Torre Financial's Portfolio Management

Recent market rotation, note on value investing, portfolio composition, rationale behind purchases

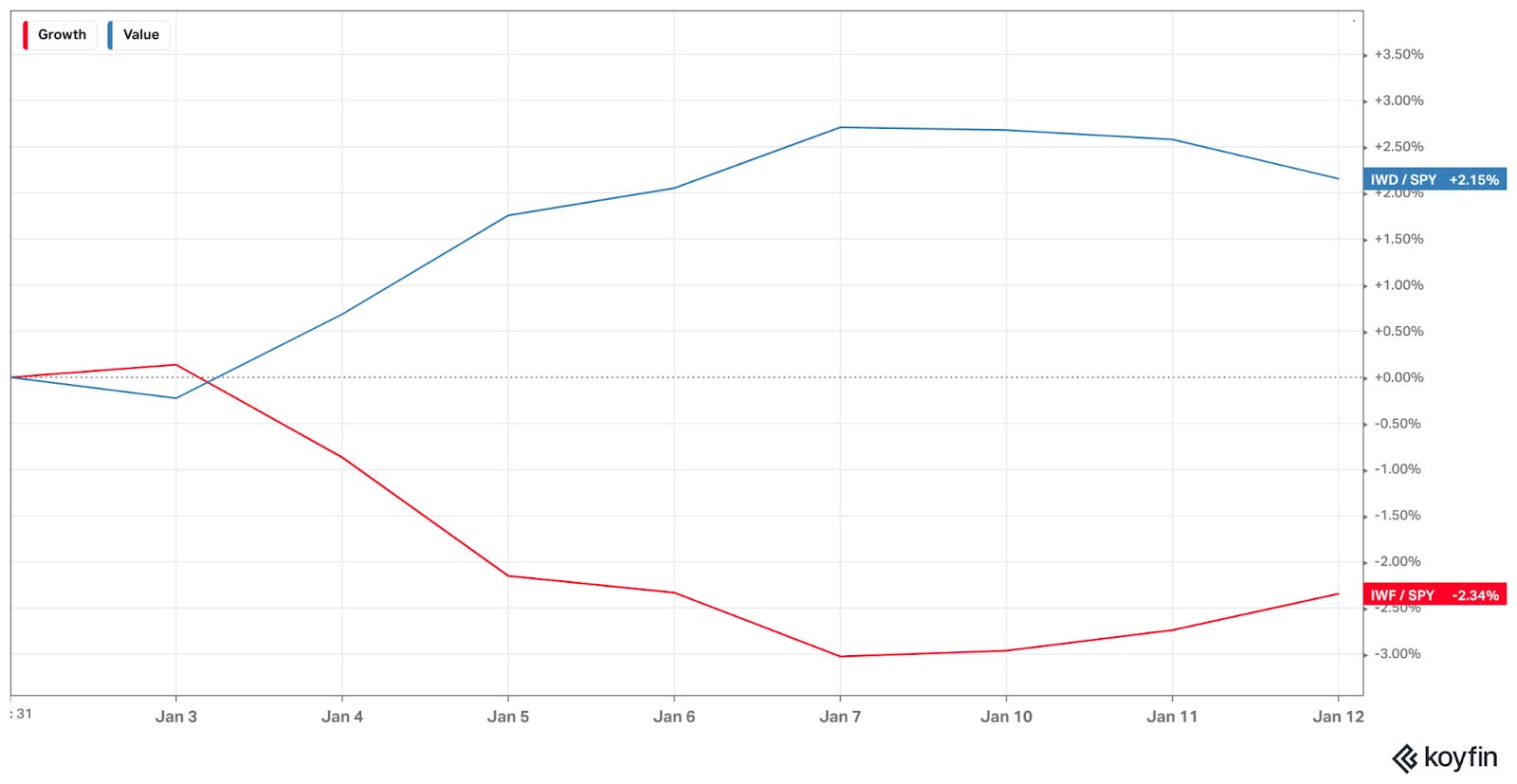

The new year is off to a volatile start, with significant rotation amongst underlying sectors fueled by concerns of the Fed moving to increase rates at a faster clip.

Two-thirds of the stocks in the Nasdaq Composite were in bear markets, down 20% or more from their 52-week high – and 40% of them were down 50% or more.

The exodus out of technology has found its way into cyclicals, financials, and other value stocks.

The current market environment can be alarming, resulting in new winners and losers.

While I’ve previously written about my investment process and the types of companies I look for, I wanted to share some additional insights into how I manage portfolios at Torre Financial.

First, a quick note on value investing.

On Value Investing

The financial industry coined value and growth as terms to easily categorize companies.

Value is the label used to group companies with low ratios - low P/E, low P/S, low P/B, and oftentimes low growth.

Growth is used to group the opposite side of the spectrum - high P/E, high P/S, high P/B, and oftentimes high growth.

Recall that the fundamental, intrinsic value of any investment is the sum of all future cash flows discounted to the present value.

Multiples of any kind, be it P/E, P/S, P/B, or any variation thereof, are merely shortcuts. While many market participants use multiples as a way to communicate easily and compare across companies, multiples alone do not inherently represent the potential or intrinsic value of an investment opportunity. Multiples are most useful when comparing a company to itself (without drastic changes in operation) or other similar companies.

Investors are best served by focusing on finding great investment opportunities at great prices, as determined by the discounted future cash flows.

In order to grow free cash flow, companies can fundamentally 1) reduce costs and/or 2) grow revenue.

Value companies tend to have cyclical, slow, or even negative growth. Their source of improvements typically come from cost optimization. There is an inherent limit to cost reduction.

Revenue growth is much higher potential, limited only by the company’s addressable market. Companies with large addressable markets, demonstrated growth, and strong fundamentals have a more durable path to both grow and maintain free cash flow.

Portfolio Composition

Torre Financial looks to invest in both emerging and established compounders.

Given the focus on consistent revenue growth and high return on invested capital, the companies skew toward asset-light models.

Of the 28 portfolio companies, 10 are emerging compounders and 18 are established compounders.

Emerging compounders tend to be concentrated in high-growth technology companies. Eight of them are enterprise software companies (UPST, CRWD, OKTA, PAYC, VEEV, NET, DDOG, PLTR), one is a hardware company (ANET), and one is a discount retailer (FIVE).

Seven emerging compounders grew annual revenue between 40%-65%. Three grew revenue around 25%. One grew revenue at 250%.

All but two companies (NET, OKTA) are free cash flow positive.

Established compounders vary more broadly across industries: two big tech advertisers (GOOGL, FB), one big tech discount retailer (AMZN), three payment technology companies (V, MA, PYPL), two investment rating and analytics companies (SPGI, MCO), four enterprise software (CRM, WDAY, BR, INTU), one financial exchange company (ICE), one homebuilder (NVR), one healthcare insurer (UNH), one medical device company (ISRG), one consumer retailer (SBUX), and one regional bank (FRC).

Established compounders are also growing revenue significantly, with half growing revenue at rates between 20-40% and the other half growing at rates between 10-20%.

More than half of the portfolio companies are founder-led.

By portfolio weight, the split between emerging and established compounders is roughly equal. The portfolio often has greater concentration in the fewer emerging compounders in an effort to take advantage of my insight as a technology operator as well as a result of their growth.

While I may adjust positions when appropriate, I look to invest in the best companies and minimize portfolio turnover.

Expected Returns

I don’t pretend to know what the portfolio returns will be. I don’t know what will happen over the next month, six months, year, or two. I certainly do not guarantee any returns.

What I do know, and can share, is how I go about reasoning purchases.

Note that a significant portion of the effort to analyze a company and include it in the portfolio is qualitative. Valuation is only assessed once a company has cleared the bar.

Expected returns are keyed on two fundamental aspects, requiring both quantitative and qualitative assessment: the current valuation and the future possibility.

I assess investment opportunities over a five year holding period, deemed sufficient for the market to realize an appropriate valuation.

While I look for investments that can return 15%+ annual returns, I focus more time on downside scenarios. Using more conservative estimates, I look for entry prices that should result in annual returns of no less than 10%.

Discounted cash flows are the essence of the analysis. However, modeling exact numbers can oftentimes lead to a false sense of security — highly precise yet likely inaccurate.

I approximate the return potential by assessing potential outcomes over the next five years, considering various multiples and revenue growth rates.

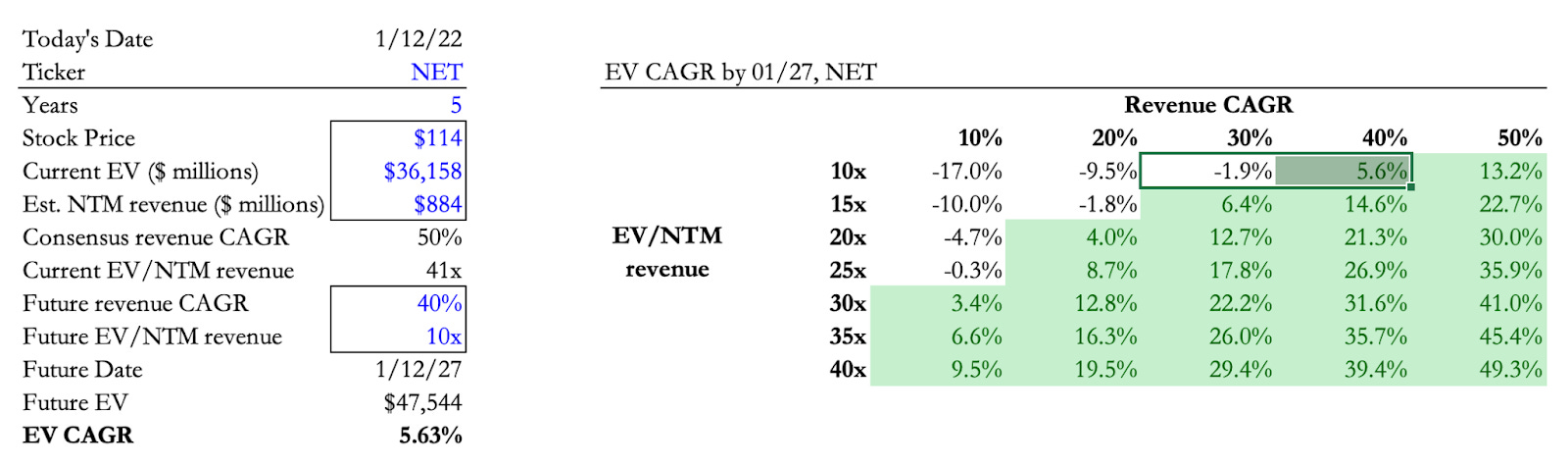

Consider the following sensitivity table for Cloudflare (NET).

The company currently trades at 41x next-twelve-months revenue. Consensus estimates call for 50% revenue growth over the next couple of years.

For my valuation assessment, I consider a reduced revenue growth rate of 30-40% and multiple compression to 10x. In this conservative scenario, enterprise value annual growth is quite muted ranging from -2% to 6%.

For a more attractive entry price, consider Okta (OKTA).

The company currently trades at 18x next-twelve-months revenue. Consensus estimates call for 36% revenue growth over the next couple of years.

Considering a conservative scenario with revenue growth rates of 30% and multiple compression to 10x, the expected annual growth would be above 15%.

Multiple compression to 10x is rather conservative. In the case that multiples persist any measure above 10x, the returns would be far more attractive.

Appropriate revenue growth expectations are based on the company’s fundamentals – their growth opportunities and ability to execute on it. Qualitative understanding of the business is informative as to what is possible. For example, many of our SaaS companies have net dollar retention rates above 100%, indicating that they have built-in revenue growth from their existing customers.

A similar exercise using EV/EBITDA and P/FCF is conducted for more established companies.

This valuation exercise is not intended to be an exact science. Rather, it acknowledges dealing in probabilistic thinking, basing the assessment on the likelihood of various outcomes.

In probabilistic approaches, the process should be of greater importance than the short-term results, which will inherently have noise.

Investing presents asymmetrical opportunities. While there will be investment errors, errors are capped at a loss of 100%.

Investing in great companies with large addressable markets allows for much greater upside, whether 10x, 100x, or more. The biggest mistake may be to sell a great company too early.

Conclusion

Those people who can sit quietly for decades when they own a farm or apartment house too often become frenetic when they are exposed to a stream of stock quotations and accompanying commentators delivering an implied message of “Don’t just sit there, do something.” For these investors, liquidity is transformed from the unqualified benefit it should be to a curse.”

-Warren Buffet

An interesting comparison between liquid and illiquid assets: when investors get a price they don’t like with illiquid assets such as a house, they don’t worry about it. They just say no and continue to wait for the right offer. In the market, however, streaming quotes seem to cause investor anxiety.

Downdrafts are undoubtedly unpleasant in the short term. To have conviction, it is important to understand the underlying process by which decisions are made. For the patient investor, downdrafts have historically proven to be great opportunities.

During difficult times, investors are best served by focusing on their companies instead of worrying about short-term price action.

--

Torre Financial is an independent investment advisory firm focused on emerging and established compounders.

Federico Torre

Torre Financial

federico@torrefinancial.com

https://torrefinancial.com

Disclaimer: This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.