2023 Q3 Letter

Review of quarterly results, contributors and detractors, portfolio overview, and personal reflection

Results

Friday, September 29th, 2023 was the last day of trading for the third quarter.

The consolidated return for Torre Financial accounts was +0.60% for the quarter.

For the same period, the S&P 500 (SPY) returned -2.98%.

Returns for individual accounts may vary as each account is managed separately.

Contributors and Detractors

Top Performers in Q3

Crowdstrike (CRWD), a leader in cybersecurity that we first covered in July 2020, is having a strong year. The cybersecurity space has been resilient, with sales growth holding up much better than other sectors. The increasing cost of capital is weighing heavily on a low-pricing competitor (SentinelOne), whilst having nearly no effect on Crowdstrike due to their strong FCF generation.

Booking (BKNG) and ADP (ADP) are two new positions over the last 2 quarters. It is nice to see them performing early on. Both companies continue to be attractively valued on a FCF yield basis, especially considering their growth and capital efficiency.

MSCI (MSCI) and Intuit (INTU) were both in the bottom performers list last quarter. MSCI’s business has been more resilient than expected, with financial institutions continuing to crave more and more data. Intuit continues to innovate across the small-and-medium business space, leveraging their existing customers to build a network and establishing themselves as an AI leader.

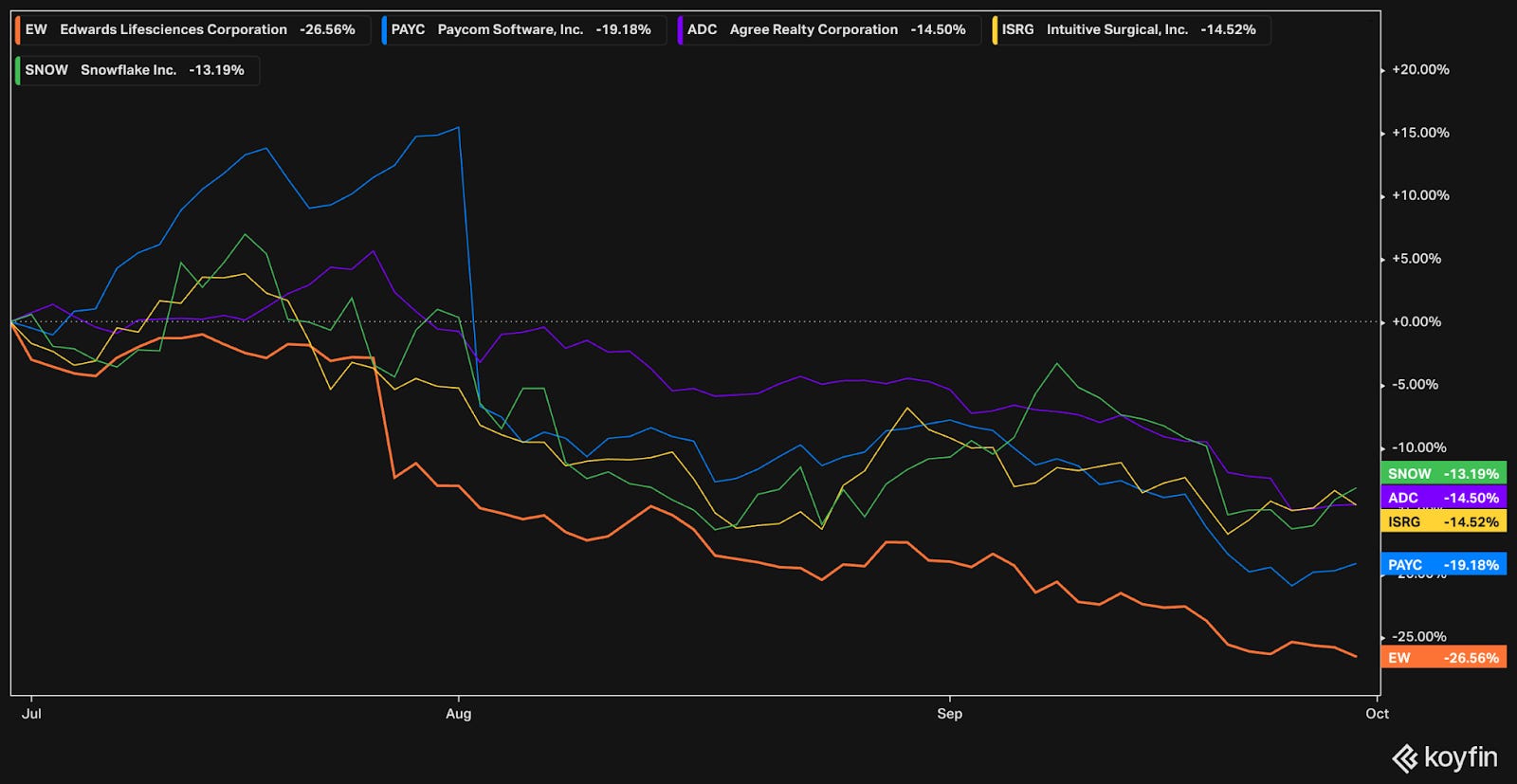

Bottom Performers in Q3

Edwards Lifesciences (EW) was one of the worst performers for the quarter. It is a brand new addition to our portfolio, and we initiated our positions in September. We expect this decline to subside shortly. Possible explanations could be the planned change in CEO or concerns about the agreement with Medtronic. On a fundamental level, the company is doing well and has raised guidance in their last two quarters.

Paycom (PAYC) is an up and coming challenger in the small-and-medium business payroll space. With less than 5% of market share and growing rapidly, Paycom has established themselves as a real contender. Given their very strong fundamentals (20%+ revenue growth, 20%+ ROIC and FCFROC) Paycom was highly valued by the markets. Possible explanations might be the high valuation and concerns about macroeconomic impact on SMBs.

Agree Realty (ADC) is making a repeat appearance on the detractors list. The real estate sector has been in pain this year as the higher rates ripple through the economy. There is over $1 trillion in debt maturing over the next 12 months. Certain sectors such as office are suffering significant vacancies. Higher yields from short term treasuries are very competitive against cash flow from REITs. The entire real estate index is down 8% in the last month alone. All that being said, Agree is one of the highest quality REITs out there. With a triple net lease model, a significant base of investment grade tenants, and a fortress balance sheet they are primed to benefit from the downturn and come out stronger. Additionally, insiders have been purchasing a significant amount of shares recently.

Intuitive Surgical (ISRG) is seeing a recovery in procedures, recently raising guidance to 20-22% growth this year. They did acknowledge pressure in bariatric procedures (i.e. weight-loss surgery) due to the rise of weight loss medication. It is only one of the many procedures that Intuitive’s products cover, but it is a small headwind. The company continues to trade for a premium (14-15% growth, 9-10% ROIC, 1.5% FCF yield). Notwithstanding, there’s a long runway ahead and they are a clear leader in minimally invasive robotic surgery that could also have further AI upside.

Snowflake (SNOW) continues to operate according to plan. As many companies focused on austerity measures, Snowflake helped them optimize usage. Having a consumption-based business model, this has been a headwind over the last year. Lower growth coupled with its premium valuation can be a possible explanation for the underperformance this quarter. They are well positioned for the wave of AI applications coming to the enterprise space. The AI hype has translated to sales for hardware vendors (i.e. Nvidia). Once the infrastructure is in place, software will be the next phase.

Portfolio Overview

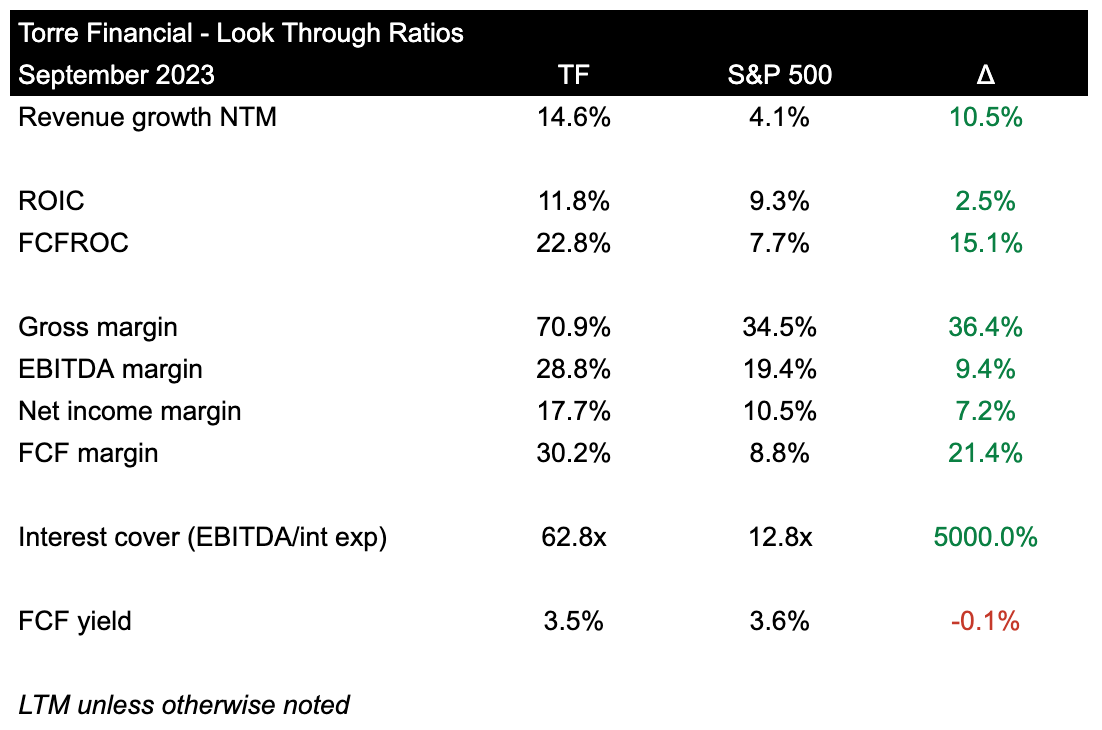

We seek to invest in the highest quality companies, those that are efficient and exhibit durable growth.

Efficient businesses make the most of their available capital (high return on capital ratios), are profitable (high margins across the board – gross, free cash flow, net income), and are effective at converting earnings into free cash flow (low capital intensity).

Durable growth can come from secular tailwinds (growing industries) as well as business model dynamics (increasing usage or consumption with existing customers; pricing models that grow with inflation).

The combination of efficiency and growth, sustained over time, maximizes the magic of compounding. At Torre Financial, we look for these companies and seek to invest at reasonable prices.

When compared to the S&P 500, our portfolio companies are superior in revenue growth, are more efficient in their use of capital, have superior margins across the board, have stronger balance sheets (higher interest payment coverage, through lower leverage), and have a very comparable FCF yield to that of the index.

This combination of superior fundamentals and reasonable valuation allows for a high probability bet of outperformance.

High quality companies are rare, there are only so many out there. In line with our investment philosophy, we aim to keep portfolio turnover at a minimum. Each company is rigorously evaluated and vetted as a long-term opportunity before being introduced.

We hold our portfolio to a maximum of 30 companies, ensuring we pick the best of the best and make the hard decisions when necessary. We strive to invest for 5+ years, which implies we turn over fewer than 6 companies a year. Our turnover activity is low, yet incorporates significant investment in research. We spend a lot of time learning, so that we can have the best possible companies and target allocation.

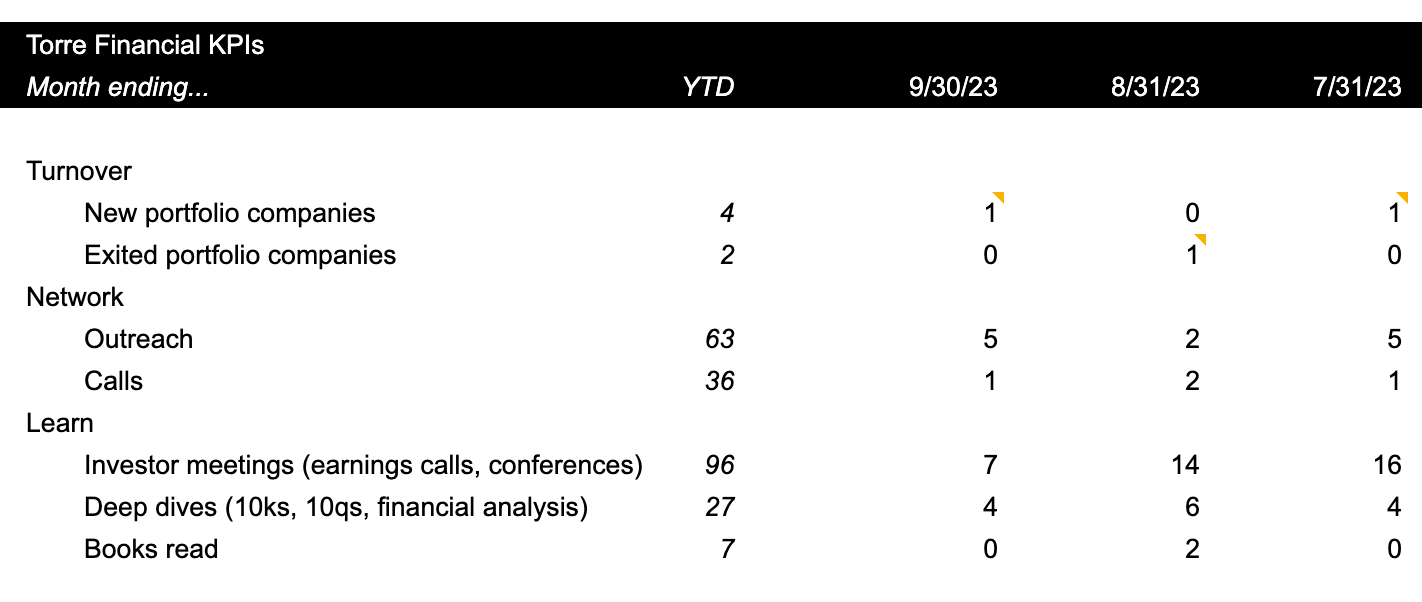

As introduced in our 2023 Q1 Letter, we are continually evolving our processes to improve any and all aspects. Some of the key performance indicators of our work input are shown below.

This quarter, we added 2 new companies and exited 1. Year-to-date we have added 4 new companies.

Diving into the details on the portfolio and target allocation weights, …

Subscribe to continue reading and get detailed insights into portfolio management including the full list of portfolio companies, specific allocation each month, rationale behind our decision making, and our plan going forward.

Keep reading with a 7-day free trial

Subscribe to Torre Financial Newsletter to keep reading this post and get 7 days of free access to the full post archives.