2024 Q1 Letter

Review of quarterly results, contributors and detractors, portfolio overview, and personal reflection

Every two weeks we share a review of the market, any earnings results, and a deep dive into one portfolio company. At the end of the quarter, we’ll share our quarterly letter. Subscribe now to follow along.

Results

The last day of trading for the first quarter was on Friday, March 29th, 2024.

For the quarter, the consolidated return for Torre Financial accounts was +7.6%.

For the same period, the S&P 500 (SPY) returned +10.4%.

Returns for individual accounts may vary as each account is managed separately.

Contributors and Detractors

Of our 29 portfolio companies:

21 (72%) were positive for the quarter, with gains ranging from 1% to 26%

8 (28%) were negative for the quarter, with losses ranging from -1% to -18%

Regarding relative performance:

10 (34%) outperformed the S&P 500’s 10.4% gain

19 (66%) underperformed the S&P 500’s 10.4% gain

One big factor this quarter was the outperformance of chip stocks, of which we do not own any. The semiconductor ETF SOXX gained 17.8% for the quarter, including NVDA’s +82%.

Portfolio weighting helped our results when compared to the index. While only 66% of companies outperformed the S&P 500, we achieved 73% of the indices gain.

Top Performers in Q1

Meta (META) is a repeat top performer. After nearly tripling in 2023, shares added another 37% this quarter. Meta has focused on efficiency and fortifying their core offerings. They continue to invest in the metaverse, albeit more moderately. Meta is well positioned as a leader in the AI movement.

CrowdStrike (CRWD) is another repeat showing on the top performer list. CrowdStrike is a leader in the cybersecurity space and is now seen as a credible, next-generation challenger to Palo Alto Network’s dominance. We most recently covered CrowdStrike on March 16th, 2024. Our initial coverage was back in July 2020.

Edwards Lifesciences (EW) seems to have turned a corner this quarter. Edwards is a leader in fighting cardiovascular disease. In our Q3 2023 review, Edwards appeared as the worst performer. We had just initiated our position, covering the company in September, 2023. The new CEO seems to be settling in just fine, the company seems to be on path to return to double digit growth, and they have many promising studies coming this year.

The Trade Desk (TTD) is having a solid start to the year. They have been resilient to macroeconomic weakness as they continue to gain market share in the digital advertisement space against the tech giants’ “closed gardens.” Election years are known for bringing increased advertisement spending. We most recently covered TTD in February, 2024.

Airbnb (ABNB) had a strong quarter, despite ongoing fears of a recession. While discretionary spend could be impacted in a recession, Airbnb has proven to be quite resilient since their restructuring post-COVID. Airbnb’s strong marketplace allows for significant operational leverage.

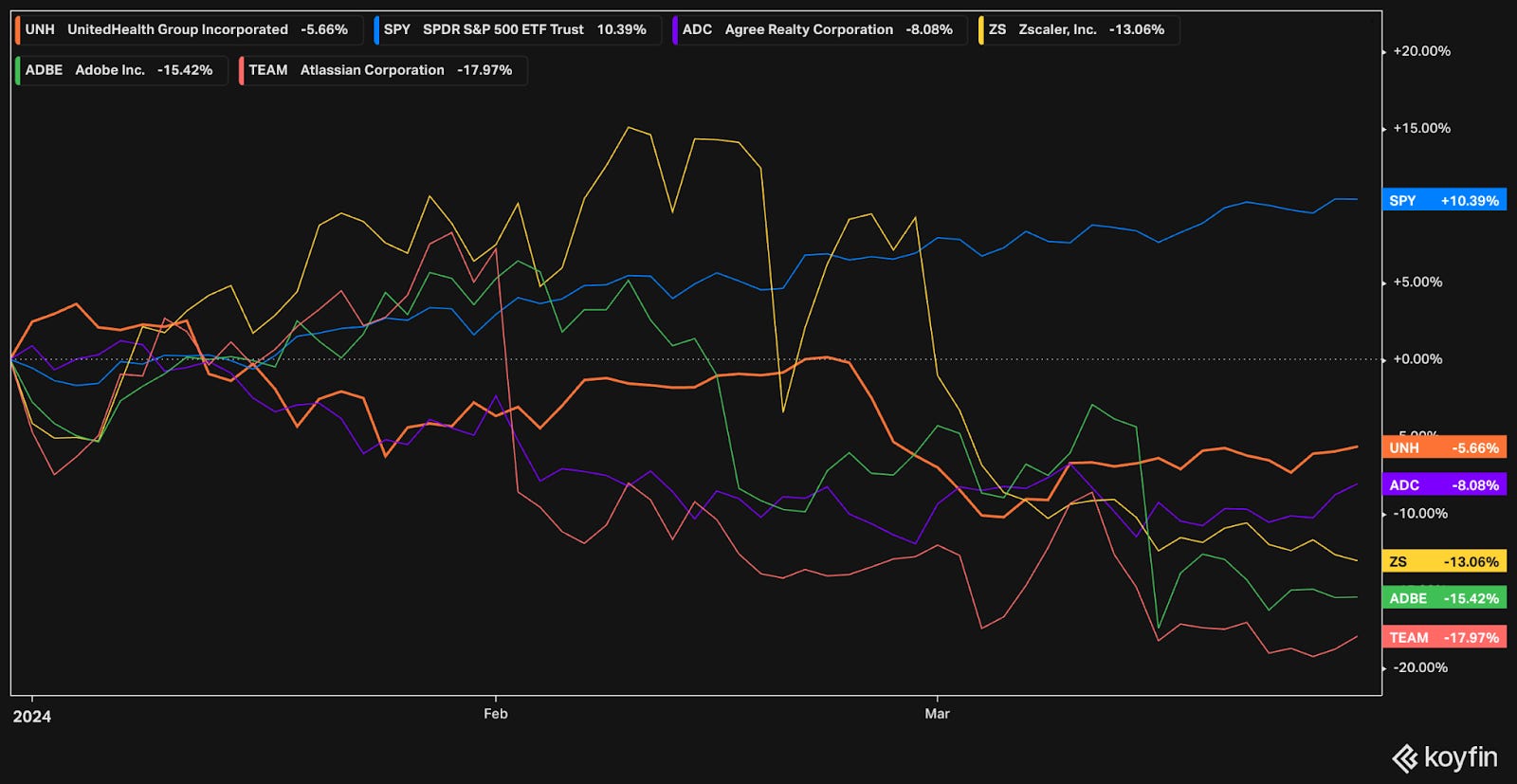

Bottom Performers in Q1

Atlassian (TEAM) joined our portfolio this quarter. We initiated our position this March. While it was the worst performer for the quarter, down nearly 18%, that is in part why it appears! Atlassian started as a software for filing and tracking bugs in software. Jira, their main offering today, is used by many development teams across the world. They have continued to roll out many new products including Confluence which is an enterprise wiki offering, Jira Workflows for ticket management, Bitbucket for code hosting, OpsGenie for on call alerting, and many more. As an enterprise SaaS company, they have strong recurring revenue. Coupled with low churn, ongoing innovation, and strong financials, Atlassian is a very attractive company.

Adobe (ADBE) was down 15% this quarter. They had previously agreed to acquire Figma, an up-and-comer in the collaborative design space, for $20 billion. While it was a very steep price, it would have further cemented Adobe’s stronghold on the market. Adobe ended up terminating the deal, unable to overcome the anti-competitive concerns of European regulators. Adobe had to pay a $1 billion break up fee. Notwithstanding, Adobe has come out very strong in the rise of AI. Their professional tools are quickly incorporating many new generative-AI technologies. Our conviction is strong, and we’ll be looking to increase our position over time.

Zscaler (ZS) was down 13% this quarter. Aside from Palo Alto Network’s commentary about softening billings, there weren’t many significant influences. Cybersecurity continues to be a compelling space. Zscaler operates at the core, protecting networks with zero trust solutions. We had trimmed cybersecurity exposure on valuation concerns. We see this pullback in Zscaler as an opportunity to slowly build exposure.

Agree Realty (ADC), a triple-net REIT, has appeared on the detractors list a few times now. Real estate broadly continues to feel the impact of higher rates. ADC is one of the highest quality REITs in the world. They have a strong focus on risk-adjusted returns; a strong base of investment-grade tenants including Walmart, Tractor Supply Co, Home Depot, and many more; and a strong balance sheet, which has allowed them to take advantage of market weakness. Insiders continue to purchase shares. In 2023, insiders purchased nearly $12 million worth of shares. In 2024 to date, they have purchased nearly $4.2 million worth. A rotation into REITs is likely to come this year. We have no issue collecting the monthly distributions as we wait for the market to turn.

UnitedHealth Group (UNH) was down nearly 6% this quarter. One of their subsidiaries, Change Healthcare, was hit by a cyber attack placing sensitive customer data at risk. Another possible explanation for the underperformance is the more defensive nature of UNH. When the market is going up and looking for growth names, the steady low-beta names tend to underperform. UnitedHealth shares have very low correlation to high growth tech names. We added to UNH throughout the quarter.

Portfolio Overview

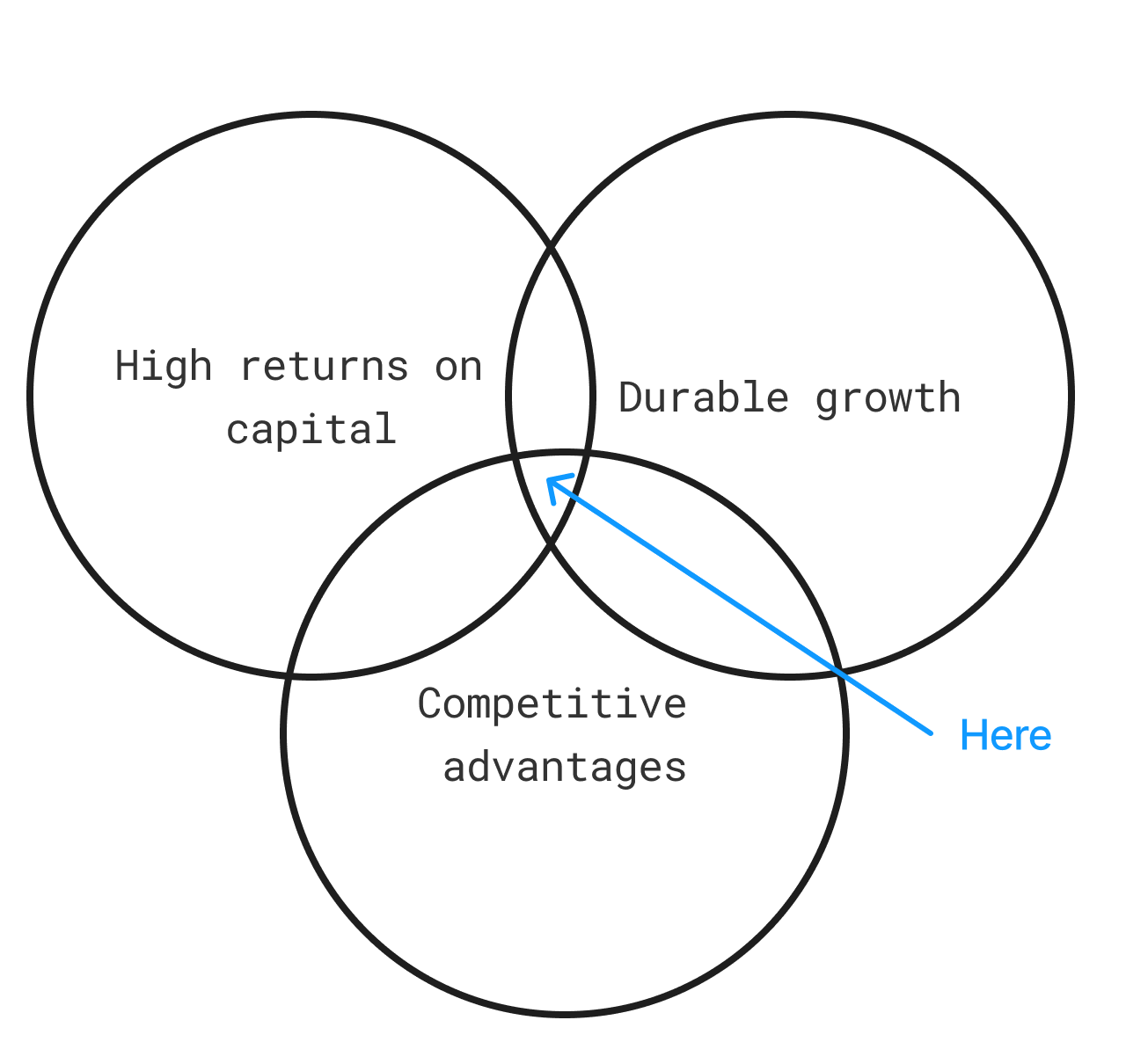

We invest in companies that have high returns on capital, competitive advantages, and durable growth. We focus primarily on fundamentals, and continually reevaluate and rebalance according to where we see the best value.

Businesses with high returns on capital are efficient, making the most of their available capital. They often exhibit low capital intensity and are effective in converting earnings into free cash flow. This allows them to reinvest excess cash flow at high incremental rates of return, and/or return it to shareholders.

Competitive advantages tend to be more qualitative than quantitative – assessing how strong a company’s moat is. Indicators include strong profitability, scale, lead positions in the industry, strong brand with customer following, pricing power, high barrier to barriers to entry, amongst more.

Durable growth can come from secular tailwinds (i.e. growing industries) as well as business model dynamics, for example a compelling approach for increasing spend with existing customers or pricing that increases with inflation.

The combination of efficiency and growth, sustained over time through their advantages, maximizes the magic of compounding. At the end of the day, the portfolio growth will follow the fundamentals.

At Torre Financial, we look for these companies and seek to invest at reasonable prices.

When compared to the S&P 500, our portfolio companies …

are superior in revenue growth

are more efficient in their use of capital on a FCF basis

have superior margins

have stronger balance sheets (lower leverage)

and are cheaper on a FCF yield basis

The relative weakness in ROIC, EBITDA margin, and net income margin is due primarily due to non-cash expenses such as stock-based compensation which are included in those measurements as expenses. Non-cash expenses are real expenses. We monitor those at the company level, keeping a close eye on dilution.

FCF is the ultimate measure. A solid business should generate an abundance of cash flow. The rest of the mechanics such as employee count or stock-based compensation often has a subjective input – management can make changes if or when appropriate.

The combination of superior fundamentals and valuation allows for a high probability bet of outperformance.

High quality companies are rare. In line with our investment philosophy, we aim to keep portfolio turnover at a minimum. Each company is rigorously evaluated and vetted as a long-term opportunity before being introduced.

We hold our portfolio to a maximum of 30 companies, ensuring we pick the best of the best and make the hard decisions when necessary. We strive to invest for 5+ years, which implies we turn over fewer than 6 companies a year. Our turnover activity is low, yet incorporates significant investment in research so that we can have the best possible companies and target allocation.

We are continually evolving our processes to improve. Some of the key performance indicators of our work input are shown below.

This quarter, we added 2 new companies and exited 4.

Diving into the details on the portfolio and target allocation weights…

Keep reading with a 7-day free trial

Subscribe to Torre Financial Newsletter to keep reading this post and get 7 days of free access to the full post archives.