Market, Earnings, and UnitedHealth Group (UNH) - January 20, 2024

Market commentary, portfolio company earnings results, and a deeper look into UnitedHealth Group (UNH)

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. Subscribe now to follow along.

Market

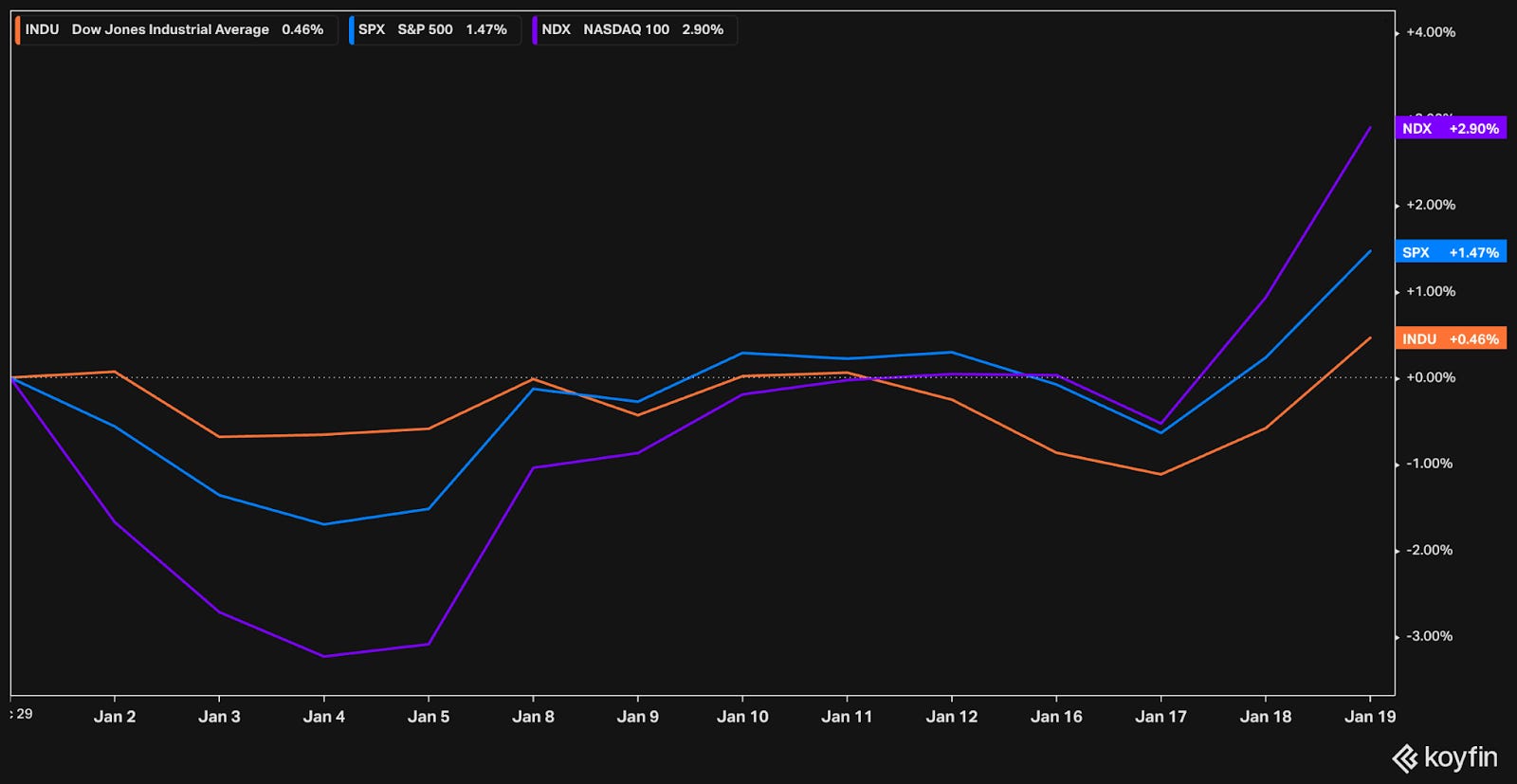

January got off to a soft start, with the S&P 500 in decline the first few days. The market looked to be range bound between 467 and 477. That didn’t last long.

The SPY reached a new all time high of 482 on Friday, January 19th, 2024. The prior high of 480 was set almost exactly two years ago on January 4th, 2022.

While the market faced some resistance, it seems to have broken out to the upside rather decisively. The two dips in late December and early January show higher lows, and the new all time high certainly clears an important resistance level.

Momentum can build on itself, and drive markets higher. We remain cautiously optimistic. Earning season just started – many large companies will be reporting in the next few weeks.

Year-to-date performance across indices:

Nasdaq +2.9%

S&P 500 +1.5%

Dow Jones +0.5%

On Liquidity

In a free market, prices are set by supply and demand. Liquidity, the amount of available cash in a system, is a key driver behind demand.

Aside from setting rates, another key tool the Fed uses to tighten or ease financial conditions is adjusting liquidity. They do this by increasing or decreasing their balance sheet – i.e. the Fed buying up treasuries releases cash into the world; the Fed selling treasuries takes cash away from the world and into their reserves.

In 2023, the Fed was shrinking their balance sheet – selling assets and taking cash away from the system, a tightening action.

The bump in March was in response to the failures of Silicon Valley Bank and First Republic.

Yet, liquidity, as measured by bank reserves, actually rose in 2023, as Alf pointed out.

Higher liquidity makes for easier financial conditions, which certainly helped fuel the market’s growth in 2023.

It turns out that the increase in liquidity is due to the Fed’s “reverse repo facilities.”

When rates were zero or negative, the “reverse repo” program allowed participants to effectively park funds with the Fed. The Fed purchased securities with the agreement to sell them at a higher price at a specific future date.

This practice, initiated in April 2021, helped take liquidity out of the system without having to raise rates. It also gave participants security and safe returns on their capital.

Following the 2023 rate hikes, there are now plenty of attractive options for yield. This has likely enticed participants to withdraw their money from the Fed, reintroducing it into the system.

There were over $2 trillion of “reverse repo” funds stored at the Fed.

To date, nearly $1.5 trillion has been withdrawn and hence reintroduced to the market – increasing liquidity.

There is still another $600 billion left.

This liquidity effect can continue to support the market, but will likely run out some time in 2024.

Relatedly, money-market funds and similar assets have seen a significant increase recently. This capital is effectively dry powder – investors’ capital that is ready to be put to use.

The $8.8 Trillion Cash Pile That Has Stock-Market Bulls Salivating - WSJ

Increased liquidity increases demand for investments. Equities, one of the largest asset classes in the world, are likely to benefit.

On Cybersecurity

In July 2023, the SEC announced new disclosure rules regarding cybersecurity practices & incidents.. This recap released in December provides additional context.

The rule went into effect in December 2023 for large companies; smaller companies have until June 2024 to begin complying.

This new spotlight only adds to the increasing attention to and importance of cybersecurity posture. Every company must have a plan in place.

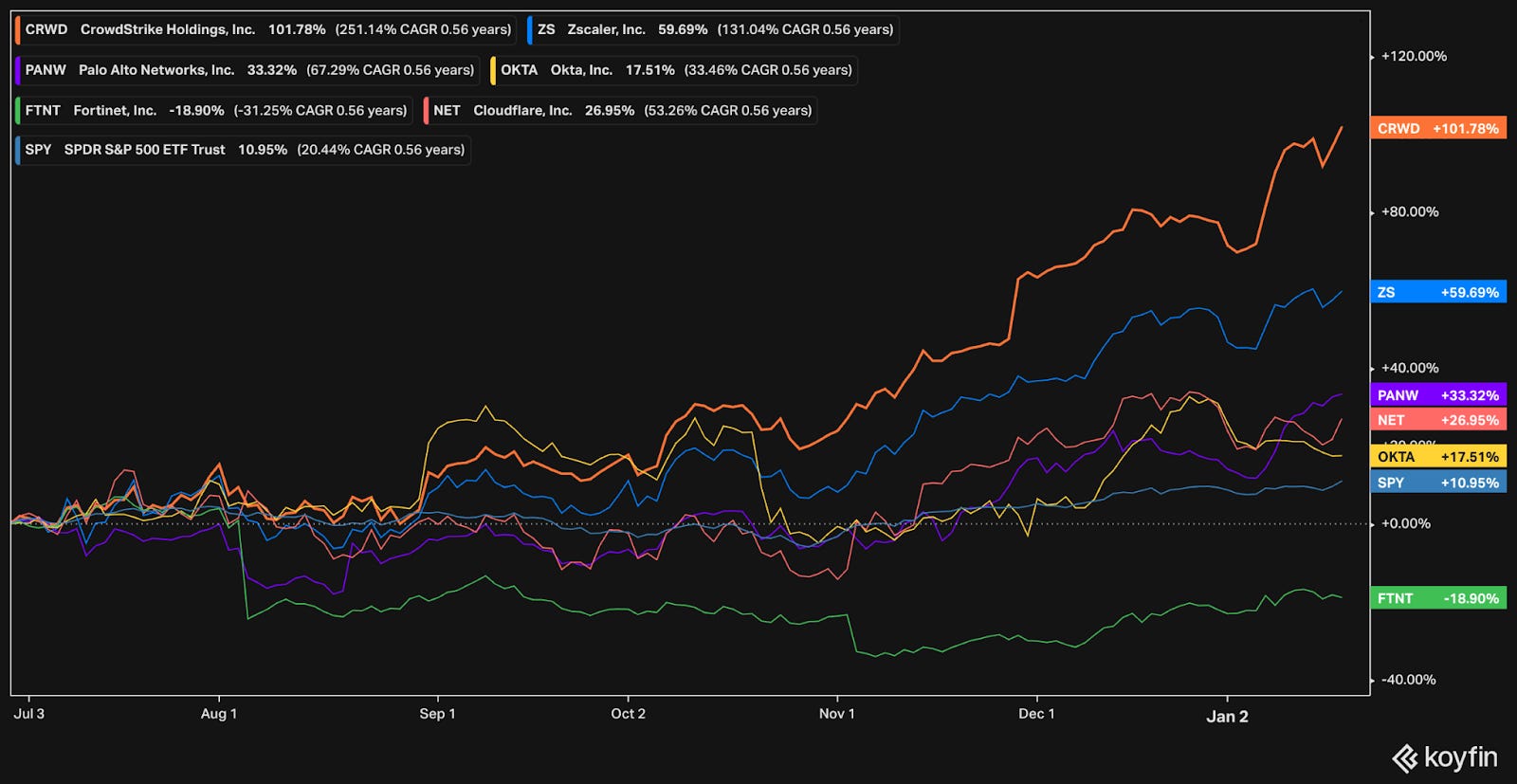

Naturally, companies that provide cybersecurity solutions have benefited. Since July, …

Crowdstrike (CRWD) is +102% (vs +11% for SPY)

Zscaler (ZS) is +60%

Palo Alto Networks (PANW) is +33%

Cloudflare (NET) is +27%

Okta (OKTA) is +18%

Fortinet (FTNT) is -19%

While these companies are likely to see increased demand and durable growth in the wake of these announcements, it is not uncommon to see the market get ahead of itself.

Investors should keep a close eye, as most of these companies are fetching premium valuations. Many of these names, for example, have FCF yields less than 1.5% – less than half the 3.25% of the S&P 500.

Earnings

One portfolio company reported earnings over the last two weeks.

UnitedHealth Group (UNH)

Prior coverage:

Market & Earnings Review - July 22, 2023 – UNH $506

Market & Earnings - January 21, 2023 – UNH $486

“UnitedHealth Group Incorporated is a health care and well-being company with a mission to help people live healthier lives and help make the health system work better for everyone. Our two distinct, yet complementary business platforms — Optum and UnitedHealthcare — are working to help build a modern, high-performing health system through improved access, affordability, outcomes and experiences for the individuals and organizations we are privileged to serve.”

UnitedHealth Group has four reportable segments:

Optum Health

Comprehensive care services, including primary, specialty, surgical, urgent, in home, virtual, and more; serves over 102 million consumers; 4 million patients in value-based care

~17% of revenue

~21% of operating income

Growing 30%+

8.5% operating margin

Optum Insight

Data, analytics, research, consulting

~3% of revenue

~12% of operating income

Growing 20%+

24.6% operating margin

Optum Rx

Pharmacy care services, managing over $124 billion in pharmaceutical spending

~20% of revenue

~15% of operating income

Growing 9%+

4.4% operating margin

UnitedHealthcare

Health insurance, typically offered through employers; serving over 26.7 million people

~60% of revenue

~50% of operating income

Growing 12%+

5.8% operating margin

UnitedHealth Group continues to execute according to their plan – the growth opportunity is in Optum Health, driving forward value-based care solutions.

Optum Health’s value-based care business has more than doubled in the last 2 years, growing to over 4 million patients. And they are doing it at a higher margin (8.5%) compared to the traditional insurance coverage model (5.8%)

In the last earnings call, CEO Andrew Witty commented:

“We remain confident in and committed to our long-term 13% to 16% adjusted earnings per share growth rate.”

“Value-based care for us is a proven way of overcoming many of the widely recognized shortcomings of a fee-for-service-based health system, such as fragmented consumer experience and incentives that can emphasize volume over quality. Our value-based offerings empower physicians to provide more connected, coordinated and comprehensive care, align incentives among consumers, care providers and health plans, deliver better health outcomes and improve costs.”

While there are certainly many secular tailwinds (people living longer, data analytics, etc), UnitedHealth and competitors have recently mentioned an increase in medical costs. As a healthcare insurer, UNH receives premiums and covers any medical expenses. If expenses are low, they have higher profit! If expenses are high, they have lower profit. The increased medical consumption is expected to be reflected in tighter margins this year.

For 2024, UnitedHealth expects revenue of $400 billion with a medical care ratio of 84%.

Diving into the financials:

Revenue accelerated up to +2% q/q, and is up to 15% y/y. For UNH, being a mature company, this is great. TTM revenue growth has been steadily climbing up the last few years. We wouldn’t be surprised to see that stabilize here.

Gross margins ticked lower to 23%, from 25% previously – likely due to increased medical costs. This gross margin is much lower than other portfolio companies, primarily due to the nature of UNH’s business.

EBITDA margin of 10% and FCF margin of 7% are appropriate for the company. The divergence between EBITDA and FCF is something to keep an eye on.

Balance sheet is reasonable with nearly $30 billion in net debt, or less than 1x TTM EBITDA.

Share counts have been declining, with the exception of the most recent quarter. We’ll want to see share counts continue to decline.

Capital efficiency is solid, with EBITDA return on capital and free cash flow return on capital at 23% and 16% respectively. Again, these have diverged over time and we’d like to see that revert back.

Contrary to many technology stocks, UnitedHealth Group’s shares have had a rather smooth trajectory. Shares climbed all throughout 2022 with the broader market. The next year, 2023, was met with some turbulence, but with a maximum drawdown of less than 20%. Shares hit the “golden cross” in September 2023 and continued to march higher.

Recently, the stock is showing weakening technical signals, forming lower lows in the most recent dips. While the company is fundamentally sound, concerns of higher medical cost ratios and a weakening technical picture may lead to lower prices ahead.

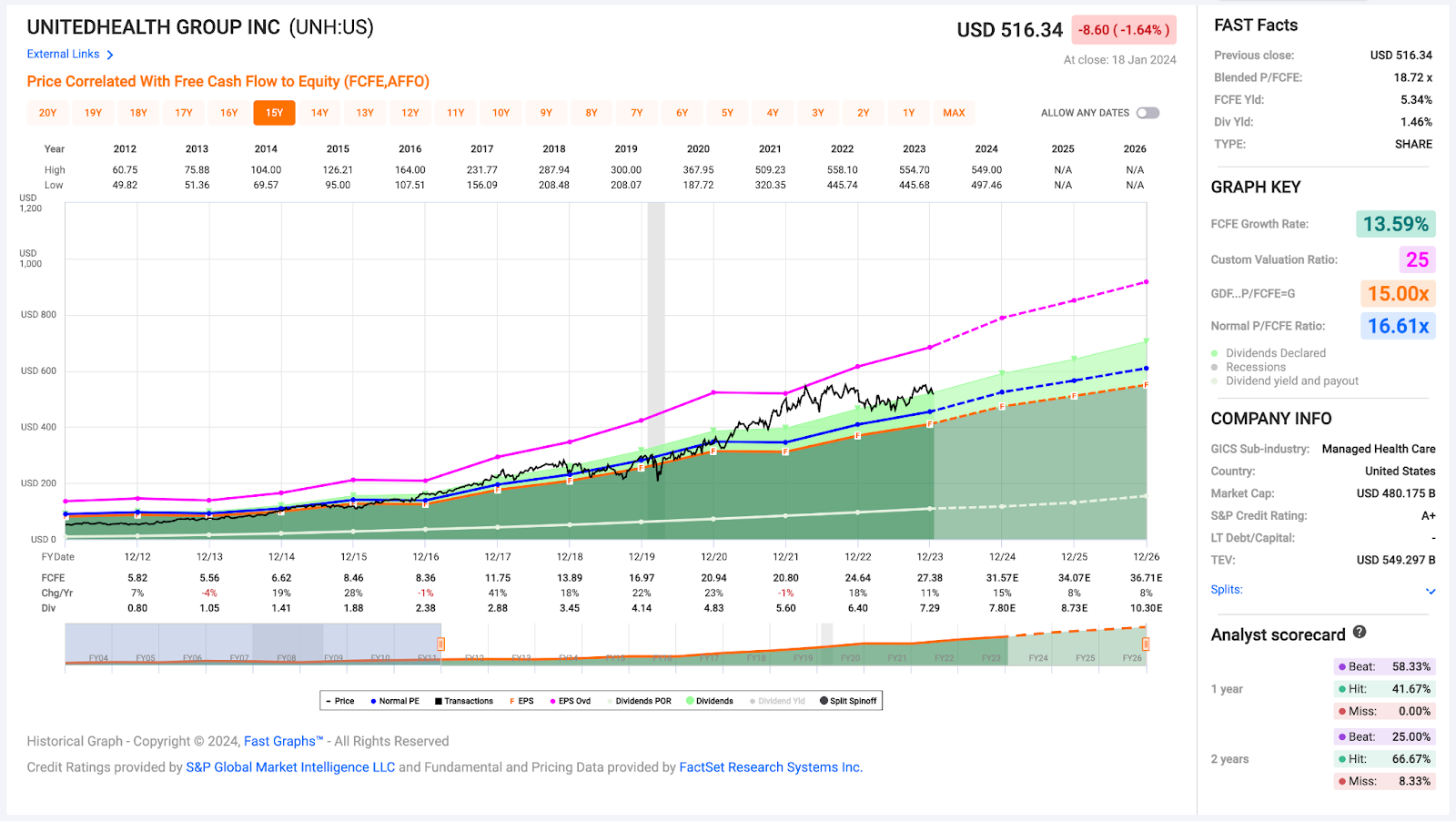

As for valuation:

UnitedHealth Group seems to be attractively valued, going for a FCF yield of 5.2% and growing at 14%. The current FCF yield and fundamental multiples are not very demanding for such a high quality, proven company.

The following table shows possible annualized returns over the next 5 years across various scenarios. The model assumes annual share reduction of 1%.

Analysts expect EBITDA to grow 9-10% through FY 2026. UNH shares could produce returns of 10-15% per year if the multiple is at least maintained.

Fast Graphs provides another perspective on valuation.

If UNH shares trade at the normal P/FCF ratio of 16.6x (slightly compressing from the current 18.7x) by the end of 2026, UNH would return at least 7% per annum.

Closing thoughts

Following a blockbuster 2023, the market continues to push higher in early 2024. Momentum can build up and drive prices beyond reasonable expectations. At the same time, for every point higher, valuation becomes that much more stretched.

At Torre Financial, we remain focused on finding the best investment opportunities at any time. We focus on companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to what the market is offering.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders – companies with high return on capital, competitive advantages, and durable growth.

Federico Torre

Torre Financial

federico@torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.