot

Platform – allows companies to build business apps with drag-and-drop tools

Slack – enterprise messaging system, “digital headquarters”

Marketing – allows companies to plan, personalize, and optimize customer marketing journies

Commerce – unify the shopping experience across mobile, web, social, and store

Analytics – business intelligence applications on top of their business data, includes Tableau

Integration – easily connect data from any system to deliver a connected experience, primarily MuleSoft

Data – “Genie”, a hyperscale real-time data platform

The Data cloud offering was recently announced at Dreamforce 2022, showing the company’s ability to continue to innovate and build new offerings.

The strength of the platform and new offerings is reinforced by some notable callouts from the most recent earnings call with Marc Benioff:

“We have 80% growth in deals more than $1 million.”

“We have a great new product. And everyone knows here at Dreamforce, Data Cloud. You can see in the quarter 1,000 new Data Cloud customers.”

“These Einstein GPT Copilots, this is a product we didn't really even have an imagination around a year ago. Of course, we had Einstein. Of course, we could see the incredible growth of Einstein. I mean now, Einstein with predictive and generative combined, is doing 1 trillion transactions a week, that's amazing. But more amazing is that 17% of the Fortune 100 are now Einstein GPT Copilot customers. And this is a product that is just coming to market.”

“Nine of the top 10 deals included six or more clouds. Think about that. Nine out of our top 10 deals included six or more clouds. So that we have amazing clouds, Sales Cloud, Service Cloud, Marketing Cloud, Platform, our Commerce Cloud, Slack, Tableau, MuleSoft, but think about it, how they're bringing all of those things together, Data Cloud, they're bringing it all together into a cocktail. That's amazing.”

“We're the only platform that are bringing CRM and data and AI and trust together for our customers in a way that enables them across every industry to be more successful, faster, be more productive, more efficient.”

“I'm saying to the copilot, hey, now can you rewrite this email for me or some -- make this 50% shorter or put it into the words of William Shakespeare. That's all possible and sometimes it's a cool party trick.

It's a whole different situation when we say, I want to write an e-mail to this customer about their contract renewal. And I want to write this e-mail, really references the huge value that they receive from our product and their log-in rates.”

Salesforce is very well positioned in the race for AI. They were quick to come out with a Data Cloud offering. They already have their customers’ most important data.

Market-perception-wise, Salesforce hasn’t benefitted from much of the AI hype. Certain peers including ServiceNow and Adobe have seen significant appreciation. Salesforce’s AI opportunity has not yet been fully recognized by the market.

Diving into the financials:

Revenue growth has remained relatively steady at 11% y/y. Guidance for Q4 calls for 10% growth. Salesforce also reports “remaining performance obligation” (“RPO”), which essentially represents customer commitments. There was a brightspot as it showed a 14% increase y/y, hinting at possible acceleration.

Gross profit of 75% has remained steady.

EBITDA margins are now up to 37%, expanding from 27% two years ago.

FCF margin has also increased to 26%, a new high over the last 3 years. Ideally we’d like to see the gap between EBITDA and FCF margins close. This is typically due to working capital – leniency on accounts receivables, resulting in the cash coming in later.

The balance sheet is healthy, with nearly $2.5 billion in net cash.

Shares oustanding have started to decrease this year. Salesforce has historically been very aggressive on stock based compensation (SBC) as well as in M&A to grow. This has resulted in dilution over time. The recently announced buyback program is starting to pay off, more than covering any SBC.

EBITDA and FCF return on capital (ROC) ratios of 17.6% and 12.3%, respectively, continue to improve alongside margins.

Salesforce shares have been taken on a ride the last few years. After hitting of $310, shares slid down to a low of $128 before starting to recover in January 2023.

This year has been a completely new chapter. Salesforce’s focus on profitbaility has been well received. Strong buying interest, as indicated by the green volume bars that line up with upwards moves, are strong signals of continued growth. The technical picture looks promising. Shares are up 90% YTD.

As for valuation:

Salesforce trades at a very reasonable valuation across both multiples: 6.4x revenue and 17.7x EBITDA. These are quite measured for such a high quality company.

For a different perspective, consider the FCF yield of 3.7% and ensuing growth of ~12% against the 10 year risk-free rate of 4.2%.

It is important to not take the yields alone at face value – the growth rate must be considered. For example:

In 10 years, the risk-free investment would still produce a yield of 4.2%.

In 10 years, Salesforce could have a FCF yield of 11.5% (3.7% * 1.12 ^ 10)

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share reduction of 1.5%.

Buying CRM, even after the recent run up at ~$250, still looks to be an attractive opportunity.

If the multiple (17.7x) stays steady between 16-18x, and EBITDA growth is equal to or faster than revenue growth (10-14%), then shares could return between 9-16% per year.

For another perspective on valuation, the Fastgraphs FCF chart shows possible annualized returns between 12-20% over a few years if shares trade between 25x FCF and 29x FCF.

Closing thoughts

The recent market performance has many investors holding positions in the green. Climbing performance, lower volatility, higher confidence, favorable macroeconomic conditions: all of these further fuel a virtuous cycle. Hence the saying, “strength begets strength”

Many of our portfolio companies have had impressive gains this year.

META +176%

CRWD +130%

CRM +90%

ADBE +81%

NOW +80%

Some of the names with the highest gains this year are very expensive, and may not necessarily be compelling opportunities looking forward.

Salesforce (CRM) bucks the trend. Notwithstanding the 90% YTD gain, there’s still opportunity for continued growth. Salesforce could benefit from all three engines of value:

Earnings growth

Change in P/E multiple

Change in shares outstanding

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Share

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.